Culinary Capital: Exploring the Fusion of Food Choices and Financial Strength

Food prices in the United States are forecast to rise 2.9% in 2026 overall, but the USDA Economic Research Service projects a split that matters more than the headline number: food-at-home is set to rise 2.4%, while food-away-from-home is set to rise 3.6%. The cost gap between cooking at home and eating out, which has been widening since 2022, is now wide enough to be a real planning lever — and meal planning to save money is the cheapest, most reliable household habit for capturing it. A household that shifts even five restaurant meals a month to the kitchen recovers a measurable, recurring chunk of cash flow.

The other half of the math is waste. The average US family of four throws away roughly $2,275 of food a year, and eliminating that waste alone cuts a grocery bill by 30-40%. A thirty-minute Sunday meal-planning session does most of the waste work and most of the budget work at the same time. This is a CFP's guide to running that session, anchored on actual USDA budget numbers, with a sample week you can copy and a 2026-current price-trend table you can plan a season around.

How much should you actually budget for groceries?

The most useful starting point for any household grocery budget is not someone else's blog. It is the USDA's Cost of Food monthly reports, which publish four reference budgets — Thrifty, Low-Cost, Moderate-Cost, and Liberal — recalculated monthly. They are the policy anchor that SNAP benefits, dietary-guidelines analyses, and most credible personal-finance budgeting frameworks rely on. The current 2026 numbers, drawn from USDA's January reports and summarized by MealThinker and Chowhound:

| Household | Thrifty plan | Low-cost plan | Moderate-cost plan | Liberal plan |

|---|---|---|---|---|

| Single adult male (19–50) | ~$309/month | ~$320/month | ~$391/month | ~$478/month |

| Single adult female (19–50) | ~$247/month | ~$280/month | ~$345/month | ~$443/month |

| Family of 4 (two adults, two kids) | $1,002/month ($12,026/year) | ~$1,060/month | ~$1,310/month (per-adult $330–$391) | ~$1,580/month |

A few things worth saying plainly about these numbers. First: the Thrifty Plan is not the bare minimum that nutritionally works. It is the lowest of the four cost tiers USDA publishes as adequate. A household running below it is generally either cooking entirely from scratch with strong shopping discipline or undereating in some way that matters. Second: the Moderate Plan is the most useful target for most middle-income households — it allows for some convenience products, occasional name brands, and routine fresh produce, while still leaving real budget headroom. Third: most households who have not actually tracked their grocery spending are surprised by where they land. If you do not know the number, the first useful step is one month of receipts, totaled.

The USDA reevaluation of the Thrifty Food Plan is on hold under the 2025 One Big Beautiful Bill Act — the next reevaluation can occur no earlier than October 1, 2027 — so the 2026 figures will hold as the policy anchor for at least eighteen months. Safe to plan against.

The 30-minute Sunday meal-plan ritual

A meal-planning session does not need an app, a binder, or a system. It needs about thirty minutes on a recurring weekly slot and five steps in roughly this order.

- Pantry audit (5 minutes). Open the fridge and the pantry. Write down the ingredients that need to be used this week before they spoil, and the staples that are running low. This single step is where most of the $2,275/year food-waste number disappears.

- Sales scan (5 minutes). Open the digital flyer for the grocery store you actually shop at. Note any deeply discounted proteins or staples (chicken thighs, ground beef, eggs, beans, frozen vegetables) — these are the spine of the week's plan.

- Menu draft (10 minutes). Plan five to seven dinners around the proteins and staples flagged in steps 1 and 2. Aim for two or three meals that share a base ingredient (a roasted chicken on Sunday becomes chicken tacos Monday and chicken soup Wednesday), one or two new recipes the household will eat, and one deliberate "leftovers and pantry-clear" night. Breakfast and lunch get a default rotation, not a daily plan.

- Grocery list (5 minutes). Build the list directly from the menu. Group by store section (produce, dairy, pantry, frozen, refrigerated) — that is where shopping-time efficiency comes from, not from any app.

- Estimated total (5 minutes). Before you leave the house, run a rough sum of the list against the prior week's per-item costs. If you are tracking against a Thrifty or Moderate target, this is the check that prevents the gap from compounding silently over a quarter.

The ritual works because every step removes a decision that would otherwise be made under fluorescent light at the end of a long day, when the marginal-decision quality of the household is at its weekly low. The point of the ritual is not perfection. It is decision pre-commitment.

Related Article: Ethical Considerations in Personal Finance and Healthcare Nexus

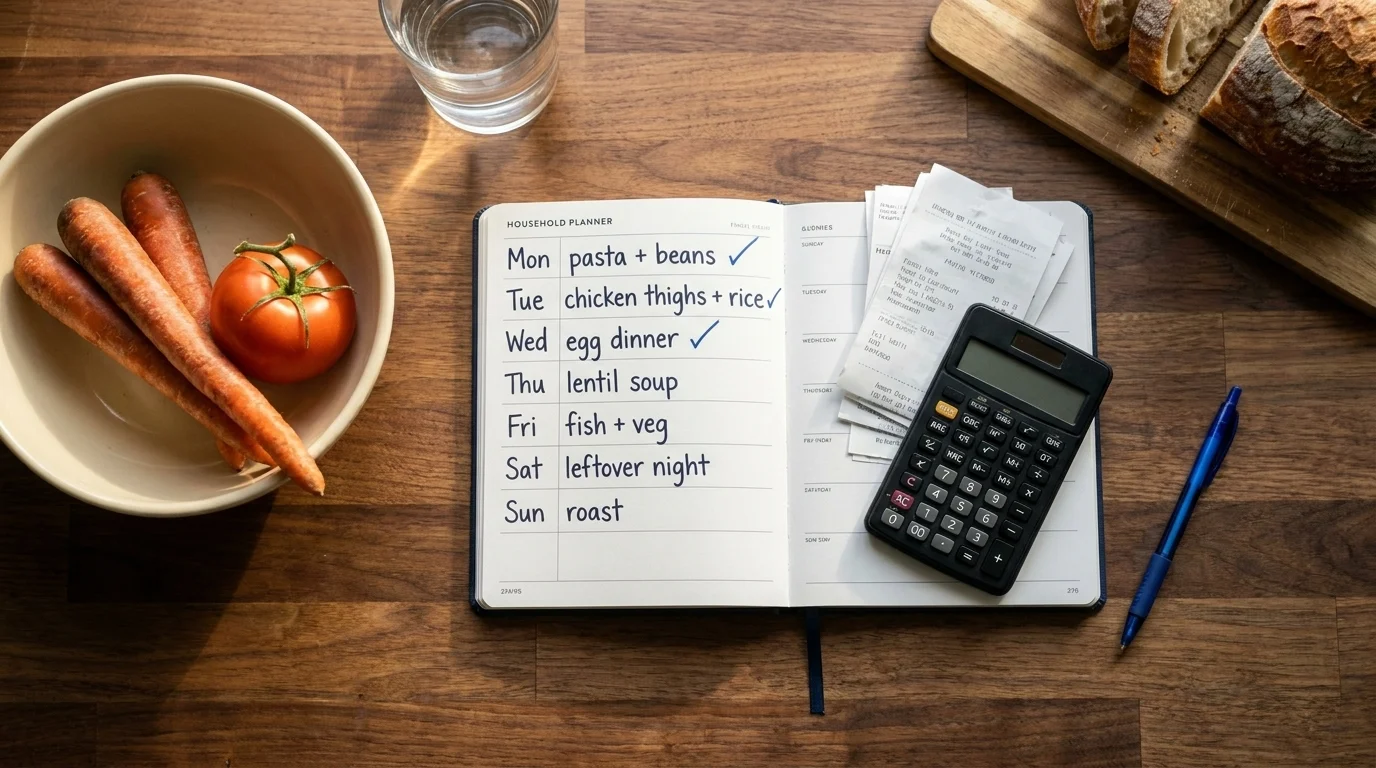

A 7-day family-of-4 sample meal plan and grocery list

The sample below targets the USDA Thrifty Plan range (roughly $1,002/month / $231/week for a family of four). It assumes one omnivore household with two adults and two school-age kids, a working pantry of basic spices and condiments, and ordinary US-suburban grocery prices. Adjust freely.

| Day | Dinner | Spine ingredient |

|---|---|---|

| Sunday | Roasted chicken with potatoes and roasted carrots | Whole chicken |

| Monday | Chicken tacos with cabbage slaw and refried beans | Sunday chicken leftover |

| Tuesday | Pasta with sausage, kale, white beans (one-pot) | Italian sausage |

| Wednesday | Chicken-and-rice soup with frozen vegetables (from Sunday's chicken carcass + broth) | Sunday chicken carcass |

| Thursday | Black bean and sweet potato bowls with rice | Beans, sweet potato |

| Friday | Sheet-pan eggs with potatoes, peppers, and onions (breakfast-for-dinner) | Eggs |

| Saturday | Pantry-clear stir-fry: whatever vegetables remain, with rice and the last of the protein | Leftovers |

Grocery list, with rough running cost (US suburban average, January 2026):

- 1 whole chicken (~5 lb) — $9

- 1 lb Italian sausage — $5

- 1 dozen eggs — $3 (eggs are forecast to drop 29% this year — see the swap table below)

- 2 lb dried black beans + 1 lb dried white beans — $4

- 4 lb potatoes — $4

- 2 sweet potatoes — $2

- 1 bag carrots — $2

- 1 head cabbage — $3

- 1 lb kale — $3

- 1 small bag tortillas — $3

- 1 lb rice — $2

- 1 lb pasta — $2

- Onions, garlic, peppers (mixed) — $7

- Salsa, refried beans (canned) — $5

- 1 bag frozen mixed vegetables — $3

- Milk, butter, basic dairy for breakfasts and packed lunches — $12

- Bread for packed lunches — $4

- Fresh fruit for the week — $12

- Peanut butter, jam (for sandwiches and breakfasts) — $5

- Cereal, oatmeal — $6

- Snack and lunchbox staples (yogurt, cheese, crackers) — $14

- Running total: ~$110 for the dinner spine; ~$53 for breakfast/lunch staples; total ~$163 for the week.

The week lands modestly under the Thrifty weekly target for a family of four. Slight overruns in any week — a $5 splurge on better cheese, a $6 substitution for grass-fed beef — are absorbed inside the cushion. If the actual total is materially higher, the question is which line you bought that the plan did not anticipate, and whether the answer is "we genuinely needed it" or "the kids and I were tired and bought twelve other things."

The 2026 inflation-aware swap table

Not every protein and produce category is moving in the same direction in 2026. USDA ERS's April 2026 outlook breaks out the categories most relevant to household grocery planning:

| Category | 2026 forecast | Implication for the weekly plan |

|---|---|---|

| Eggs | −29.4% | Post-avian-flu recovery. Lean in — eggs are the cheapest complete protein on the shelf this year. Sunday brunch, breakfast-for-dinner, baked goods. |

| Dairy | Declining | Stock up modestly on staples (milk, butter, basic cheese). Premium cheese remains a discretionary indulgence. |

| Pork | Stable / soft | Continues to be a good rotation protein alongside chicken. |

| Chicken | Roughly stable | Whole birds and bone-in cuts remain the per-pound winner; boneless skinless breast prices stay elevated. |

| Beef | +6.3% | On top of a roughly 37% run from 2019 to 2024. Treat as a deliberate-occasion protein, not the weekly default. |

| Fresh vegetables | +4.8% | Plan around what is in season locally; frozen vegetables are a meaningful price-stability hedge. |

| Cereals and bakery | Roughly stable | Lean toward store-brand; the per-unit savings hold. |

| Restaurant meals (FAFH) | +3.6% | Discussed in the next section. |

The headline year for a household running a tight grocery budget is: eggs are dramatically cheap, beef is dramatically not, and the gap between the two is the largest it has been in recent memory. Households running 4–5 meals a week with eggs and beans as the protein spine, two meals a week with chicken or pork, and beef as an explicit weekend or occasion meal will see the largest 2026-specific savings versus a beef-default plan.

Discount-grocer math: Aldi, Lidl, and Costco in 2026

The discount-grocer category has visibly destigmatized over the past two years. NPR reported in May 2026 that Aldi and Lidl prices were running more than 8% below Walmart on comparable baskets. For a household spending the Thrifty Plan ~$1,002/month, a clean shift of the primary grocery shop from Walmart to Aldi recovers in the neighborhood of $80/month — about $960/year — for substantively the same food.

The store-brand decision compounds the same logic at a finer grain. Yahoo Finance's reporting on grocery tactics puts the comparable-product savings at roughly 25% per item when a household systematically defaults to the store brand on staple categories (pasta, canned tomatoes, baking staples, cereal, basic dairy). Most US households can substitute store-brand on about 60–70% of items before they hit a category they have a defensible reason to keep brand-loyal on — and that line is different for every household, which is the point.

The Costco math is its own conversation: the membership cost is roughly $65/year (Gold Star) or $130/year (Executive). For households shopping monthly, the Executive 2% cashback typically pays for the membership tier upgrade within a few months on grocery and gas spending alone. The cost-per-unit advantage is concentrated in specific categories (proteins, paper goods, dairy basics, baking staples) and is materially smaller or absent on others (fresh produce, specialty items). Costco is a stack-on-top-of strategy for a household that already runs a primary discount-grocer plan, not a replacement for one.

The opportunity cost of dining out

The cleanest CFP-grade framing for restaurant spending is not "stop eating out." It is "see the cost of a restaurant meal in the same units you measure everything else in your portfolio." A representative example: a $60 dinner-for-two, eaten once a week, is $3,120 a year. Invested instead at a 7% real annual return over 30 years, that same $3,120/year contribution compounds to roughly $295,000. Not a typo. The 7% number is the conventionally-cited long-run real-equity assumption — your mileage will vary; the point is not the precise endpoint but the shape of the comparison.

The honest planning question is not whether to dine out. It is how often and with what cap. For most households I see across a planning conversation, the answer that holds up well is treating restaurants as a sinking-fund line item with a stated monthly cap — typically 10-15% of total food spend. A family of four running a Moderate Food Plan budget of ~$1,310/month would land in the $130-$200/month range for dining out. The arithmetic is more interesting than the moralizing: every $100/month moved from food-away-from-home to food-at-home is approximately $1,200/year, which is approximately $115,000 in 30-year real-FV terms at the same 7% assumption. Not "give up restaurants." Move the dial deliberately and see the compounded shape of the move.

The 2026-specific reason this matters more than usual: the 1.2-percentage-point gap between FAFH (+3.6%) and FAH (+2.4%) forecast inflation widens that arithmetic further every year. The compounding is no longer the only force pulling in one direction.

Related Article: The Art of Financial Planning for Young Professionals: Building Wealth from the Start

What to actually do this week

For a reader who has gotten this far:

- Run one month of grocery receipts, total them, and compare to the relevant USDA tier for your household. Most households are surprised. The number is the starting point — not a judgment.

- Block a 30-minute Sunday slot for the meal-planning ritual. Treat it as a recurring calendar item, not an aspiration. The cheapest cash-flow lever in the household budget is decision pre-commitment on weekly food spend.

- Run the discount-grocer experiment for one month — make Aldi, Lidl, or your closest equivalent your primary grocery shop for four consecutive weeks. The roughly 8% delta is large enough to be visible in the first month's receipts.

- Set a sinking-fund cap on dining out in writing, at a stated dollar figure per month. The compounded math of even a modest move is the kind of number that does not show up in any single statement and quietly dominates the household's 30-year balance sheet.

The Thrifty-vs-Moderate gap, the FAH-vs-FAFH gap, and the discount-grocer delta are the three numbers that drive most of the durable grocery-budget improvement available to a middle-income US household in 2026. They are also the three numbers a generic blog post cannot calibrate for your specific household — bracket, family size, dietary requirements, the regional grocery options actually within driving distance. For decisions of any size, the calibration belongs in a conversation with someone who can see the rest of the picture, not at the end of an article.

Frequently Asked Questions

USDA's January 2026 Thrifty Food Plan puts the cost at roughly $1,002/month (~$12,026/year) for two adults and two kids; the Moderate plan runs about 30-40% higher. Most middle-income households target the Moderate range, which allows some convenience products and routine fresh produce while still leaving budget headroom.

Yes — eliminating food waste alone can cut a grocery bill 30-40%, and the average US family throws away roughly $2,275 of food per year. A 30-minute Sunday ritual (pantry audit, sales scan, menu, list, estimated total) recaptures most of that and is the cheapest cash-flow lever available to most households.

Eggs — USDA ERS projects a 29.4% price drop in 2026 as the egg market recovers from avian flu. Beef is forecast to rise another 6.3% on top of a roughly 37% climb since 2019. Beans, eggs, and bone-in chicken are the strongest per-pound protein plays for the year.

NPR's May 2026 reporting cites Aldi and Lidl prices running more than 8% below Walmart on comparable baskets. For most US households, switching the primary grocery shop to a discount-grocer is the single largest one-time savings move available — roughly $80/month for a household on the Thrifty Food Plan budget.

Treat restaurants as a sinking-fund line item with a stated monthly cap (typically 10-15% of total food spend). Food-away-from-home prices are forecast to rise 3.6% in 2026 vs. 2.4% for food-at-home — the math increasingly favors cooking. A $60-per-week restaurant habit compounds to roughly $295,000 over 30 years at a 7% real return; the point isn't to stop, it's to move the dial deliberately.

A 30-minute Sunday ritual: (1) pantry audit — what needs to be used this week; (2) check store sales for discounted proteins and staples; (3) plan 5-7 dinners around a shared protein with at least one leftovers night; (4) build the grocery list grouped by store section; (5) estimate the total before you shop. The point is decision pre-commitment, not perfection.

The Thrifty Food Plan is the lowest of four USDA reference budgets (Thrifty, Low-Cost, Moderate-Cost, Liberal) that USDA publishes monthly. It anchors SNAP benefits and is the most widely-cited 'minimum adequate' grocery cost figure. The 2025 One Big Beautiful Bill Act froze the next TFP reevaluation until at least October 2027, so the 2026 figures are stable to plan against for at least 18 months.

Check Out These Related Articles

Embracing Rational Decision-Making: The Psychology of Prudent Financial Choices

Financial Wisdom through the Ages: Learning from Ancient Philosophers and Modern Financial Gurus

Redefining Financial Literacy through Interactive Social Media Initiatives