Sustainable Investing: Aligning Values with Financial Goals

The number worth starting with for sustainable investing in 2026 is not "ESG investing is up" or "ESG investing is dead." It is $84 billion in net redemptions from global sustainable funds in calendar 2025 — the first year of net outflows since Morningstar began tracking the universe in 2018. What that measures is revealed preference at scale: how investors who control the allocation actually behaved versus what they said in surveys. What it does not tell you is whether the category is structurally broken or whether the outflows reflect a temporary brand problem on top of a sound investment thesis. The honest answer is both — and the rest of this article is about how to think clearly about sustainable investing in 2026 without joining either of the two unhelpful camps that have hardened around the topic.

The 2026 Reality Check

Five things changed since the typical 2024-era sustainable-investing guide was written:

- First net-outflow year on record. Global sustainable mutual funds and ETFs bled $84B in 2025 versus $38B in inflows during 2024. US sustainable funds notched 12 consecutive quarters of net outflows through Q4 2025.

- Benchmark outperformance collapsed. Only 26% of ESG indexes outperformed their non-ESG equivalents in 2025, down from 45% in 2024.

- Institutional retreat from the "ESG" label. BlackRock rebranded its sustainable-investing business as "transition investing" in mid-2024, renamed 18 funds totaling $42B AUM with transition terminology, and dropped sustainability terms from 56 funds totaling $51B AUM ahead of the ESMA fund-naming rules effective 21 May 2025.

- SEC climate rule withdrew. The SEC voted on 27 March 2025 to end its defense of the March 2024 Climate-Related Disclosures Rule; the Eighth Circuit declined a merits decision in September 2025 and is holding the case in abeyance. US public companies currently have no federal climate disclosure mandate.

- EU SFDR is being rebuilt. The European Commission's November 2025 SFDR 2.0 proposal abolishes the existing Article 8 and Article 9 categories and replaces them with three new categories (Sustainable, Transition, ESG Basics), each requiring at least 70% of assets to meet category-specific criteria. No grandfathering for existing funds.

Despite all of that, global sustainable fund AUM still grew about 4% in Q4 2025 to over $3.9 trillion — driven entirely by stock-market appreciation, not new money. The category is alive, smaller, slower, and going through an honest reset. The category is not dead; it is also not the boom story it was in 2021.

ESG vs SRI vs Impact vs Ethical vs Transition

The first reason readers are confused about sustainable investing in 2026 is that the field has at least five distinct vocabularies that get used interchangeably in casual conversation and mean materially different things in a fund prospectus. Untangling them is the first useful step.

| Label | Definition | Approach | Example fund | Best for | Limitation |

|---|---|---|---|---|---|

| ESG | Uses environmental, social, governance factors as risk inputs alongside financial analysis | Tilt — overweight high-ESG, underweight low-ESG; minimal exclusions | iShares ESG Aware MSCI USA (ESGU) | Investors who want broad-market exposure with a sustainability tilt | Often >95% holdings overlap with the benchmark — the tilt is real but small |

| SRI | Socially Responsible Investing — historical term predating ESG | Negative screening — exclude whole industries on values grounds (tobacco, weapons, fossil fuels) | iShares MSCI KLD 400 Social (DSI) | Investors with firm exclusions who accept some active-management risk | Concentrated by exclusion; can underperform during sector-specific rallies |

| Impact | Capital deployed for measurable social or environmental outcomes alongside return | Outcome — invest where the capital itself creates the change (green bonds, microfinance, affordable housing) | Calvert Impact Capital, community development financial institutions, green bond funds | Investors with explicit non-financial goals and patience for measurement | Lower liquidity; harder to benchmark; mission-fit varies by fund |

| Ethical | Umbrella retail term displacing "ESG" as the public-facing label | Mixed — usually a combination of tilt + exclusion | Many advisor-marketed "ethical portfolios" | Investors who want a less politically loaded vocabulary | Imprecise — read the prospectus; the term means different things at different firms |

| Transition | Finances companies actively decarbonizing rather than excluding them | Engagement + sector inclusion (energy, industrials with credible transition plans) | BlackRock-rebranded funds; many EU "Article 9 transition" funds | Investors who believe excluding heavy emitters cedes influence | Newer label; methodology varies; some "transition" funds look identical to old ESG holdings under a new name |

The labels overlap but are not synonyms, and the practical implication is that a "sustainable" portfolio built from ESG tilt funds will look very different from one built from SRI exclusion funds, which will look very different from one built from impact funds. Decide which approach matches your actual reason for sustainable investing before you pick a ticker.

Did ESG Investing Fail? An Honest Look at the Numbers

The headline answer is: no, but the brand failed, and the performance gap is real. The 2024 numbers tell the cleaner story. Large-blend sustainable funds returned a median 20.7% versus 21.5% for conventional funds and 24.1% for the Morningstar US Market Index — sustainable funds trailed by roughly 80 basis points against conventional and 340 bp against the broad market index. That is a meaningful gap, but it is not catastrophic underperformance. The structural reason for the trailing returns is straightforward: most ESG tilt funds underweight energy, which had a strong 2024. Methodology matters more than ideology here.

2025 was harder. Only 26% of ESG indexes beat their non-ESG benchmarks, down from 45% in 2024 — a sharp deterioration that underwrites the redemption wave. The 12-consecutive-quarters-of-US-outflows streak is the revealed-preference data: investors who were comfortable holding sustainable funds during the 2020–2021 boom started rotating out as the outperformance argument lost its empirical support.

What this data does not tell you is whether the underperformance is structural (the screens systematically exclude winning sectors) or cyclical (energy and defense, both common exclusions, happened to rally during the recent window). The honest read is that both are partly true. Investors with a 10-year horizon and a firm preference for the sustainability tilt can reasonably accept a small expected return drag in exchange for the values alignment; investors who picked sustainable funds purely on the "ESG outperforms" pitch from 2020–2021 are now experiencing the predictable consequence of having bought a thesis that was always going to revert.

The right framing is the one Eli's CFA training instilled in this kind of question: name the time horizon. Over a 5-year period through 2024, a fund like ESGV (Vanguard ESG US Stock ETF) returned 13.03% annualized — competitive on an absolute basis with broad-market alternatives, with a small relative trail. That is the actual data the decision needs to be made against, not the "ESG outperforms" or "ESG is dead" headlines on either side of the discourse.

ESGV vs ESGU: The Head-to-Head

The two largest, lowest-cost ESG ETFs cover most of the practical retail decisions in this category. They look nearly identical at the wrapper level and behave somewhat differently underneath.

| Metric | ESGV (Vanguard) | ESGU (iShares) |

|---|---|---|

| Issuer | Vanguard | BlackRock / iShares |

| Expense ratio | 0.09% | 0.15% |

| AUM | ~$11.1B | ~$14.8B |

| Methodology | FTSE US All Cap Choice Index — broad exclusion screen (fossil fuels, tobacco, weapons, adult entertainment, gambling) | MSCI USA Extended ESG Focus Index — ESG tilt that overweights higher-ESG securities while staying close to the broad market |

| 1-year return | 11.71% | 11.83% |

| 3-year return | 20.64% | 19.39% |

| 5-year return | 13.03% | 13.19% |

| Style | Exclusion-heavier | Tilt-heavier |

The practical distinction is between what gets removed (ESGV) and what gets reweighted (ESGU). ESGV's broad exclusion screen takes whole industries out of the portfolio; ESGU keeps a closer-to-market exposure and tilts within it. Cost-conscious investors who want the exclusions pick ESGV at 9 basis points. Investors who want benchmark-like exposure with a sustainability layer pick ESGU and pay the additional 6 bp. The one-year returns are nearly identical because both funds are dominated by large-cap US equities, and that segment moves together; the methodology differences show up on a multi-year horizon and during sector-rotation episodes.

What this comparison does not tell you is what happens during a true energy-sector rally, where ESGV's full exclusion bites harder than ESGU's tilt. The 2022 oil bid was a small preview; a similar 2026 episode would widen the gap meaningfully.

The 2026 ESG ETF Comparison

For investors who want to look beyond the two flagship funds, the practical 2026 ESG ETF menu spans cost leaders, broad-market screens, and thematic tilts. The table below is a snapshot, not advice; verify each fund's current prospectus before allocating.

| Ticker | Issuer | Expense ratio | Approximate AUM | Methodology / focus | What it's for |

|---|---|---|---|---|---|

| VOTE | TCW Transform 500 | 0.05% | ~$0.5B | S&P 500 with active engagement / proxy voting | Lowest-cost ESG-style US large-cap exposure |

| XVV | iShares ESG Select Screened S&P 500 | 0.08% | ~$0.5B | S&P 500 with screening | Cheap S&P-500-shaped ESG screen |

| ESGV | Vanguard | 0.09% | ~$11.1B | FTSE All Cap Choice — broad exclusion | US large-cap with firm exclusions |

| ESGU | iShares | 0.15% | ~$14.8B | MSCI USA Extended ESG Focus — tilt | US large-cap with light tilt |

| SUSA | iShares | 0.25% | ~$5.6B | MSCI USA Extended ESG Select — best-in-class | Higher-conviction ESG large-cap tilt |

| DSI | iShares | 0.25% | ~$3.7B | MSCI KLD 400 Social — historical SRI index | Long-running SRI screen with track record back to 1990 |

| ESGD | iShares | 0.20% | ~$9.4B | MSCI EAFE Extended ESG Focus | Developed ex-US ESG exposure |

| ICLN | iShares | 0.41% | ~$2.2B | S&P Global Clean Energy | Thematic — clean energy companies only |

VOTE at five basis points is the current cost leader and the cleanest example of the "engagement, not exclusion" approach — same S&P 500 holdings as a standard index fund, with proxy voting tilted toward shareholder ESG resolutions. XVV at eight basis points is the cheapest path to a screened large-cap. ESGV and ESGU are the workhorse middle of the menu. The thematic funds (ICLN especially) sit on their own — they are a sector bet, not a diversified ESG core.

Transition Investing: What BlackRock's Rebrand Actually Means

The most visible institutional retreat from the "ESG" label happened at BlackRock. In mid-2024 the firm rebranded its sustainable investing business to "transition investing"; in the run-up to the European Securities and Markets Authority (ESMA) fund-naming rules effective 21 May 2025, BlackRock renamed 18 funds totaling $42 billion AUM with transition-related terms and dropped sustainability terminology from another 56 funds totaling $51 billion AUM.

What "transition investing" actually means: financing companies that are actively decarbonizing rather than excluding heavy emitters wholesale. The thesis is that owning a high-emitting cement company with a credible decarbonization plan and using shareholder engagement to enforce it does more for real-world emissions than refusing to own the company at all. The argument has merit. It also has the obvious failure mode of "transition" becoming a license to hold whatever the manager wants to hold while keeping the sustainability marketing intact. Read the holdings.

The practical takeaway for retail investors is that "transition" funds are mostly the same holdings under a less politicized label, sometimes with strengthened engagement language. If you held the BlackRock funds before the rebrand, you still hold what you held; if you are choosing one now, the relevant question is the same as for any other sustainable fund: what does the methodology actually do?

Sidebar: Anti-ESG — Real Trend or Media Story?

Anti-ESG funds (RSPM, MAGA, DRLL, and similar tickers) explicitly avoid ESG screens or invest in "politically incorrect" sectors. They get more discourse attention than dollar attention: combined AUM is under $300 million. At the state level, 11 anti-ESG bills passed across 10 Republican-trifecta states in 2025 out of 106 introduced — a low success rate reflecting the financial costs of earlier statutes (notably higher municipal borrowing costs in Texas after its 2021 anti-ESG law). On 3 February 2026 a Texas federal district court enjoined Senate Bill 2337 — the proxy-advisor anti-ESG law — as unconstitutional. For most retail investors, anti-ESG is news to follow, not a portfolio choice to make.

Sidebar: What Happened to the SEC Climate Rule?

The SEC adopted the Climate-Related Disclosures Rule in March 2024 but voluntarily stayed it pending litigation. On 27 March 2025 the SEC voted to end its defense of the rule. In September 2025 the Eighth Circuit declined to rule on the merits and is holding the case in abeyance. The practical state of climate disclosure for US issuers in 2026: no federal mandate; California's SB 253 and SB 261 are operative for large companies doing business in the state; the EU's Corporate Sustainability Reporting Directive (CSRD) applies to qualifying US subsidiaries of EU groups and to large US issuers with significant EU operations. The federal regulatory floor is currently absent.

Sidebar: ESG Ratings Disagree

The three major ESG rating providers — MSCI, Sustainalytics (a Morningstar subsidiary), and ISS — frequently rate the same companies very differently. In published academic studies the cross-rater correlation hovers around 0.6, well below the ~0.99 correlation between major credit-rating agencies. The reason is not incompetence; it is that ESG ratings aggregate dozens of subjective component scores with different weightings, and small methodology differences compound. The practical implication: do not treat any single ESG rating as gospel. Use ratings as one input, read the methodology behind whatever rating you rely on, and recognize that a company with a strong rating from one provider may carry a weak rating from another.

Impact Investing: The Distinct Category

Impact investing search volume is rebounding +21% MoM/QoQ, and the category is genuinely different from ESG. Where ESG funds reweight a broad-market portfolio against sustainability metrics, impact funds deploy capital where the capital itself creates the change — green bonds funding specific renewable projects, community development financial institutions (CDFIs) lending to underserved geographies, microfinance funds, affordable-housing bond funds. The expected returns are typically lower than broad-market alternatives, and the liquidity is more limited, in exchange for the directly attributable outcome.

For a retail investor with a modest impact allocation (a single-digit slice of portfolio), the practical menu is green-bond ETFs (BGRN, GRNB), community-investment notes (Calvert Impact Capital, Community Investment Notes), and the small number of registered impact mutual funds. The CDFI route requires more legwork — most CDFIs accept direct investment via notes with 1–10 year terms — but is where the highest-attribution capital deployment happens.

What this kind of investment does not tell you is whether the impact dollar would have been more effectively deployed through philanthropy. For many investors, the cleanest framing is to separate the investment dollar (compound returns at low cost in broad index funds) from the impact dollar (donate to high-leverage charities, or invest in CDFIs with full awareness of the return cost). That separation is the third path discussed below.

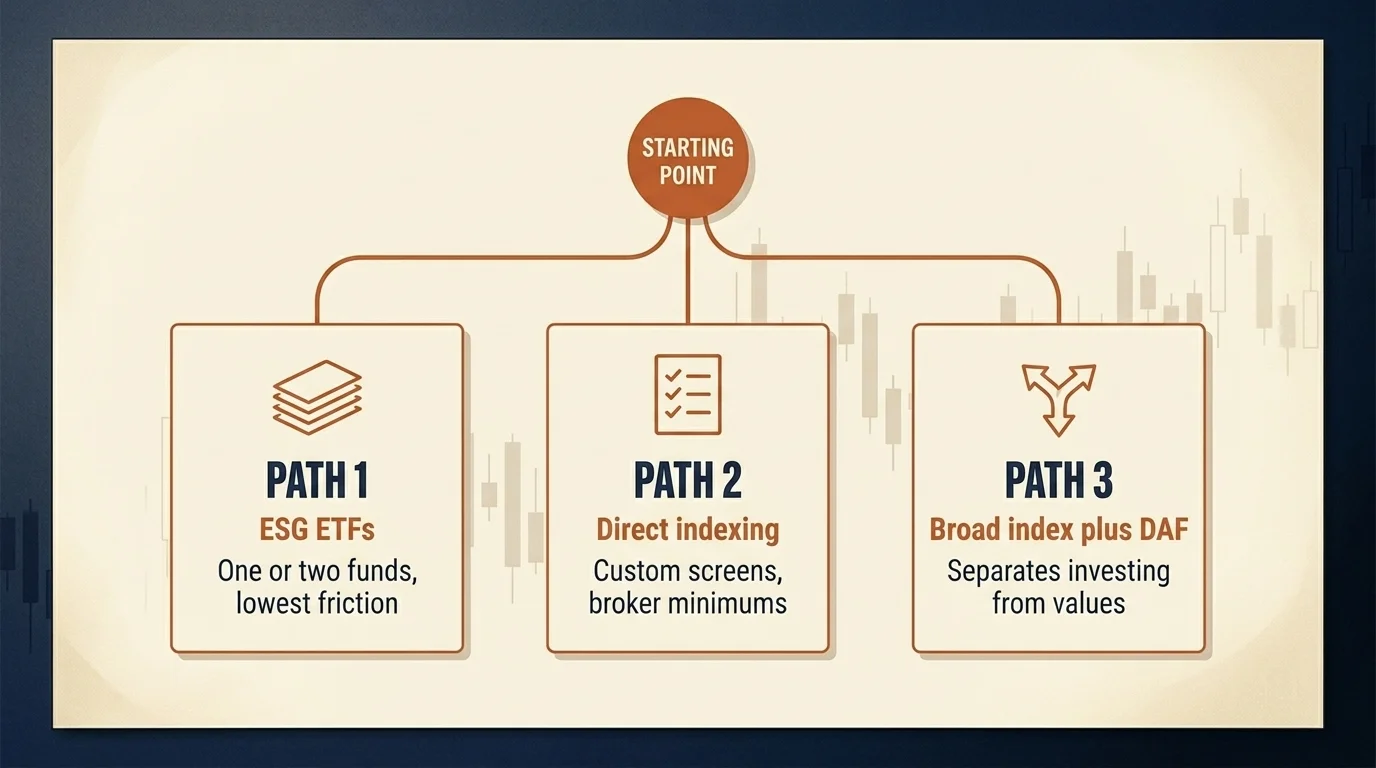

Three Paths to Values-Aligned Investing

The fund question — which ESG ETF to hold — is the most-discussed path because it has the lowest friction. It is not the only path.

Path 1: ESG / SRI / Transition ETFs. Lowest effort. Pick one or two of the funds in the comparison table above, set a target allocation, rebalance on schedule. Total cost runs from 5 basis points (VOTE) to 25 basis points (DSI, SUSA). For most retail investors, this is the right path, full stop.

Path 2: Direct indexing with personal screens. Several brokerages now offer direct indexing — you own the underlying stocks of a custom-screened index instead of an ETF, which lets you exclude specific companies (or sectors) by name and lets you tax-loss-harvest at the individual-position level. Wealthfront, Frec, and Vanguard Personalized Indexing run this product; minimums range from roughly $5,000 (Wealthfront, Frec) to $100,000 (Vanguard PI). Costs are typically meaningfully higher than an ESG ETF, partially offset by the tax-loss-harvesting benefit. The path makes sense if you have an unusual exclusion list (specific companies, specific sub-industries) that no off-the-shelf ETF gives you.

Path 3: Traditional indexing plus a Donor-Advised Fund. The often-overlooked path: invest the portfolio in low-cost broad-market index funds (lowest expense ratio, no values-screen drag, full tax efficiency), and route the values-expression dollar through a donor-advised fund where you donate appreciated stock and grant out to specific high-leverage charities or impact funds. For tax-aware investors with both compounding goals and charitable goals, this is often the most efficient structure — you separate the two questions and optimize each one independently rather than tangling them inside a single ETF wrapper.

The right path depends on dollar size, time horizon, how strong your specific exclusion list is, and whether you have a separate charitable budget. The honest answer for most retail investors at typical brokerage-account size is Path 1 with one or two ETFs.

Where to Start in 2026

For an investor with a small to moderate portfolio who wants to start the sustainable-investing allocation today, a concrete five-step action list:

- Pick the right category for your reason. ESG tilt if you want broad-market exposure with light sustainability weighting. SRI if you want firm exclusions on specific industries. Impact if you want measurable attribution. Transition if you believe engagement beats exclusion.

- Choose one or two ETFs from the comparison table. For most retail investors, ESGV plus a thematic complement (ICLN for clean energy, or ESGD for international diversification) is a defensible starting point. VOTE if cost is the primary driver.

- Set an explicit allocation target. 5%, 10%, 20% of the portfolio — write the number down. Sustainable investing without a target percentage is just an emotional commitment; with a target percentage it becomes a rebalancing rule.

- Decide your tax-loss-harvesting practice. ETF-level tax-loss harvesting (selling ESGV at a loss and replacing with a similar but not identical ETF) preserves the allocation while capturing the tax benefit. If you want individual-position tax-loss harvesting, that is the case for Path 2 above.

- Review annually, not weekly. Fund methodology, expense ratios, and AUM change slowly. Check once a year, rebalance if needed, do not chase quarterly performance.

Related Article: Impact of Inflation on Investment Strategies

What Would Change My View

The thesis underneath this article is that sustainable investing as a category is alive, smaller, and going through an honest reset — not dead, and not the boom it was in 2021. The expected return drag for the typical ESG tilt fund versus a broad-market index runs in the 50–100 basis point range over multi-year periods, more during sector-rotation episodes that favor excluded industries. That is a tolerable cost for an investor with a real sustainability preference and a long horizon; it is not a free lunch.

What would change my view? Two consecutive years in which (a) net flows to sustainable funds turn positive again at a meaningful scale, and (b) the share of ESG indexes outperforming their non-ESG benchmarks recovers to a clear majority. Either signal alone is suggestive; both together would indicate the category has worked through its 2022–2026 reset and is operating in a different regime. Until that data prints, the right answer for an individual allocator is small allocation, low-cost ETF, clear category choice, annual review.

The category has changed shape and is going to keep changing — SFDR 2.0 will reshape European fund labels by 2028, the SEC climate-disclosure question is unresolved, and the "ESG" brand itself may not survive the decade in retail use. None of that argues against sustainable investing as a portfolio sleeve; it argues for picking based on what the fund actually does, not on what its label says it does.

This article is for educational purposes only and is not individual financial advice. Sustainable-investing fund holdings, expense ratios, and performance data change frequently; always verify a fund's current prospectus, holdings, and methodology before investing. Consult a licensed financial advisor for guidance matched to your specific situation. Past performance does not guarantee future returns.

Frequently Asked Questions

No, but it changed shape. Global sustainable fund AUM grew to over $3.9T in Q4 2025, but 2025 was the first year of net outflows ($84B globally) since tracking began in 2018, and only 26% of ESG indexes beat their non-ESG benchmarks that year (vs 45% in 2024). The category is alive, just smaller, slower, and rebranded.

ESG uses environmental/social/governance factors as risk inputs alongside financial analysis. SRI (socially responsible investing) typically excludes whole industries — tobacco, weapons, fossil fuels — on values grounds. Impact investing deploys capital for measurable social/environmental outcomes alongside returns. Ethical investing is the umbrella retail term replacing 'ESG' since the politicization. Transition investing is BlackRock's 2024 rebrand emphasizing financing companies in the process of decarbonizing rather than excluding them. They overlap but aren't synonyms.

Mixed and worsening. In 2024 the median large-blend sustainable fund returned 20.7% vs 21.5% for conventional and 24.1% for the Morningstar US Market Index — close but trailing. In 2025 only 26% of ESG indexes beat their non-ESG equivalents, down from 45% in 2024. Specific funds like ESGV have returned 20.64% on a 3-year basis through early 2026 — competitive, but not a free lunch.

It depends on cost vs methodology. ESGV (Vanguard) charges 0.09% with ~$11.1B AUM and excludes more industries (fossil fuels, tobacco, weapons, adult entertainment, gambling); ESGU (iShares) charges 0.15% with ~$14.8B AUM and uses a lighter MSCI ESG-tilt methodology that keeps more of the broad market. 1-year returns are nearly identical (ESGV 11.71% vs ESGU 11.83%). Cost-conscious investors with stronger exclusion preferences pick ESGV; investors who want benchmark-like exposure pick ESGU.

For US large-cap ESG exposure: ESGV (Vanguard, 0.09% ER, broad screens) and ESGU (iShares, 0.15% ER, lighter tilt). Cheapest options: VOTE (TCW Transform 500, 0.05% ER) and XVV (iShares ESG Select Screened S&P 500, 0.08%). International: ESGD (developed ex-US) and VSGX (Vanguard global ex-US). Thematic climate: ICLN (iShares Global Clean Energy).

Transition investing finances companies actively decarbonizing rather than only those already 'green.' BlackRock rebranded its sustainable business to 'transition investing' in 2024, renamed 18 funds ($42B AUM) with transition-related terms, and dropped sustainability terminology from 56 funds ($51B AUM) ahead of the ESMA fund-naming rules effective 21 May 2025. The shift reflects political pressure in the US, regulatory pressure in the EU, and recognition that 'ESG' had become a brand liability.

No. The SEC adopted the Climate-Related Disclosures Rule in March 2024 but voluntarily stayed it pending litigation, then voted to end its defense of the rule on 27 March 2025. In September 2025 the Eighth Circuit declined to rule on the merits and is holding the case in abeyance. US public companies currently have no federal climate disclosure mandate; California's SB 253/261 and the EU's CSRD are the operative climate-disclosure regimes for large companies.

They're directional, not definitive. MSCI, Sustainalytics (Morningstar), and ISS often rate the same company differently — the cross-rater correlation in published academic studies hovers around 0.6, far lower than the ~0.99 correlation between credit-rating agencies. Use ratings as one input, not gospel; read the methodology for any rating you rely on.

Anti-ESG funds (e.g., RSPM, MAGA, DRLL) explicitly avoid ESG screens or invest in 'politically incorrect' sectors like fossil fuels and weapons. They exist as a media phenomenon more than a portfolio strategy — combined AUM is under $300M. State-level anti-ESG legislation passed 11 bills across 10 Republican-trifecta states in 2025 (out of 106 introduced), and a Texas federal court enjoined Senate Bill 2337 on 3 February 2026 as unconstitutional. For most retail investors, this is news to follow, not a portfolio choice to make.

Yes. Three viable paths: (1) ESG/SRI/transition ETFs — cheapest and lowest effort, expense ratios from 0.05% (VOTE) to 0.25% (DSI, SUSA); (2) direct indexing with personal screens via Frec, Wealthfront, or Vanguard Personalized Indexing — you own the underlying stocks and exclude what you want, but minimums range $5k–$100k; (3) traditional low-cost index funds plus a Donor-Advised Fund — separates investing decisions from values-expression decisions, often the most tax-efficient path for affluent investors with both return and charitable goals.

Check Out These Related Articles

Securing Financial Health: Safeguarding Consumer Interests in Investment Products

Finance Mentor vs Sponsor: What Actually Compounds a Career

Youth-Led Financial Revolutions: Crowdsourcing as a Catalyst for Investment Innovation