The Art of Financial Planning for Young Professionals: Building Wealth from the Start

Financial planning for young professionals comes down to one question I hear most often in a first job: should my first extra dollar go into the 401(k) match, the Roth IRA, the student loan, or the savings account? The honest answer is that it depends on four numbers — your federal marginal bracket, your employer match formula, your highest-interest debt rate, and how many months of expenses you have in cash. Notice that "how the market does next year" is not on that list. For most young professionals, the market return over the next twelve months has less impact on where you end up in twenty years than whether you get the first-paycheck sequence right. Boring, but load-bearing.

The rest of this article is the sequence — built around the 2026 IRS limits that took effect in January, the new SECURE 2.0 rules that change how employer matches and student loans interact, and the SAVE plan termination scheduled for July 1, 2026 that affects 7.5 million borrowers. The math is the same kind of math I run for clients at the desk: name the bracket, name the horizon, then choose.

The 2026 IRS Limits Reference Box

Six numbers anchor most of the planning decisions below. The IRS announced them November 13, 2025; they apply to the 2026 tax year.

| Account | 2026 limit | Catch-up (50+) | Notes |

|---|---|---|---|

| 401(k) / 403(b) elective deferral | $24,500 | $8,000 | Super catch-up (ages 60–63): $11,250 |

| IRA (Traditional or Roth) | $7,500 | $1,100 | Combined limit across all IRAs |

| Roth IRA income phase-out (single) | $153,000–$168,000 | — | Backdoor required above |

| Roth IRA income phase-out (MFJ) | $242,000–$252,000 | — | Backdoor required above |

| HSA (self-only) | $4,400 | — | Triple tax advantage; HDHP min deductible $1,700 |

| HSA (family) | $8,750 | — | HDHP min deductible $3,400 |

Two things in this table matter more than the others for young professionals. First, the new 2026 rule that catch-up contributions to employer plans must be Roth (after-tax) if your prior-year FICA wages exceeded $150,000. If you are on a high-earner trajectory, the strategic value of building Roth habits now — when your bracket is low — increases under this rule because your future catch-up money is being forced into Roth anyway. Second, the HSA's triple tax advantage: tax-deductible contributions, tax-deferred growth, tax-free withdrawals for qualified medical expenses. For young professionals with a high-deductible health plan, the HSA is the most tax-efficient account available, and it is structurally underused because the contribution gets confused with FSA money.

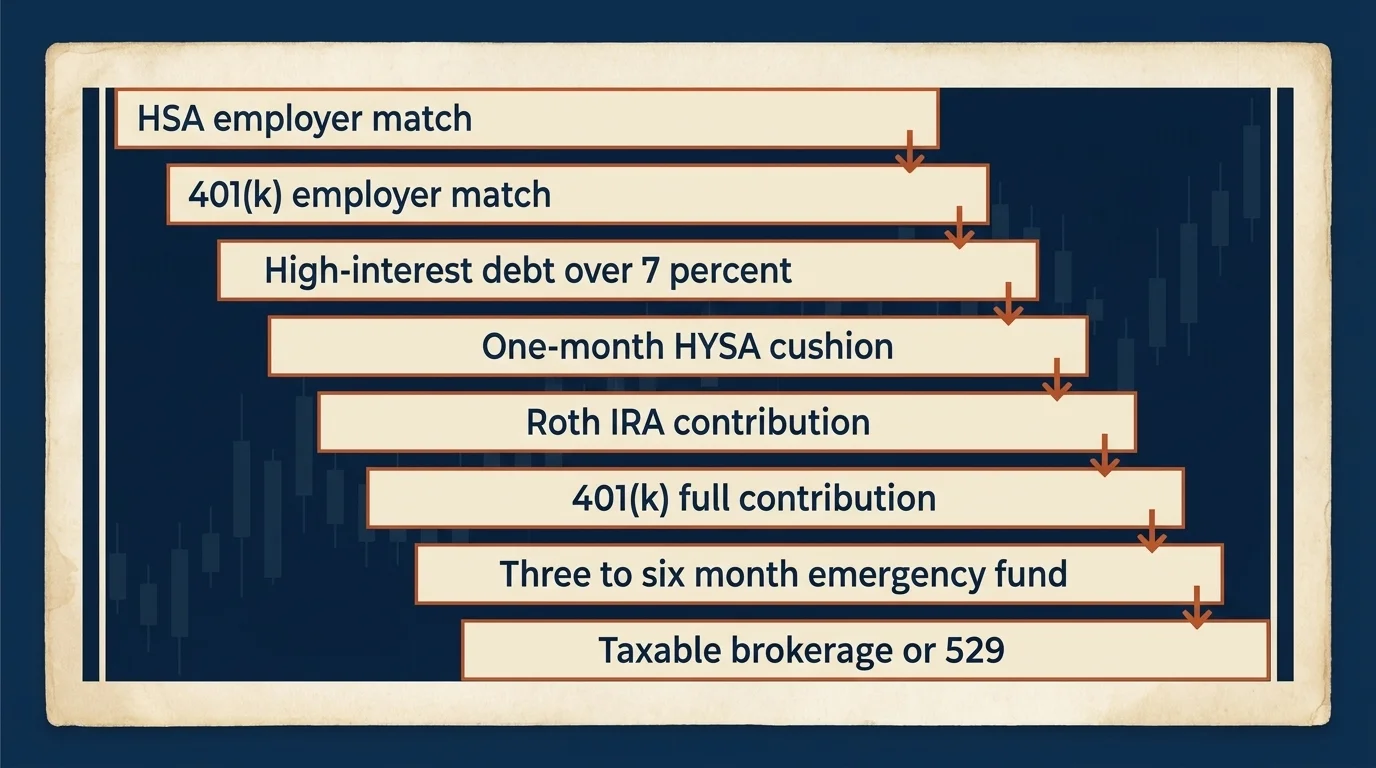

The First-Paycheck Waterfall

The single most useful framework I give young professionals at the desk is a priority sequence — what dollar goes where first. The order matters more than people realize because the highest-return dollar (the employer match) and the highest-cost dollar (high-interest debt) need to come before the rest.

- HSA up to any employer contribution — if you are on an HDHP and your employer contributes to the HSA, capture the contribution. This is rarer than 401(k) matches but worth checking.

- 401(k) match in full — if your employer matches 50% on the first 6% of salary, contribute 6% from day one. A 50% return on the first dollar is unbeatable economics; turning down a match is an unforced error. Many newer 401(k) plans now auto-enroll under SECURE 2.0 at 3–10% with 1% annual escalation — verify yours.

- Kill any debt above ~7% interest — credit-card balances above 18% APR are emergencies. Private student loans above 7%. The math of paying down 9% private debt is a guaranteed 9% return; the long-run real return on equities is roughly 7%. Pay the debt.

- Build a one-month emergency-fund layer in a HYSA — at May 2026 high-yield savings rates of 4.20–5.00% APY, one month of expenses earns roughly the same as a short-term Treasury fund with less complexity. See the emergency fund section below.

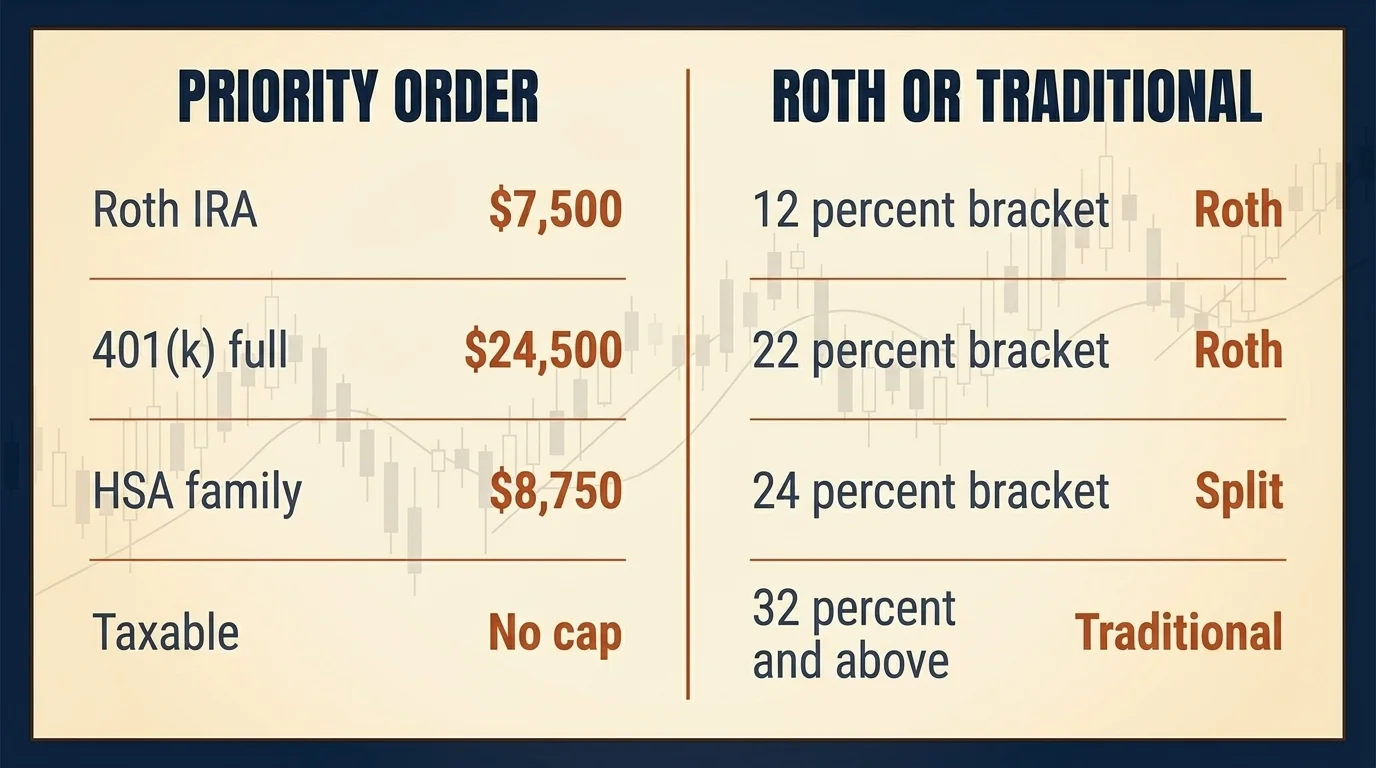

- Max your Roth IRA ($7,500 in 2026) — for almost every young professional in the 12%–24% federal bracket, the Roth wins the math (see the Roth-vs-Traditional section below).

- Top up the 401(k) past the match toward the $24,500 limit — the order of operations between Roth IRA and full 401(k) reflects the IRA's superior investment flexibility (no 401(k)-menu constraint) and the typical young-pro bracket logic. If your 401(k) has an excellent index-share-class TDF available, the gap narrows.

- Build the emergency fund to 3 months, then 6 months — life stage matters here (more below).

- Taxable brokerage / 529 / down-payment savings — only after the tax-advantaged buckets are filled.

A line about why this order: the 401(k) match captures a guaranteed return that nothing else replicates. High-interest debt is a guaranteed cost that no investment can outrun. After those two, the Roth IRA gives you the maximum tax-arbitrage value because you are likely in your lowest lifetime bracket. After that, the priorities are about completion and life stage.

Related Article: Ethical Considerations in Personal Finance and Healthcare Nexus

Budgeting Methods That Work

Two methods cover most of what young professionals actually need.

The 50/30/20 rule is the simplest. On take-home (after-tax) pay, allocate 50% to needs (rent, utilities, groceries, transport, minimum debt payments), 30% to wants (dining, travel, entertainment), and 20% to savings plus extra debt payoff. On a $5,000/month take-home, that is $2,500 needs, $1,500 wants, $1,000 savings. The discipline is in the third bucket: $1,000 a month into a HYSA plus retirement contributions, before any of it gets reallocated to wants.

Zero-based budgeting is the more demanding method — every dollar gets assigned a job at the start of the month, and the budget literally balances to zero. The advantage is precision; the disadvantage is the time cost of running it. Apps like YNAB, Monarch, and Rocket Money exist specifically for the zero-based workflow.

The third method I see work — particularly for variable-income earners — is pay-yourself-first: automate the 20% savings transfer on the day the paycheck hits, treat what is left as the entire spending budget, and skip the line-item categorization. Mechanically simple, behaviorally robust because there is nothing to mess up.

The right method is the one you will actually use for more than three months. Most failed budgets fail because the method asked too much of the budgeter, not because the math was wrong. Start with 50/30/20 or pay-yourself-first; graduate to zero-based only if you actually find yourself wanting more visibility.

Your Emergency Fund in a HYSA

The traditional advice is "three to six months of expenses." That range is correct but unhelpful because it does not match the advice to the situation. The version I use with clients ladders the target:

- 1 month of expenses — start here, before the Roth IRA. Even unstable employment situations are protected by this much cash.

- 3 months — appropriate for dual-income households with stable W-2 employment and no dependents.

- 6 months — single income, one earner supporting a mortgage or kids, or any situation where job replacement would take meaningfully longer.

- 9 months — self-employed, contract worker (1099 income), or specialized employment where re-hiring is slow.

Where the emergency fund lives matters because the opportunity cost is real in either direction. In May 2026, high-yield savings account APYs at the top of the market sit between 4.20% and 5.00% — Varo around 5.00%, SoFi 4.50%, Axos 4.21%, Newtek 4.20%. The FDIC national average savings rate is 0.38%. A $20,000 emergency fund in a HYSA earns roughly $900 a year more than the same fund at your old checking-account bank. That is real money, and it is FDIC-insured up to the standard $250,000 per depositor per institution.

The rule I give clients: park the first three months in a single HYSA; if you go to six or nine months, split the surplus between the HYSA and a short-Treasury ETF or a one-year T-bill ladder. The Treasuries earn slightly more, are state-tax exempt, and ladder out cleanly. Use the HYSA for the actual emergency layer; the additional liquidity beyond three months can earn a bit more.

Student Loans and Debt

The two named debt-payoff methods — snowball and avalanche — solve different problems.

Debt avalanche orders payments by interest rate, highest first. Mathematically optimal: at $50,000 in total debt across multiple accounts, avalanche typically saves about $2,135 in interest and shortens the payoff by roughly three months compared with snowball.

Debt snowball orders payments by balance size, smallest first. Less efficient on dollars, more effective behaviorally — the small wins from closing a paid-off account in the first quarter sustain motivation through the long middle of the payoff process. Academic evidence from the NBER and from a 2012 Kellogg School study finds that concentrating payments on one account at a time increases actual follow-through. Roughly 75% of debt-payoff plans fail within six months; the method that the borrower actually completes beats the method that is mathematically superior on paper.

The decision rule: if you are confident you will see the payoff through (most readers who are reading a planning article are), avalanche saves you more. If past attempts have stalled, snowball gives you the early wins that sustain effort.

The Debt-vs-Invest Bright Line

The cleanest version of the debt-vs-invest decision uses the 7% line.

- Interest rate ≥ 7%: pay down the debt before investing beyond the employer match. The guaranteed return on debt payoff exceeds the long-run expected real return on equities (roughly 7%).

- Interest rate < 5%: invest first. Federal student loans at 4.5%, mortgages at 6.5% mortgage interest after deduction effects, low-rate auto loans — the long-run market return is reasonably expected to exceed the borrowing cost.

- 5% to 7%: split. Pay above the minimum on the debt while continuing to invest in tax-advantaged accounts. Reasonable people disagree about the exact split inside this band; what matters is that you are doing both, not one or the other.

The SAVE Plan Is Ending: July 1, 2026

For the 7.5 million federal student-loan borrowers currently in the SAVE plan, the planning landscape changes this summer. Starting July 1, 2026, you will receive a 90-day notice to select a legal repayment plan — Income-Based Repayment, Pay As You Earn, the new Tiered Standard, or the new Repayment Assistance Plan (RAP). If you do not choose, you auto-default into the Standard or Tiered Standard plan.

RAP, the new income-driven option launching the same day, shields on-time payers from runaway interest accrual — a meaningful improvement over the previous IDR plans for borrowers who keep up with payments. The choice between RAP and the Standard plan depends on your income trajectory and whether you are on a Public Service Loan Forgiveness path. For most federal-loan borrowers in early-career W-2 jobs, RAP is likely the right answer; for high-income earners who will be done with the debt quickly anyway, the Standard plan minimizes total interest. Don't drift into the auto-default; choose deliberately.

SECURE 2.0: Your Employer May Match Your Student Loan Payments

The SECURE 2.0 Act now allows employers to make matching contributions to your 401(k) based on your qualified student-loan payments, as if those payments were your own 401(k) contributions. If your employer offers this benefit, paying down federal loans effectively earns you the employer match without requiring out-of-pocket 401(k) contributions. This is dramatically underused — check with HR whether your plan offers it.

How to Start Investing

For most young professionals, the answer is uncomplicated: a broad-market index fund or an index-share-class target-date fund inside the 401(k) and IRA, contributions automated, rebalancing handled by the fund. The discipline is the boring part — buying every paycheck, holding through volatility, not chasing the latest narrative — and the math is the part most people undersell.

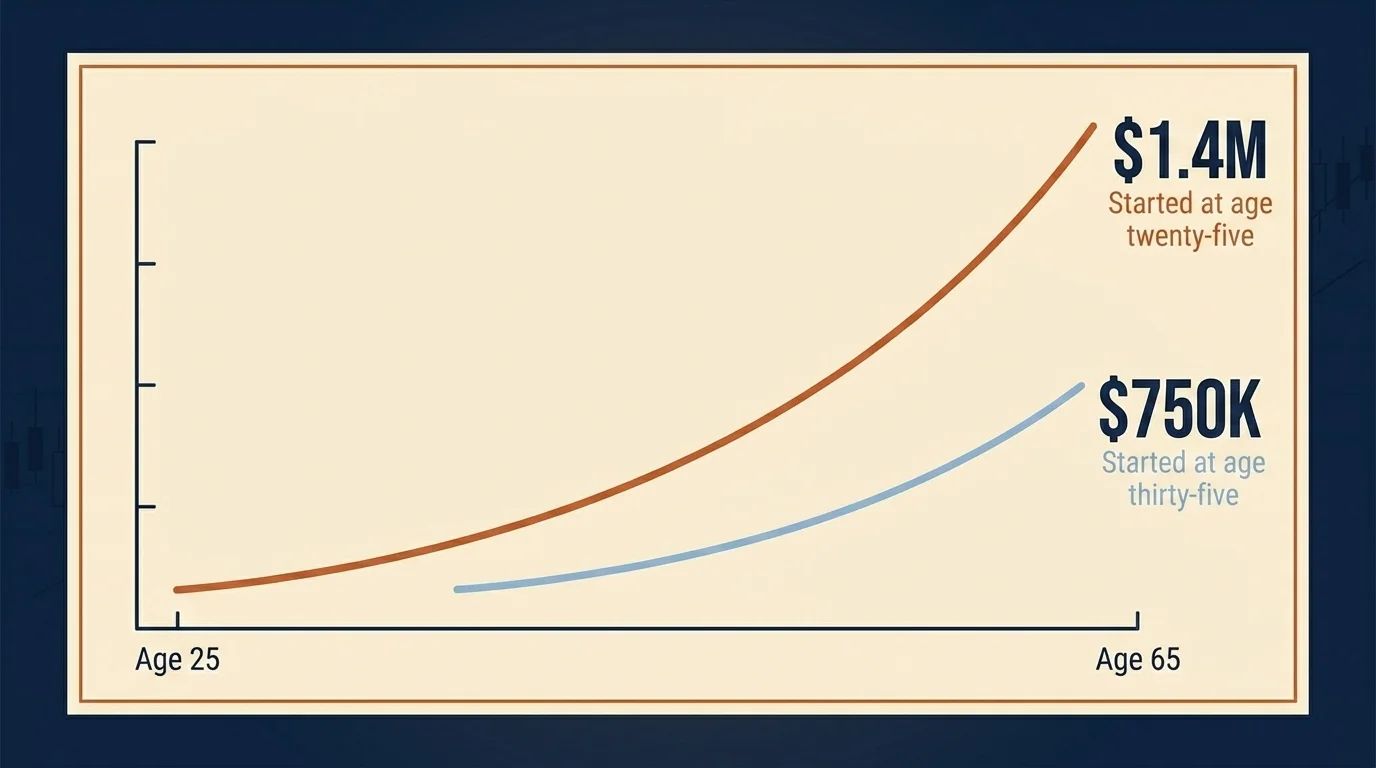

The compound interest you actually earn. A worked example with round numbers. Assume a 7% real return (roughly the long-run inflation-adjusted equity market return). $500/month contributed every month from age 25 to age 65 compounds to approximately $1.4 million. The same $500/month started at age 35 instead and continued to 65 compounds to roughly $750,000. Even doubling the contribution to $1,000/month from age 35 to 65 lands at roughly $1.0 million — still less than the $500/month from 25 case. Starting early is mechanically worth more than catching up later. This is the most important math in the article, and the reason "start now, even if the amount feels small" is the correct answer to most young-professional anxiety about investing.

Target-date funds: be careful about the expense ratio. Most 401(k) plans default young professionals into a target-date fund matched to a projected retirement year. Index-based TDFs run 0.08% to 0.15% expense ratios; actively-managed TDFs can exceed 0.60%. Over a 40-year horizon, a 50 basis-point fee difference compounds to roughly $200,000 less on a $500,000 portfolio. If your 401(k) offers an index-share-class TDF, choose it; if it offers only the actively-managed version, consider building the equivalent allocation from the underlying index funds in the plan menu.

The 2065 and 2070 glide paths still start at approximately 90% equity for early-career investors — that is the right exposure for someone with a 40-year horizon. Don't lower it because the most recent quarter felt scary.

App-first investing is now the norm. Sixty-five percent of Gen Z investors use investing apps, and 43% access robo-investment advice only — meaning a substantial share of the audience for this article has never had a human financial advisor. That is not bad in itself; a well-designed robo at low cost beats most do-it-yourself stock-picking. What matters is what the robo is doing under the hood (index funds at a reasonable all-in cost — typically 0.25%–0.40% with the management fee) and whether the platform will still be appropriate when your financial life gets more complex (multiple accounts, equity compensation, tax-loss harvesting needs).

Roth vs Traditional: The Bracket-Today-vs-Later Question

For most young professionals, Roth wins. The reasoning is the same logic I apply to Roth conversions for older clients, just in reverse: you are paying tax at the lower of two brackets — the one you are in today versus the one you are likely in later — and the lower bracket is almost always now.

A typical 25-year-old in the 22% federal bracket who expects to spend most of their career in the 24%–32% bracket is paying 22% tax on the contribution today in exchange for tax-free growth and tax-free withdrawals later, at a likely 24%–32% bracket. That arbitrage is worth real money over a 40-year horizon. For a young professional in the 12% bracket — early-career, part-time, or in a lower cost-of-living area — Roth is even more strongly preferred.

The bright lines I use at the desk:

- Federal bracket today is 24% or below, and you expect to peak higher → Roth wins. Pay tax now at the lower rate.

- Federal bracket today is 32% or above → Traditional 401(k) contributions earn you the deduction at the current high rate, which usually wins, especially if you expect to draw from the account during retirement at a meaningfully lower bracket.

- In the 24% bracket today, uncertain about peak earnings → Split contributions between Roth and Traditional. Hedge.

The new 2026 rule reinforces the Roth case. If your prior-year FICA wages exceed $150,000, your catch-up contributions to the employer plan must be Roth starting in 2026. This means a high earner who is on track for that threshold will be making Roth catch-ups in their fifties regardless — the only choice is whether to build the Roth habit (and the tax-free balance) earlier or later. Earlier wins.

What this analysis does not capture is your specific situation. Bracket arithmetic depends on filing status, state tax, deductions, and projected retirement-state residency. The rule of thumb above is correct on average. The specific answer is one I would work through with a planner who can see your actual return.

Where to Open Your First Brokerage

A brief commercial note before continuing: I do not recommend specific securities by ticker because the answer depends on your situation. I can comfortably comment on which brokerages and account types serve young professionals well, because that is a structural question.

- Fidelity — full-service, fractional shares, no-fee index funds with $0 minimums, integrated cash management, strong app. The defensible default for most young professionals.

- Vanguard — the cheapest index funds in the industry; the customer experience is more spartan than Fidelity's, which some readers prefer.

- Schwab — comparable to Fidelity on most dimensions; integrated checking account is well-regarded.

- Robinhood — app-first, fractional shares, very polished mobile experience, but historically thinner on retirement-account features and customer support.

- Betterment and Wealthfront — robo-advisors for hands-off investors; all-in cost typically 0.25% management fee plus the underlying fund expenses (~0.10%), so 0.35% total. Worth it for investors who would otherwise not invest at all; worth less for investors who will manage an index-fund portfolio themselves.

The default that fails almost nobody: open a Roth IRA at Fidelity, Vanguard, or Schwab; auto-contribute the full annual limit divided across monthly payments; invest 100% in a target-date fund matched to your retirement year, or in a 90/10 mix of broad-market US index plus broad-market international index plus a small bond sleeve. Set it up once, automate, leave it alone, increase the contribution when you get a raise.

Coast FIRE: How Early Saving Lets You Stop Saving

Coast FIRE is a milder version of the broader FIRE (Financial Independence, Retire Early) framework that I find more useful for young professionals than the original. The idea: if you front-load retirement saving aggressively for the first five to ten years of your career, the compounding math allows you to stop contributing later and still arrive at a comfortable retirement balance at a normal retirement age.

A 30-year-old who has $128,000 invested today, assuming a 7% real return, will reach approximately $1 million by age 65 without further contributions. At age 40, that target number jumps to approximately $252,000. The mechanic that earlier feels harsh and later feels almost impossible to catch up to is exactly the mechanic the compound-interest chart above showed: compounding rewards time in the market far more than amount contributed.

For young professionals: the highest-leverage years of your career for retirement saving are not your peak earning years. They are your first ten years, when the dollars contributed have 35-plus years to compound. Treat them accordingly. The benefit of Coast FIRE is not that you have to actually stop saving at 32; it is that you have the option to ratchet contributions down later if your priorities change — a sabbatical, a family, a career pivot — without breaking the long-run plan.

529s, HSAs, and Other Tax-Advantaged Wrappers

A short note on the accounts the original article spent time on. For most 25-year-old young professionals without children, the 529 is premature — the contribution should not displace your Roth IRA. The SECURE 2.0 Act now allows a limited rollover from a 529 to a Roth IRA after 15 years of seasoning (subject to the $7,500 annual Roth contribution cap and a $35,000 lifetime maximum from the 529), which makes the 529 marginally more flexible than it used to be, but does not change the priority order.

The HSA, for young professionals on an HDHP, is structurally the most tax-efficient account available — the triple tax advantage means contributions are deductible, growth is tax-deferred, and qualified medical withdrawals are tax-free. The disciplined use is to fund the HSA up to the $4,400 self-only / $8,750 family limit, invest the balance rather than letting it sit in cash, pay current medical expenses out of pocket where possible, and keep receipts for future reimbursement at retirement. Used this way, the HSA functions as an additional retirement account with better tax treatment than the 401(k) or IRA.

The Housing Reality

A brief, honest note on a topic that loads disproportionate emotional weight onto young-professional planning. Only 28% of millennials can afford a 20% down payment on a typical home, and 45% have enough for a 10% down. The first-time-buyer share of the market has fallen to 21% — the lowest level the National Association of Realtors has recorded — with median first-time-buyer age now 40. Eighty percent of Gen Z homeowners and 56% of millennial homeowners received financial help with the down payment.

The implication is not that you should give up on home ownership. The implication is that "save for a house" should be treated as a discrete decision — a specific dollar amount targeted at a specific timeline, parked in a HYSA earning 4.20%–5.00% APY, accumulated separately from your retirement contributions. It is not a default goal that absorbs every spare dollar. Some young professionals will buy at 32; some will buy at 42; some will rent indefinitely and channel the would-be down payment into a taxable brokerage. None of those is the wrong answer in itself — the wrong answer is letting the housing question consume the planning conversation without actually deciding.

What to Discuss with Your Planner

The framework above is approximately correct for the majority of young professionals I have advised over twelve-plus years of practice. It is not specifically correct for you. Some of the variables that matter most for the right answer are not visible to me from a blog post: your projected lifetime earnings curve, your state of residence (state tax matters), your filing status and any planned changes, your employer's specific match formula and HSA contribution, whether you have equity compensation, your specific student-loan portfolio and PSLF status, your projected family situation, and your honest risk tolerance under drawdown.

If you have those facts in front of you and the math feels straightforward, the framework above will get you most of the way there: capture the matches, kill the high-rate debt, build the HYSA emergency fund, max the Roth IRA, automate everything, increase contributions when you get raises, and let compound interest do the work. If any of the variables I named above are unusual — equity compensation, a non-standard career arc, family transitions, an aggressive house-buying timeline — the framework breaks in specific ways that are worth thinking through with someone who can see your actual situation.

A few specific things to ask your planner about, sorted by life stage: in your first year of work, ask about the employer-match formula and the vesting schedule; in years two through five, ask about Roth conversion ladders if you have any traditional 401(k) balances from past jobs; if you are above the Roth IRA income phase-out by year four or five, ask about the backdoor Roth process; if you have federal student loans, ask whether your employer offers SECURE 2.0 student-loan matching; if you are accumulating equity compensation, ask about Section 83(b) elections and AMT exposure; in your thirties, start asking about tax-efficient asset location across your tax-deferred, tax-free, and taxable accounts.

Boring, but load-bearing. Start now, automate everything, and stay out of your own way for thirty years. The math takes care of the rest.

This article is for educational purposes only and is not individual financial advice. Tax brackets, contribution limits, plan rules, and student-loan programs change annually, sometimes mid-year — always verify current numbers and rules from the IRS, your plan administrator, and the U.S. Department of Education before making a decision. Consult a licensed financial advisor and a tax professional for guidance matched to your specific situation, including the variables your planner can see and a blog post cannot.

Frequently Asked Questions

Run the first-paycheck waterfall in order: contribute enough to your HSA and 401(k) to capture every dollar of employer match (free money), kill any debt above ~7% interest, build a one-month emergency-fund layer in a HYSA at 4.20–5.00% APY, then prioritize a Roth IRA before maxing the 401(k).

Target 15–20% of gross income into long-term savings/retirement once the employer match is captured. Start with the 1-month emergency-fund layer, then the 401(k)-match minimum, then build to 3 months of expenses in a HYSA, then max the $7,500 Roth IRA.

If your federal bracket today is 24% or below and you expect to peak higher, Roth almost always wins — pay tax now at the lower rate. Above 32%, the Traditional deduction usually wins. Starting in 2026, if your prior-year FICA wages exceed $150,000, your age-50+ catch-up contributions to employer plans must be Roth anyway.

1 month to start; 3 months once stable (dual income, salaried, no dependents); 6 months for single income / one earner / mortgage; 9 months for self-employed or 1099 income. Park it in a HYSA earning 4.20–5.00% APY, not a traditional savings account.

Use the 7% bright line. Loans ≥7% interest → pay down before investing beyond the employer match. Loans <5% → invest first; the long-run market return beats the interest cost. Federal loans 5–7% → split. If your employer offers a SECURE 2.0 student-loan match, take it — it counts your loan payments toward the match without 401(k) contributions of your own.

SAVE is being unwound. Starting July 1, 2026, the 7.5 million SAVE-enrolled borrowers will receive a 90-day notice to choose a legal repayment plan — otherwise they auto-default to the Standard or new Tiered Standard plan. The new Repayment Assistance Plan (RAP) launches the same day and is the new income-driven option, with built-in interest-runaway protection for on-time payers.

Allocate 50% of after-tax income to needs (rent, utilities, groceries, transport, minimum debt payments), 30% to wants (dining, travel, entertainment), and 20% to savings + extra debt payoff. On a $5,000/mo take-home: $2,500 needs / $1,500 wants / $1,000 savings + debt-payoff. Pair with automated transfers on payday to remove the decision.

Fidelity for full-service plus fractional shares and integrated cash management; Schwab for the integrated checking account; Vanguard for low-cost-index purists; Robinhood for app-first investors; Betterment or Wealthfront for hands-off robo management. Whichever you pick, default to a broad low-cost index fund or an index-share-class target-date fund with a 0.08–0.15% expense ratio.

Yes — front-load retirement saving for 5–10 years and the compounding math allows you to ratchet contributions down later. A 30-year-old with $128,000 invested today reaches ~$1M by age 65 at a 7% real return without further contributions. At age 40, that number jumps to ~$252,000. The first ten years of your career are the highest-leverage years for retirement saving.

For 2026: 401(k) elective deferral $24,500 (up from $23,500); IRA $7,500 (up from $7,000); 401(k) catch-up (50+) $8,000; new super catch-up (ages 60–63) $11,250; IRA catch-up $1,100. HSA self-only $4,400; family $8,750. Roth IRA income phase-outs: single $153,000–$168,000; MFJ $242,000–$252,000.