Financial Wisdom through the Ages: Learning from Ancient Philosophers and Modern Financial Gurus

The philosophy of money has, in the last three years, become a content category. The Daily Stoic — the largest Stoicism brand online — now runs a dedicated wealth vertical. Darius Foroux's The Stoic Path to Wealth (Portfolio/Penguin, 2024) sits on the canonical-reference shelf for "stoic investing". And at least one US wealth-advisory firm now positions itself explicitly under the Stoic banner. As a planner I find this both encouraging and slightly suspicious — encouraging because the underlying principles are genuinely useful, suspicious because financial media tends to absorb any serious idea and grind it down into a content hook.

So let me try to do something more useful than that, which is to walk through what the ancient philosophers actually said about money, what survives translation into a modern financial philosophy framework, and where I think the marketing has run ahead of the substance. Three or four ideas in this lineage are genuinely load-bearing for the way I do planning work. The rest is decoration.

What the Stoics actually said about money

The dominant 2025 framing — and the one that has won — is to map the four Stoic cardinal virtues (wisdom, courage, justice, temperance) onto personal-finance behavior (Four Philosophies on Stoic principles for personal finance). It is a tidier scaffolding than the older "Stoicism teaches discipline" one-liner, and I am willing to use it. But I want to be specific about what each virtue actually translates to in dollars, not just in vocabulary.

Wisdom is research. It is reading a fund prospectus before agreeing to the share class, reading the 10-K before buying the stock, and reading a plan document before opting into a new 401(k) auto-feature. It is the opposite of moving on a headline.

Courage is the willingness to act on the research once you have done it — most often by not selling when your portfolio is deep in the red during a recession, by holding through a sequence-of-returns shock at the front edge of retirement, and by continuing to contribute through the bad years that produce most of the long-run return. It is not the courage to buy individual stocks on a tip.

Justice is the recognition that money has external consequences — that what you pay for has a supply chain behind it, and that the way you accumulate capital is not separate from how the wider economy is structured. Whether you operationalize that as ESG screens, charitable contributions, or simply not investing in things you would be embarrassed to defend is a personal question. The Stoics would have considered the question itself non-optional.

Temperance is the savings rate. It is the difference between a household that saves a serious fraction of its income and one that saves a token amount. Over a multi-decade horizon at any plausible real-return assumption, that single variable swamps almost everything else a financial planner can do for you.

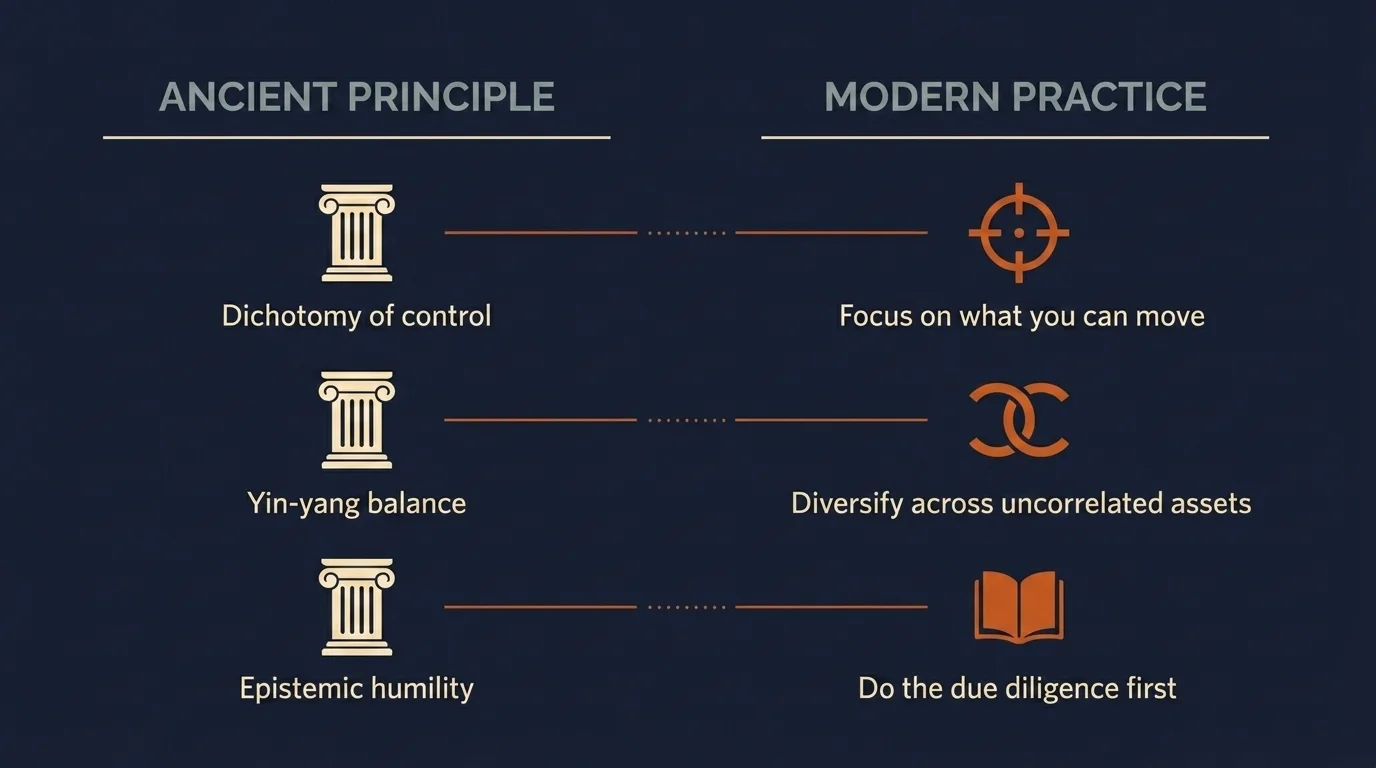

The Stoic texts themselves are surprisingly direct on money. Seneca's Letters from a Stoic, written in the first century AD to his friend Lucilius, returns repeatedly to the idea that wealth is acceptable provided it does not own you. Marcus Aurelius's Meditations — written to himself as private notes during a Roman emperor's working day — treats material concerns as a category to be observed, not chased. Epictetus's Enchiridion is the source of what is now called the dichotomy of control: the principle that you should focus your energy on what is within your power and let go of what is not. In a financial context, the dichotomy maps cleanly onto a list I have given clients more times than I can count.

Within your control: your savings rate, your asset allocation, your withdrawal sequencing, your tax planning, your time horizon, your decision to read or not read the daily market headlines. Outside your control: next quarter's returns, where inflation prints, what the Fed does, what your neighbor's portfolio did, what a YouTube finance personality thinks. A stoic mindset in financial terms is the willingness to spend almost all your effort on the first list and almost none of your effort on the second. This is not abstract. Households that internalize this distinction make different decisions during recessions, and the difference compounds.

A modern Stoic investing playbook

What Foroux and the broader modern stoicism current have done is take these principles and operationalize them as numerics. Whether or not you buy the marketing, the rules themselves are useful and worth naming.

The three-pillar structure in The Stoic Path to Wealth is: earning money, losing money, and growing money (Foroux, The Stoic Path to Wealth). The order is deliberate — you cannot grow capital you have not earned, and you cannot grow capital you cannot stop losing. Most retail investors I see skip directly to "growing" because that is what financial media is about, and the result is predictable.

The 90/10 rule allocates 90% of investable assets to broad index funds and 10% to anything speculative, including individual stocks (Foroux, The Stoic Path to Wealth). The exact split is less important than the structural commitment: the bulk of your portfolio compounds in the background while a small bounded sleeve absorbs whatever urge you have to be cleverer than the index. The Stoic framing is that the 10% is the part of the portfolio you accept may be wrong; the 90% is the part where you have made a structural decision not to engage with daily price movement.

The 10% maximum-loss-per-position rule sets a hard ceiling on what any single speculative bet can do to the rest of your capital (Foroux, The Stoic Path to Wealth). It is the operational form of Epictetus's dichotomy applied to the speculative sleeve: you cannot control whether a position goes wrong, but you can control how much of your total capital is exposed when it does.

And the line that has become the slogan of the field — "investing is 9% theory, 1% execution, 90% managing emotions" (Foroux, The Stoic Path to Wealth) — is the one I am most willing to repeat. The reason most retirement plans fail is not that the math is wrong. The math is mostly fine. They fail because a household sells equities at the bottom of a recession, locks in the loss, and never re-enters the market — or because a household pulls retirement contributions to chase a hot sector and never replaces the contributions. Both are emotional failures dressed in financial vocabulary.

A useful extension here is premeditatio malorum — Stoic negative visualization — applied to financial planning. It is the practice of asking, in advance, what the worst plausible version of next year looks like, and pricing the plan to survive it (New Trader U on Stoic strategies). In practice this is what every honest retirement plan does: it stress-tests a deep equity drawdown in year one of decumulation, names how many years of expenses are held in short-duration fixed income, and asks whether the household can hold its course without selling equities into the loss. The Stoics did not invent stress testing. But the framing is correct.

Aristotle, Graham, Buffett: the prudence chain

Now I want to draw a longer line than most of the popular Stoic-investing literature does.

Aristotle, in the Politics and the Nicomachean Ethics, distinguished oikonomia — the prudent management of a household, including its resources — from chrematistike, the accumulation of money for its own sake without natural limit. He approved of the first and was sharply critical of the second. The distinction is not anti-wealth; it is anti-purposeless-accumulation. The question for any acquirer was whether the wealth served a defined life or whether the acquiring had become the life.

That distinction is the philosophical ancestor — and I mean this literally, not as a stretch — of Benjamin Graham's The Intelligent Investor, the 1949 book that almost single-handedly defined the modern value-investing tradition. Graham's framing of margin of safety, of the difference between investment and speculation, and of the requirement that an investment be defended by analysis and a reasonable expectation of preserving capital, is Aristotelian prudence wearing a fedora. Graham was not quoting Aristotle. He did not have to. The intellectual lineage was already in the water.

Warren Buffett was Graham's student at Columbia Business School and worked for him at Graham-Newman before launching his own partnership. The warren buffett philosophy as articulated in the Berkshire Hathaway annual letters — concentrated ownership of high-quality businesses bought at sensible prices, indefinitely long holding periods, near-total indifference to short-term price action — is Graham's framework iterated and refined. Charlie Munger, Buffett's longtime partner, made the chain more explicit by repeatedly attributing his own decision-making framework to a small set of dead Europeans, the Stoics among them.

The reason I belabor this is that the entire chain — Aristotle → Graham → Buffett → Munger — is built on a single Aristotelian commitment: that money is a tool inside a defined life, not a scoreboard. Every popular financial-media presentation of any of these figures elides that commitment because it does not sell. The honest version of the lineage is not "be like Buffett". It is "decide what the money is for, and then let that decision shape every subsequent question about the money".

Plato sits at the front of the same lineage in a quieter way. His commitment to epistemic humility — the principle that one should refuse to claim more knowledge than one actually possesses — is the philosophical root of the boring discipline of due diligence. The honest investor's answer of "I do not know enough yet" is Platonic.

Eastern philosophy: yin-yang and Buddhist non-attachment

The Eastern half of the synthesis is usually written badly — generic yin-yang gestures followed by generic "mindfulness" gestures. There is more substance available than that.

The yin-yang principle of balance between opposing forces maps onto portfolio construction in a specific way: a diversified portfolio is not a portfolio that goes up when one thing goes up; it is a portfolio whose component returns are not perfectly correlated, so that the whole has lower volatility than any single piece. The yin-yang framing is not a substitute for the math, but it is a useful intuition for clients who otherwise want to hold whatever asset was hottest last year. Concentration on a winner feels right; balance feels wrong; balance is usually correct.

Buddhist non-attachment has a sharper modern application than is usually written. The relevant behavioral-finance overlap is loss aversion — Daniel Kahneman and Amos Tversky's prospect-theory finding that losses register psychologically at roughly twice the magnitude of equivalent gains. Loss aversion is the engine behind almost every emotional investing failure I see in practice: selling equities at the bottom, holding losing positions past the point of recovery, refusing to recognize a capital loss for tax purposes because closing the position would make the loss feel real. The Buddhist non-attachment frame — that one's identity and well-being should not be hostage to any particular outcome — is the philosophical counter-practice. Whether or not you frame it in Buddhist terms, the work is to dampen the asymmetry between how losses and gains land.

Confucian frugality and the broader East Asian household-savings tradition are worth one more sentence here. The savings rates that quietly drive multi-decade outcomes in many Asian and Asian-diaspora households are not philosophical accidents. They reflect a household-level cultural commitment to temperance that the four-cardinal-virtues framing would recognize immediately.

Ancient principle, modern practice

Here is the cross-tradition synthesis as a single table. None of it is a recommendation. It is a translation key.

| Ancient principle | Tradition | Modern financial practice |

|---|---|---|

| Dichotomy of control | Stoic (Epictetus) | Focus on savings rate, allocation, withdrawal sequencing, tax planning; ignore daily market noise |

| Premeditatio malorum | Stoic (Seneca, Aurelius) | Retirement stress testing; sequence-of-returns risk budgeting; cash reserve sizing |

| Aristotle's mean | Aristotelian | Periodic portfolio rebalancing back to target allocation |

| Oikonomia vs. chrematistike | Aristotelian | Defining the life the money is for before setting accumulation targets |

| Buddhist non-attachment | Buddhist | Counter-practice for loss aversion; rules-based selling instead of emotion-driven selling |

| Yin-yang balance | Daoist / Chinese | Diversification across uncorrelated assets, not concentration in last year's winner |

| Confucian frugality | Confucian | A savings rate sustained across decades, not optimized in one year |

| Plato's epistemic humility | Platonic | Due diligence before acting; "I do not know enough yet" as a valid investment thesis |

The table is not the article. The point is that the principles are not in conflict. They converge on the same handful of behaviors — moderate savings sustained for a long time, decisions that survive negative scenarios, a clear-eyed sense of what is and is not within your control, and a willingness to be unimpressed by short-term outcomes.

What this means for your own planning

I want to close in the way I close most things, which is to acknowledge that I cannot see your situation from a blog post, and that the answer to any specific question about your money depends on facts I do not have — your time horizon, your marginal tax bracket, your withdrawal sequencing assumptions, your household's actual cash needs over the next five years.

What I can tell you is this. If you read about Stoicism and money and the only thing that survives the exercise is "I am going to be calmer about short-term market movements", that alone will probably improve your outcomes over a 25-year horizon more than any tactical asset-allocation decision you make this year. If you read about the philosophy of money and conclude that you want to define what the money is for before setting an accumulation target, you are doing better thinking than most of the financial media you will encounter this year. And if you take from any of this the more specific operational rules — a 10% ceiling on any speculative position, a 90% commitment to broad index ownership, a written stress test of the worst plausible year, a savings rate held through the bad ones — you have done the actual work the philosophical tradition is pointing at.

The right way to apply any of this to your own household is the boring one: discuss the specifics with a fiduciary planner who can see the whole picture, particularly the tax and withdrawal-sequencing variables that no general article can address. The philosophy is the frame. The planning is the work.

Frequently Asked Questions

Through Epictetus's dichotomy of control: focus your effort on what is within your power — savings rate, asset allocation, withdrawal sequencing, tax planning, time horizon — and stop spending energy on what is not — next quarter's returns, headlines, what your neighbor's portfolio did. The modern Stoic-investing canon adds three operational rules on top: a 90/10 split between broad index funds and a bounded speculative sleeve, a hard 10% maximum-loss-per-position ceiling, and the recognition that investing outcomes are roughly 90% emotion management.

Aristotle distinguished oikonomia — the prudent management of a household and its resources — from chrematistike, the accumulation of money for its own sake without natural limit. He approved of the first and was sharply critical of the second. The distinction is not anti-wealth; it is anti-purposeless-accumulation. This Aristotelian prudence framework is the direct philosophical ancestor of Benjamin Graham's The Intelligent Investor and, through Graham, of Warren Buffett's and Charlie Munger's investing discipline.

The named modern Stoic-investing lineage runs Aristotle → Benjamin Graham → Warren Buffett → Charlie Munger. Graham's margin-of-safety framework, Buffett's indefinitely long holding periods and indifference to short-term price action, and Munger's repeated attribution of his decision-making framework to Stoic and other classical sources all sit on the same intellectual foundation. Darius Foroux's 2024 book The Stoic Path to Wealth has popularized this as a named investing school with concrete rules.

The most useful translation is the four cardinal virtues: wisdom as research, courage as the willingness to hold through downturns, justice as awareness that capital has external consequences, and temperance as a sustained savings rate. Beyond the virtues, Epictetus's dichotomy of control gives investors a discipline for ignoring market noise, and Seneca's and Marcus Aurelius's writings reinforce the idea that wealth is acceptable provided it does not own the holder.

Two sharper applications survive translation. The yin-yang principle of balance between opposing forces maps onto portfolio diversification: combining assets whose returns are not perfectly correlated produces a portfolio with lower volatility than any single piece. Buddhist non-attachment is the philosophical counter-practice to loss aversion — Kahneman and Tversky's prospect-theory finding that losses register at roughly twice the magnitude of equivalent gains — which is the engine behind most emotional investing failures. Confucian frugality reinforces the temperance/savings-rate point from a different cultural angle.

Aristotle's framework of prudence, moderation, and the distinction between purposeful and purposeless wealth is the philosophical foundation of modern value investing. Benjamin Graham's insistence on margin of safety and on distinguishing investment from speculation is Aristotelian prudence in modern language. Warren Buffett and Charlie Munger have iterated that framework into the most widely taught investing discipline of the past 75 years.

They give the planning work a frame. Defining what the money is for before setting an accumulation target — the oikonomia question — is better thinking than most retail-investor planning starts with. The Stoic dichotomy of control gives investors a discipline for distinguishing the variables they can move from the ones that move on their own. Premeditatio malorum (negative visualization) is the philosophical root of modern stress testing. None of this is a substitute for individual tax and withdrawal-sequencing planning, but it improves the conversation the household has with its planner.

Plato's commitment to epistemic humility — the refusal to claim more knowledge than one actually possesses — is the philosophical root of due diligence. The honest investor's answer of 'I do not know enough yet' is Platonic. This same disciplined humility shows up in Graham's insistence on analytical defense of every position, in Buffett's circle-of-competence framing, and in Munger's repeated point that the first job of investing is to avoid stupidity rather than to seek brilliance.