Youth-Led Financial Revolutions: Crowdsourcing as a Catalyst for Investment Innovation

The most useful number to anchor any 2026 conversation about crowdfunding investment is not a price or a return. It is that as of May 2025, 8,492 Regulation Crowdfunding (Reg CF) offerings had cumulatively raised $1.34 billion from retail investors, with an average individual investment of $1,120 per investor. The retail-equity-crowdfunding channel that did not exist before the 2012 JOBS Act now sits inside a global alternative-finance market projected at $316.25 billion in 2025, up from $260.65 billion in 2024. What those numbers actually measure is how much real capital is moving through the permissionless rails of private-company investing right now, which is a more useful signal than any individual deal's pitch deck. What they do not tell us is which of those 8,492 offerings will eventually produce a return — and based on the underlying startup-failure data, most will not. That is the honest limit of the picture.

I write about onchain markets and digital assets day-to-day, and the analytical discipline transfers cleanly to crowdfunding investment. The relevant questions are the same ones I would put to any new asset class: who runs the rails, what does the regulation require, what are the named platforms doing, what are the realistic returns, what are the failure rates, and what is genuinely investable versus what is speculation with a TED-talk wrapper. The rest of this article walks through the actual answers.

A practical caveat up front, because the SEC and FINRA both treat this seriously: this is not individual financial advice. Crowdfunding investments are illiquid, unprotected by FDIC or SIPC, and a meaningful fraction of them will return zero. Talk to a licensed advisor before committing capital from your household savings.

What investment crowdfunding actually is

The cleanest taxonomy comes from J.P. Morgan's institutional explainer, which splits the field into four distinct types — three of which are investment-grade and one of which is not.

1. Donation crowdfunding. A funder gives money with no expectation of financial return. GoFundMe is the canonical example. This is not an investment vehicle; it is a giving vehicle.

2. Rewards-based crowdfunding. A funder gives money in exchange for a product, a perk, or early access. Kickstarter and Indiegogo are the canonical examples. Reward-based crowdfunding contributed roughly $1.05 billion to the US economy in 2025. This is closer to a pre-order than an investment.

3. Debt-based crowdfunding (peer-to-peer lending). The funder lends money to a borrower — an individual, a small business, or a project — and is repaid principal plus interest. The borrower is on the hook regardless of the outcome of the underlying enterprise. This is genuinely an investment vehicle.

4. Equity-based crowdfunding. The funder buys an ownership stake in a company. Returns come from a future acquisition, IPO, or dividend distribution, with no contractual obligation to repay if those outcomes do not materialize. J.P. Morgan reports US equity-based crowdfunding deployed $558 million in 2024, against a 2021 peak of $1.07 billion across 835 deals. This is also genuinely an investment vehicle, and it is the category most of this article is about.

For an investor evaluating the space, the distinction that matters is debt versus equity — the same distinction that matters in public markets. Debt has contractual cash flows and predictable defaults; equity has variance and a long tail of total losses against occasional outsized winners.

Regulation Crowdfunding (Reg CF) and Reg A+

Two SEC frameworks define the retail-investor side of US investment crowdfunding, and both are worth knowing by name.

Regulation Crowdfunding (Reg CF) is the framework that opened private-company investing to non-accredited investors after the 2012 JOBS Act. The current rule allows a company to raise up to $5 million from any combination of accredited and non-accredited investors per 12-month period. Non-accredited investor participation is capped on a sliding scale based on annual income and net worth, with the FINRA-supervised funding portal or broker-dealer required to facilitate the offering. This is the regulatory rails underneath Wefunder, StartEngine, Republic, and most of the rest of the US retail equity-crowdfunding ecosystem.

Regulation A+ Tier II is the next tier up, allowing a company to raise up to $75 million in a 12-month period from any retail investor — accredited or not — with significantly more extensive disclosure requirements. Reg A+ sits structurally between Reg CF and a full IPO, and it is the path taken by larger crowdfunding offerings that want broader retail access without going through the public-markets process.

The investor-protection rationale of both frameworks is the same: limit the maximum a non-accredited investor can put into any single offering, require platform-level intermediation, and mandate disclosure. The rationale does not eliminate risk. It limits its blast radius.

A note on jurisdiction. The EU runs a parallel framework, the European Crowdfunding Service Providers Regulation (ECSPR), which standardised cross-border fundraising under a single license and imposes a mandatory four-day reflection period for non-sophisticated investors before they finalize a commitment. The UK has its own FCA framework with broadly similar investor-protection logic. Cross-border platform access matters: 17% of all EU crowdfunding investments are now cross-border, and according to research summarised by GECA, 40% of successful equity crowdfunding campaigns would have failed without cross-border participation.

Top US crowdfunding investment platforms compared

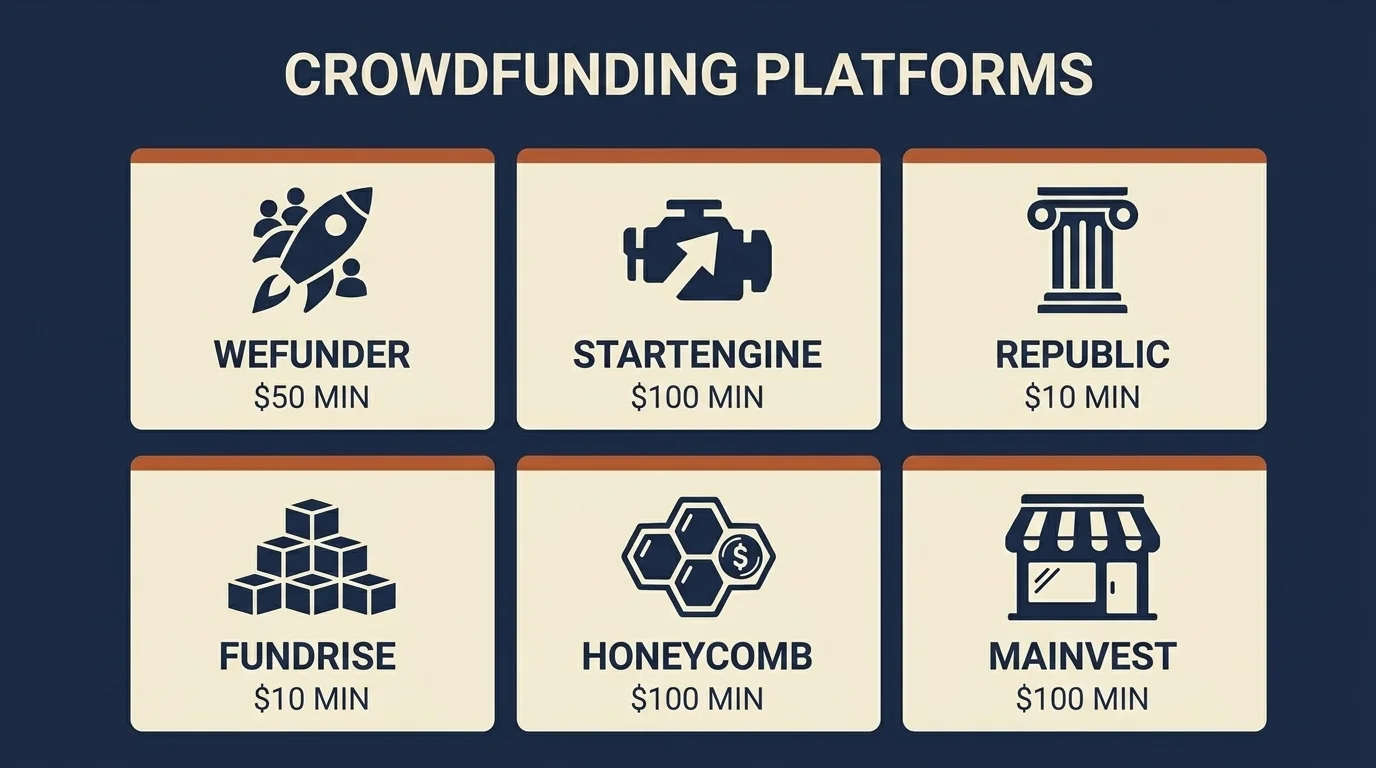

The named-platform list is shorter than the marketing copy suggests. Six platforms cover the substantial majority of US Reg CF and Reg A+ activity. The numbers below are pulled from Bankrate's platform review and P2PMarketData's platform aggregates.

| Platform | Minimum | Deal type | Investor fees | Accreditation |

|---|---|---|---|---|

| Wefunder | $50–$100 | Reg CF equity, Reg A+ | 2% ACH/wire; 5.5% + $2 credit card | Not required |

| StartEngine | $100 | Reg CF + Reg A+ equity | Platform fees vary by offering | Not required |

| Republic | $10 / $50 (tiers) | Reg CF + Reg A+ equity | 2-5% platform fee on capital raised | Not required |

| Fundrise | $10 | Real estate funds (REIT-style) | 0.15% advisory + 0.85% management (1.85% on Innovation Fund) | Not required |

| Honeycomb Credit | $100 | Small-business debt | Targeted return 5–12% annually | Not required |

| Mainvest | $100 | Small-business revenue-share | Variable per offering | Not required |

Cumulative track records: StartEngine has raised $700M+ across 500+ offerings since launch; Wefunder reports $930M since 2012; Republic US reports $2.6B since 2016. The platform-fee benchmark across the industry is 3–8% of capital raised plus 0–2% on exit.

What this table actually tells you. The minimums are genuinely low — $10 to $100 — which means the barrier to participation is no longer the entry check. The barrier is the underlying risk, which the next two sections cover.

Peer-to-peer lending platforms

The debt-based segment is structurally different from equity crowdfunding and worth treating separately. P2P lending matches individual lenders to individual or small-business borrowers, with the platform handling underwriting, servicing, and default management.

The named US platforms are LendingClub, Prosper, and Upstart, each of which has shifted business models over the past five years away from pure retail lending toward institutional-and-bank-facilitated flow. For retail investors, the residual P2P market in the US is more constrained than it was in the 2015-2020 peak — most of the platforms above no longer accept new retail lender accounts. The category persists but the access has narrowed.

The EU and UK P2P landscape is broader. Estateguru, an EU real-estate-backed P2P platform, has cumulatively originated €893 million across 7,296 loans through July 2025, with a historical return of 10.09% and an average loan-to-value ratio of 62%. Republic Europe reports a portfolio-wide IRR of 12.91% from 2012-2022 across £3 billion of cumulative volume. These are not zero-risk numbers — both involve illiquid private exposure that can underperform sharply — but they are at least anchored to reported track records rather than projection.

The analytical distinction: P2P lending generates predictable cash-flow streams when underwriting is sound, similar to any consumer-credit or small-business-credit exposure. Equity crowdfunding does not. Mixing the two on a single platform browse session without keeping the distinction in mind is one of the easier ways to mis-allocate.

2026 trends: coordinated capital, hybrid structures, AI screening

Three current shifts in the space deserve naming.

From "pure crowd" to "coordinated capital". Equity crowdfunding in 2026 is increasingly structured as ecosystems blending retail, professional, and supervised capital rather than as pure retail-driven rounds. The implication for retail investors is that they are increasingly co-investing alongside professional money rather than ahead of it, which changes the screening that happens before a deal hits the platform.

Hybrid deal structures. Equity + revenue-share + debt blends are gaining share over pure-equity rounds. The structure aligns issuer and investor incentives differently — investors get income alongside ownership — but it also raises the disclosure complexity of any individual offering.

AI screening and blockchain transparency. Roughly 40% of platforms or campaigns now integrate AI for deal evaluation and fraud detection, with blockchain transparency layers for cap-table and reporting. What this does not tell us is whether the AI screening is materially improving issuer quality or whether it is mostly marketing. The honest read is that it is doing some of both, and the platforms with the longer track records are the ones whose screening claims I would weight more heavily.

Real estate crowdfunding

A short callout because the adjacent vertical is large. The global real estate crowdfunding market reached approximately $29 billion in 2025, up 43% year-over-year. The structural draws are real — fractional access to commercial and residential real estate, lower minimums than direct ownership, professional asset management — and so are the structural risks. Real estate crowdfunding holdings are typically locked for 5-10 year periods, the underlying assets carry leverage, and platform fees compound across the holding period in ways that compress net returns.

Fundrise, RealtyMogul, Arrived, and the institutional Crowdstreet are the dominant US platforms. The vehicles are different enough from equity crowdfunding that they deserve their own evaluation rather than being treated as the same category.

Your first $100: how to start

The honest framing for a 22-year-old (or a 32-year-old, or a 52-year-old) starting from $100 is that the first dollar through any of these platforms is a learning expense, not a wealth strategy. The numbers below give you the on-ramp.

Read the prospectus. Pick a platform, pick a single offering you find interesting, and read every disclosure document the platform provides. The Reg CF Form C filing is a substantive piece of information that most investors skip; the substance is in there.

Start with $10–$50. Fundrise and Republic both have $10 minimums. A single position at that scale is a stake low enough that the loss is genuinely tolerable and the learning is real.

Diversify across deals before increasing exposure to any one. Given startup failure rates (next section), concentrating $100 in a single Reg CF offering is statistically a coin-flip-with-loaded-coin between zero and a return. Spreading across five to ten offerings does not eliminate the risk but it changes the distribution.

Track the platform's track record over a real time horizon. Look at what the platform has produced in cumulative returns over five-plus years, not what the marketing page says about the most successful single exit.

Match the asset to a portfolio bucket. Treat crowdfunding investment as a sleeve of your overall portfolio — typically the same sleeve you would use for any other illiquid private exposure — not as a substitute for diversified public-market index exposure.

Honest risks: illiquidity, dilution, failure rates

Every previous section has been about access. This one is about what the access is access to.

Illiquidity. Most equity-crowdfunding positions are locked until acquisition, IPO, dividend distribution, or platform-mediated secondary sale. The realistic holding period is 5-10 years, sometimes longer. Real estate crowdfunding holds are typically in the same range. P2P loans amortize over their stated term but cannot generally be sold before maturity. Whatever capital you commit, treat as committed until the underlying event happens — not until you change your mind.

Dilution. In equity crowdfunding, subsequent funding rounds dilute your ownership stake. The Reg CF round is rarely the last round the company will raise. The terms of subsequent rounds typically include anti-dilution protection for new institutional investors that does not extend to the prior Reg CF holders.

Failure rate. This is the number most readers will skip and that I am going to put squarely in the middle of the article. Across the broader US startup ecosystem, roughly 50-60% of early-stage companies fail before a meaningful exit, and the failure rate inside Reg CF-funded companies is at minimum in that range and likely higher, because Reg CF tends to be the channel companies use when institutional capital is harder to raise. Treat any single Reg CF equity position as a probable partial-to-total loss until the company demonstrates otherwise. The thesis is built on the small number of winners covering the cost of the larger number of losses.

No FDIC or SIPC protection. Crowdfunding investments are not insured. They are not bank deposits, and they are not brokerage cash. If the platform fails, the protections you have come from the platform's own custody structure and FINRA portal supervision, not from the federal deposit-insurance system. The FINRA investor education page on crowdfunding is worth reading in full before allocating.

Platform risk. Several US crowdfunding platforms have shut down over the past decade. When a platform fails, the underlying investments typically transfer to a successor servicer, but the experience for the investor — locked positions, slow reporting, complicated tax treatment — is uniformly worse than continuing operations.

Operational safety note. If you suspect fraud at the issuer or platform level, report to the SEC at sec.gov/tcr, the FTC at ReportFraud.ftc.gov, and FINRA via the BrokerCheck and complaint pathways. None of this is legal advice — if you have lost meaningful capital to a fraudulent offering, contact a securities attorney for recovery steps.

Related Article: Sustainable Investing: Aligning Values with Financial Goals

What would change my view

I want to close on what I would actually watch for, because the framing above rests on one specific assumption: that the regulatory rails for retail equity crowdfunding remain stable enough for a multi-year track record to develop. Two things would change my view.

The first would be a meaningful change in the Reg CF cap or accredited-investor threshold from the SEC over the next regulatory cycle. Either a significant raise of the cap (making the channel more attractive to larger issuers) or a tightening of the non-accredited investor limits (making access more constrained) would shift the equilibrium of who actually deploys capital here.

The second would be a sustained, transparent reporting of platform-level realized-return data — something the industry has so far been reluctant to standardise. Until investors can compare platform-by-platform realized returns the way they compare mutual-fund track records, the analytical work is harder than it needs to be.

Until those things happen, the right working position on crowdfunding investment is the one any honest treatment of an illiquid alternative asset class arrives at: small allocations, diversification across many positions, long time horizons, and clear-eyed expectations about failure rates. As always, none of this is individual financial advice. Before committing capital to any specific platform or offering, talk to a licensed advisor who can see your overall balance sheet, your tax situation, and the part of your portfolio this exposure would actually fit inside. The structure is the article. The decision belongs with someone who can see you specifically.

Frequently Asked Questions

Minimums in 2026 are genuinely low. Fundrise and Republic offer entry points at $10. Wefunder, StartEngine, Honeycomb Credit, and Mainvest sit at $50-$100. The barrier to participation is no longer the entry check — it's the risk of the underlying offering. As of May 2025, the average individual Reg CF investment is $1,120, but starting at the minimum is a reasonable way to learn the platform before committing more.

Reg CF allows a company to raise up to $5 million from any combination of accredited and non-accredited investors per 12-month period, with non-accredited limits scaled to income and net worth, and a FINRA-supervised funding portal facilitating the offering. Reg A+ Tier II allows up to $75 million per 12-month period with significantly broader disclosure requirements. Reg A+ sits structurally between Reg CF and a full IPO.

No — and the regulators are explicit about this. Crowdfunding investments are illiquid (typically 5-10 year holds for equity and real estate), unprotected by FDIC or SIPC, and subject to the underlying ~50-60% early-stage startup failure rate. Treat any single equity position as a probable partial-to-total loss until the company demonstrates otherwise; the thesis is built on a small number of winners covering the larger number of losses. The FINRA investor education page on crowdfunding lays out the risk framework in detail.

Returns vary by deal structure. Debt-based platforms like Honeycomb Credit target 5-12% annually. Equity-based portfolios are higher-variance: Republic Europe reported a portfolio-wide IRR of 12.91% from 2012-2022 across £3 billion of cumulative volume, but individual deals frequently return zero. Estateguru's EU real-estate-backed P2P book has reported a 10.09% historical return at an average 62% loan-to-value. Past performance is not indicative — and platform-level realized returns are still inconsistently reported across the industry.

Rarely. Most equity-crowdfunding positions are locked until acquisition, IPO, dividend distribution, or platform-mediated secondary sale — typically 5-10 years. A few platforms (StartEngine, Republic) offer limited secondary markets but liquidity is thin and pricing is opaque. P2P loans amortize over their stated term but cannot generally be sold before maturity. Treat any committed capital as committed until the underlying event happens.

The structural shift is that retail investors — many of them under 35 — now have direct access to private-company and small-business capital that was previously the domain of institutions only. As of May 2025, the US Reg CF channel has cumulatively raised $1.34 billion across 8,492 offerings, and the global alternative-finance market sits at a projected $316 billion in 2025. The behavior is also more sophisticated: the 2026 trend in equity crowdfunding is 'coordinated capital' — retail investors co-investing alongside professionals rather than ahead of them — and hybrid deal structures blending equity, revenue-share, and debt are gaining share over pure-equity rounds.

Check Out These Related Articles

Securing Financial Health: Safeguarding Consumer Interests in Investment Products

Finance Mentor vs Sponsor: What Actually Compounds a Career

Red vs. Blue: The Battle of Colors in Investment Marketing