The Rise of ESG Investing: Ethics Meets Profit

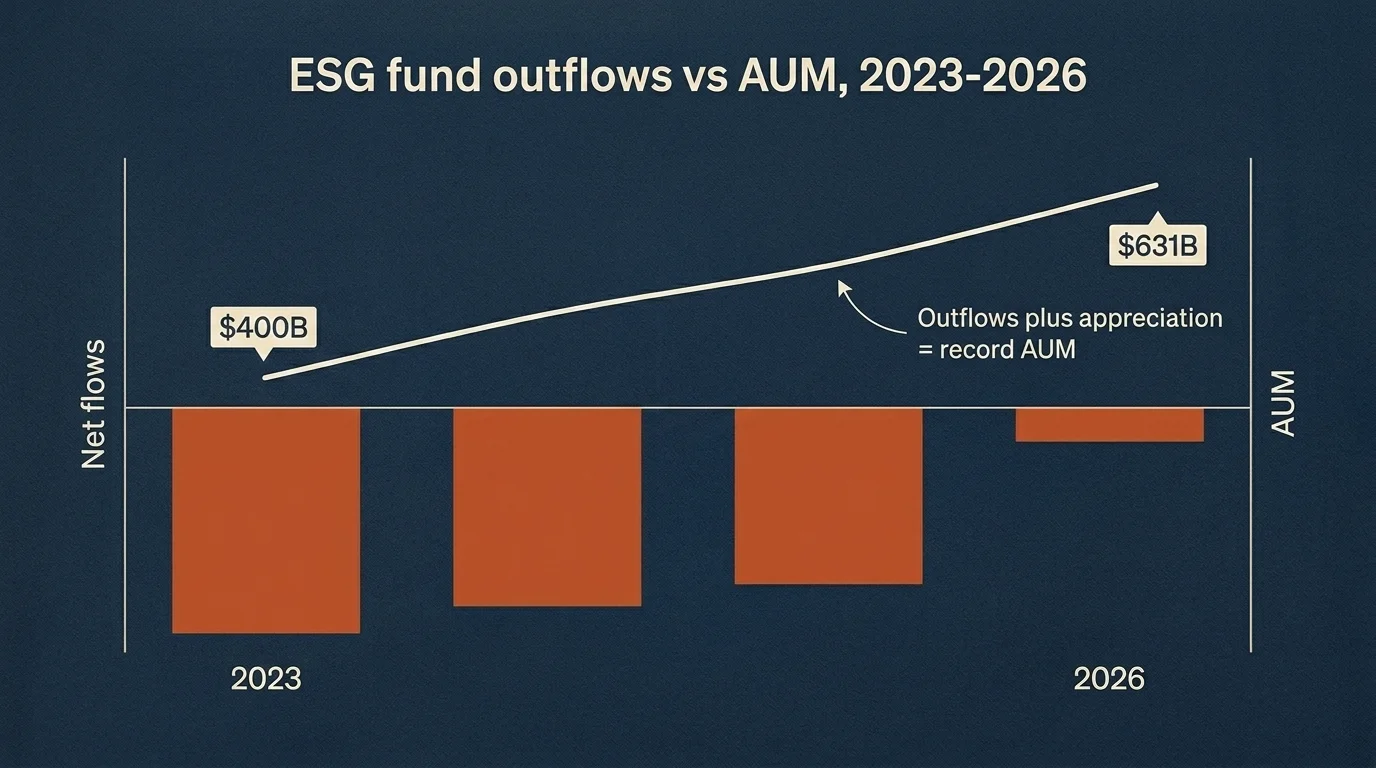

The number worth opening with on ESG investing in 2026 is the paradox: in 2025, U.S. sustainable funds saw $21 billion in net outflows — the third consecutive year of outflows, the worst on record since Morningstar began tracking. In the same year, U.S. sustainable fund assets under management hit an all-time high.

What that combination actually measures is a market in which existing investors are riding stock-market appreciation while marginal investors have stopped allocating new capital under the ESG label. What it does not tell us is whether the strategy has stopped working — that is a separate question, and the answer there is more interesting. In H2 2025, 89% of sustainable funds delivered positive returns versus 84% of traditional funds, and seven-year sustainable fund returns still beat traditional benchmarks even through the volatility of 2022.

The honest reading, and the analytical thesis of this guide: ESG investing in 2026 is not dead. It has been substantially renamed, the regulatory architecture supporting it has been gutted on both sides of the Atlantic, and the marketing language around it has shifted to "transition," "responsible," and "sustainable" to dodge the backlash. The underlying capital — and most of the underlying strategy — remains. This is not a 2021 ESG explainer. It is a 2026 reckoning.

What ESG actually means (and why the label is fading)

ESG — Environmental, Social, and Governance — is an investment framework that integrates three sets of non-financial-but-financially-material factors into security analysis. Environmental: a company's energy use, emissions, water management, waste, and resource intensity. Social: how it manages employees, suppliers, customers, and the communities it operates in. Governance: board composition, executive pay, audits, internal controls, shareholder rights.

The framework can be implemented across a spectrum. Pure ESG integration uses the factors as additional risk inputs in conventional analysis — the analyst still cares about cash flows, ROIC, and valuation, but adds ESG as a lens for tail risk and long-horizon durability. Negative screening excludes specific industries (tobacco, weapons, fossil fuels) on values grounds. Best-in-class weights toward sector leaders on ESG metrics. Thematic invests directly into transition themes (clean energy, water, resource efficiency). Impact targets measurable outcomes alongside returns.

The label "ESG" has been used loosely to cover all of those approaches, which is part of why the term lost traction. An investor buying a thematic clean-energy ETF is doing something materially different from an investor whose actively managed fund integrates ESG factors as risk inputs. Conflating them under one acronym was a marketing convenience that the regulatory and political environment of 2024-2026 finally broke.

The search-trend evidence makes the rebrand visible in real time. "ESG investing" U.S. search volume is down 47% year-over-year. "Responsible investing" is up 182% month-over-month and 129% quarter-over-quarter. "Sustainable investing" is up 116% quarterly. "Impact investing" has flattened (-19% yearly, the mildest decline in the cluster). The strategy is migrating to successor labels faster than any of them can fully consolidate. That is a marketing event, not an investment event.

The 2025–2026 regulatory timeline

The institutional and regulatory shift that drove the rebrand is the part most retail-facing ESG content underplays. The dates and specifics matter for any investor trying to understand where the framework actually stands today.

- March 2024 — SEC finalizes its climate-related disclosure rule. Public companies would have been required to report material climate risks and, in some cases, Scope 1 and 2 greenhouse gas emissions.

- April 2024 — Eighth Circuit stay. Multiple state attorneys general challenged the rule; the Eighth Circuit issued a stay pending litigation.

- February 2025 — SEC freezes the rule. Acting Chair Mark Uyeda paused the rule's defense.

- March 27, 2025 — SEC ends defense. The Commission voted to end its defense of the climate-related disclosure rules in the Eighth Circuit. The agency simultaneously withdrew 14 Biden-era proposals including the ESG fund disclosure rule and the shareholder proposal reform. The court could still rule independently, but the agency's institutional position was no longer behind the rule.

- March 2025 — Florida AG opens investigation into proxy advisory firms ISS and Glass Lewis over ESG and DEI voting policies.

- December 2025 — EU Omnibus deal. The Council and Parliament struck a deal to substantially scale back the Corporate Sustainability Reporting Directive (CSRD) and Corporate Sustainability Due Diligence Directive (CSDDD).

- February 26, 2026 — Directive 2026/47 published. Entered into force March 18, 2026. CSRD threshold raised to 1,000+ employees AND €450M turnover (cuts in-scope companies by approximately 85%). CSDDD threshold raised to 5,000+ employees AND €1.5B turnover (cuts approximately 70%); compliance deferred to July 2029 with the climate transition plan obligation removed. The European Sustainability Reporting Standards (ESRS) draft cuts mandatory data points from approximately 1,100 to approximately 430.

- 2025 cumulative — 11 anti-ESG bills passed across U.S. states. Approximately 16 states (Alabama, Arkansas, Florida, Georgia, Idaho, Indiana, Kansas, Kentucky, Louisiana, Montana, North Carolina, North Dakota, Ohio, South Carolina, Tennessee, Texas) now have rules limiting ESG investing in public funds. These laws restrict ESG criteria in public pension and state contracting decisions. They do NOT restrict individual investor choices.

The pattern is consistent: the formal regulatory architecture supporting ESG-as-a-disclosure-regime has been substantially rolled back in both the U.S. and EU between early 2025 and early 2026. What remains is the underlying market practice — the integration of ESG factors into analysis where they affect risk and return — which is now operating under different labels because the original label has become a political liability. The strategy is unchanged. The packaging is.

The performance reckoning: three years of outflows, record AUM

The performance story is the part that most ESG content cherry-picks in either direction. The honest version, told with the actual numbers:

- 2025 was the worst year on record for U.S. sustainable fund flows since Morningstar began tracking — $21 billion in net outflows, with $4.6 billion withdrawn in Q4 2025 alone and $55 billion in net outflows from the global sustainable fund universe in Q3 2025. It was the third consecutive year of outflows.

- Despite three years of outflows, U.S. sustainable fund AUM reached an all-time high at year-end 2025 — driven by stock-market appreciation rather than new flows. The math: existing assets compounded faster than redemptions could exit them. That is a meaningful structural fact about the investor base. Long-horizon holders are not selling; the marginal flow is just no longer arriving.

- Total ESG mutual fund and ETF AUM as of February 2026 was $631.03 billion, up $2.00 billion month-over-month, with $2.00 billion in net outflows in February alone. The pattern has continued into 2026 — appreciation outpacing outflows on a net AUM basis, but flows still negative.

On performance:

- In H2 2025, 89% of sustainable funds delivered positive returns versus 84% of traditional funds. Seven-year sustainable fund returns still beat traditional funds through the 2022-2024 volatility window.

- Several thematic ESG ETFs delivered 30–67% YTD returns in 2026, though with elevated volatility. Broad ESG ETFs have largely matched conventional equivalents.

- The narrative of "ESG underperformance" that hardened during 2022 was real — energy stocks surged on the post-COVID supply shock, and ESG funds were structurally underweighted in the sector that drove the S&P that year. The narrative of "ESG outperformance" that had hardened pre-2022 was also real, on a longer-horizon look-back. Both were partial readings of a partial dataset. The longer-horizon record is closer to "comparable to broader benchmarks at lower fossil-fuel exposure," which is what the integration thesis actually predicted.

The honest version of the performance question, the one I would put to a new analyst: ESG-aligned portfolios, on average, have delivered risk-adjusted returns comparable to or slightly better than broader benchmarks over rolling seven-year windows. They underperform during commodity-driven equity rallies and outperform during periods of regulatory tightening or company-specific governance failures. Whether the trade is worth it for any specific household depends on that household's tolerance for the underperformance windows and its values around capital deployment. Sizing belongs to a planner.

ESG vs SRI vs Impact vs Sustainable vs Responsible — disambiguation

The terminology is genuinely confusing because the labels were applied loosely and have been rebranded under pressure. The differences below are real even when the marketing blurs them.

| Term | What it screens for / targets | Typical fund example category | How it differs from ESG |

|---|---|---|---|

| ESG | Integrates E/S/G factors as risk inputs in financial analysis | Broad ESG ETFs (e.g., ESGV, ESGU, SUSL) | The umbrella term. Now politically loaded; usage declining. |

| SRI (Socially Responsible Investing) | Negative screening — excludes specific industries on values grounds | Faith-based funds, tobacco-free funds | Older label, more values-based, less analytically integrated |

| Impact Investing | Targets measurable positive outcomes alongside financial returns | Community development funds, green bonds, microfinance | Outcome-focused, often illiquid, often institutional |

| Sustainable Investing | Broad umbrella for environmental + governance-aligned investing | Sustainable equity funds, climate transition funds | The current rebrand of choice; broader than ESG, less politicized |

| Responsible Investing | Catch-all for E/S/G consideration; the fastest-rising successor term | "Responsible" or "transition" labelled funds | Rapidly replacing ESG in fund naming and investor surveys |

| Transition Investing | Targets companies actively transitioning to lower-emission operations | Climate transition ETFs, BlackRock's preferred frame | BlackRock's chosen successor; focuses on companies in motion, not just leaders |

The practical implication: a fund labeled "responsible" in 2026 may be doing exactly what an "ESG" fund was doing in 2021. A fund labeled "transition" may be doing something more specific — explicitly targeting companies on a credible path to lower emissions, not necessarily today's ESG leaders. Read the prospectus. The label is downstream of the strategy, not the other way around.

How ESG ratings actually work (and why agencies disagree)

This is the part most retail-facing ESG content skips, which is unfortunate because it explains a lot of the confusion in the space.

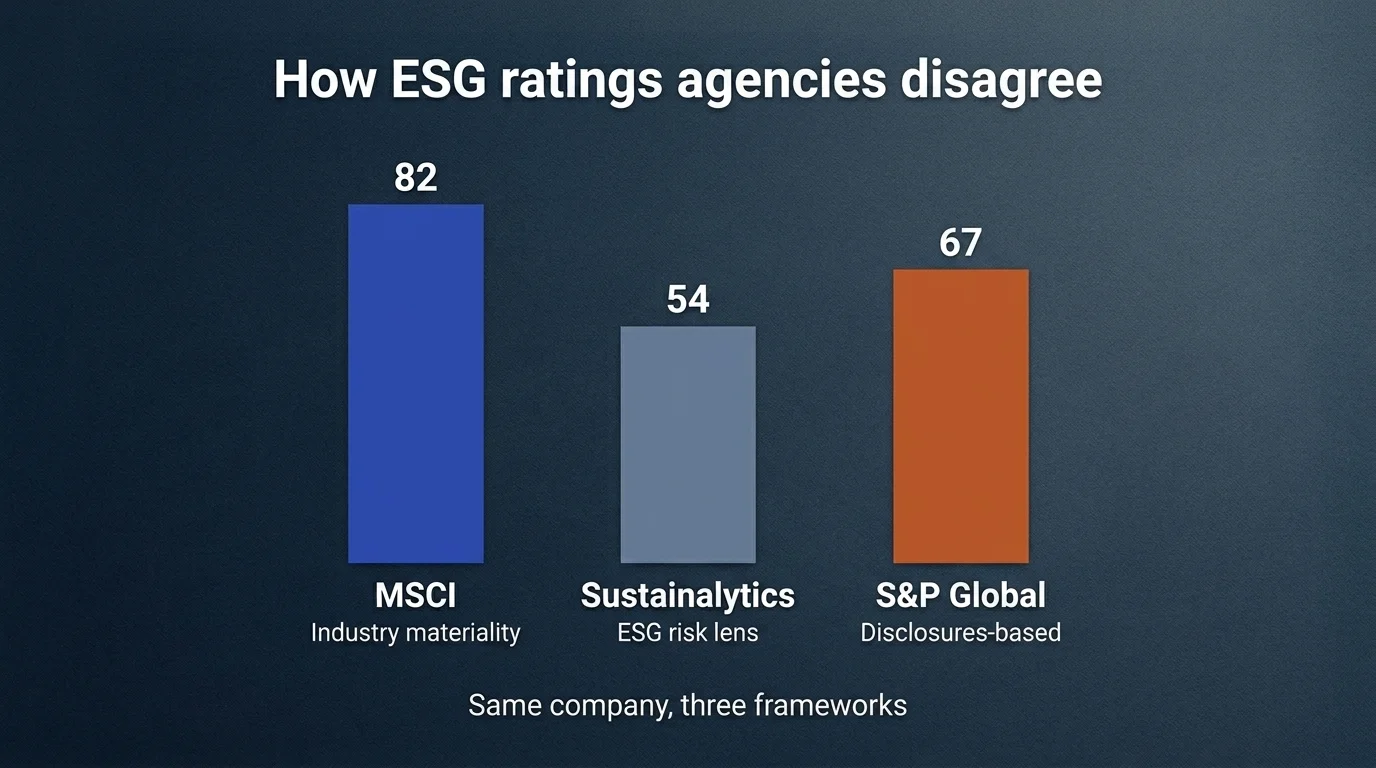

The major ESG ratings agencies — MSCI, Sustainalytics (a Morningstar company), S&P Global ESG Scores, Moody's ESG, ISS — each apply their own methodology to score companies on ESG factors. The methodologies differ in three important ways:

- What they weight. MSCI weights "industry materiality" — which factors matter most for a given sector. Sustainalytics scores "ESG risk" with a downside lens. S&P Global emphasizes corporate disclosures and policies. The same company can score very differently depending on which framework's weights are applied.

- How they handle data gaps. When companies don't disclose, agencies must impute. Some impute conservatively, some lean on third-party data, some use proxy industry averages. Imputation choices materially affect the score.

- The reference universe. Some agencies score within sector (best-in-class), others score against a global universe. A high MSCI score in the energy sector means something different from a high MSCI score in the tech sector.

The Tesla example is the classic illustration. For years, Tesla scored relatively high on MSCI's framework (which weights low-emission products favorably for an automaker) and relatively low on S&P Global's (which weighted governance and labor-relations factors more heavily). Same company, two defensible methodologies, very different scores. An investor screening for "ESG leaders" gets different portfolios depending on which agency they trust.

This is not a flaw to fix. It is a feature of the framework. ESG ratings are inherently model outputs based on judgment calls about what to weight and how to handle missing data. They are useful as one input among several. They are not, and will never be, like credit ratings — which are themselves model outputs but converge tightly because the underlying data is more standardized.

The practical advice for any household using ESG ratings to inform investment decisions: read at least two agencies' scores, look at the underlying methodology, and treat the rating as a starting point for analysis rather than a conclusion.

Named ESG funds and what they actually screen for

The publicly traded names most discussed in retail ESG investing fall into a few clear categories. Listing them is descriptive, not a recommendation. Sizing any of them in your portfolio belongs to a licensed financial advisor who knows your full situation.

- Broad ESG ETFs — funds that hold ESG-screened versions of broad-market indices. Common names include ESGV (Vanguard's broad ESG-screened U.S. equity ETF), ESGU (iShares MSCI USA ESG Optimized), and SUSL (iShares MSCI USA ESG Leaders). The mechanics differ — some apply best-in-class screens within sectors, some apply tilted weighting by ESG score, some apply negative screens for specific industries. Read the prospectus.

- Thematic clean-energy and transition ETFs — funds focused on specific environmental themes. ICLN (iShares Global Clean Energy), TAN (Invesco Solar), QCLN (First Trust NASDAQ Clean Edge Green Energy). These are concentrated, sector-specific bets rather than diversified ESG exposure. Their volatility is substantially higher than a broad ESG ETF.

- Active ESG mutual funds — actively managed funds that integrate ESG into their security selection. The Parnassus family (especially Parnassus Core Equity) is among the longest-running U.S. examples; Calvert Equity Fund is another. Active management adds both manager-skill upside and manager-decision risk.

- Faith-based / values-based screens — older SRI-vintage funds that exclude specific industries on values grounds (tobacco, weapons, gambling, fossil fuels, alcohol). These are values-driven rather than analytically integrated; the screening criteria are usually well-documented on the fund's site.

A 2026 honest observation: many of the broad ESG ETFs hold portfolios that overlap substantially with broad-market indices. The tracking error against the S&P 500 is usually in the low-single-digit percentage points. If your goal is values-aligned investing without dramatic factor exposure, this is probably what you want. If your goal is a meaningfully different portfolio that tilts toward ESG leaders or environmental themes, the thematic funds give you that — but at the cost of higher concentration and higher volatility.

BlackRock dropped ESG: what they're calling it now

The rebrand visible in fund naming is the most concrete evidence that the strategy is migrating rather than dying. BlackRock removed "ESG" from the names of more than 50 European strategies covering approximately $51 billion in AUM by 2025. Larry Fink's 2025 and 2026 chairman's letters omit "ESG", "climate change", "sustainability", and "DEI" entirely — replaced with "energy pragmatism", infrastructure investment, and asset democratization framing.

What BlackRock is doing under the new labels is, in many cases, a meaningful refinement of what it was doing under the old. "Transition investing" — the firm's preferred successor frame — focuses specifically on companies actively transitioning to lower-emission operations rather than today's ESG leaders. That is a defensible distinction with different portfolio implications: a "transition" portfolio holds higher-emission companies in motion, not just current leaders. Whether that is a better or worse investment thesis depends on your view of the credibility of corporate transition plans, which is itself an open empirical question.

The lesson for investors: when a major asset manager renames $51 billion of strategies, the strategies are usually not changing as much as the names. Read the prospectus, compare the holdings to the previous label, and decide based on what is actually in the portfolio.

How to invest ESG-style in 2026

Practical guidance for a U.S. household trying to apply some version of ESG-aligned investing in the current environment:

- Inside a 401(k), your fund menu may or may not include ESG-screened or sustainable-labeled options. If it does, evaluate them on the same criteria as any other fund — expense ratio, underlying index methodology, holdings overlap with your existing allocation. If your plan doesn't offer one and you want exposure, the simplest workaround is a self-directed brokerage option (if your plan allows) or directing the ESG-aligned portion of your portfolio to your IRA or taxable accounts where the fund universe is unrestricted.

- Inside an IRA, the entire fund universe is available to you. The constraint is usually the brokerage's fund availability and your willingness to research. Most major brokerages (Vanguard, Fidelity, Schwab) offer their own and competing ESG funds with comparable expense ratios.

- Inside a taxable brokerage, the same flexibility applies, with the additional consideration that fund turnover affects after-tax returns. Some active ESG funds have higher turnover than passive equivalents, which can erode after-tax performance materially in a high-tax bracket.

- If your state has an anti-ESG law, those laws restrict ESG criteria in public pension and state-contract decisions. They do NOT restrict individual investment choices. Your IRA, your 401(k), and your taxable brokerage are not subject to state-level ESG restrictions. The political signaling has been louder than the practical reach for retail.

- Watch the IRMAA threshold and tax-cost trade-offs the same way you would on any allocation decision. If implementing an ESG-aligned strategy requires meaningful realized gains in a taxable account, the after-tax cost of the switch may exceed the marginal benefit of the ESG tilt. Sequence the move through tax-advantaged accounts first.

The practical reality of 2026: your access to ESG-style investing as a U.S. household is not meaningfully different than it was in 2021. The fund options are similar (under different names), the brokerages still offer them, and your personal account choices remain unrestricted. What has changed is the marketing language and the regulatory disclosure architecture above the fund level.

What would change my view on the rebrand thesis

In keeping with how I approach any analytical thesis: here is the single variable that, if it changed, would invalidate the framework above.

The framework rests on the assumption that the underlying capital flows and investment practice are continuing under different labels. If U.S. sustainable fund AUM begins to decline in absolute terms — not just experiencing outflows masked by appreciation — that would indicate the strategy itself is contracting, not just the marketing. As of February 2026, AUM is still rising on appreciation; outflows are negative but smaller than market gains. If outflow scale exceeds market gains for two consecutive years, the "rebrand only" thesis weakens and the "actual contraction" thesis strengthens. I am watching the year-end 2026 ICI and Morningstar numbers for this.

The second variable is regulatory direction. If the SEC or EU re-establishes climate or ESG disclosure mandates within the next 18 months, the rebrand-as-political-defense thesis weakens — the strategy did not need a rebrand because the regulatory environment is back to favoring it. As of April 2026, this looks unlikely in the near term. But political environments change, and the investment thesis has to be re-run when they do.

That is the state of ESG investing in 2026 as I would walk a new analyst through it on day one. None of it is individual financial advice. All of it is starting material for the conversations a household should have with the licensed advisor who can translate it into a plan for their specific situation.

Frequently Asked Questions

No, but the label is fading. U.S. sustainable funds saw a third consecutive year of outflows ($21 billion in 2025), yet AUM hit a record high on stock-market appreciation, and 89% of sustainable funds delivered positive returns in H2 2025 versus 84% of traditional funds. The strategy is migrating to 'responsible,' 'sustainable,' and 'transition' framings — substantially the same investments under different names. The political backlash has reshaped the marketing and disclosure architecture more than the underlying capital allocation.

In February 2025, acting SEC Chair Mark Uyeda paused the rule. On March 27, 2025, the Commission voted to end its defense of the rule in the Eighth Circuit, effectively withdrawing it. The SEC also withdrew 14 other Biden-era proposals including the ESG fund disclosure rule and shareholder proposal reform. The Eighth Circuit could still rule independently on the underlying litigation, but the agency's institutional position is no longer behind the rule.

Mixed but trending comparable on a risk-adjusted basis. In 2025, 89% of sustainable funds delivered positive returns versus 84% of traditional funds, and seven-year sustainable fund returns still beat traditional benchmarks. Several thematic ESG ETFs are up 30-67% YTD in 2026, though with elevated volatility. Broad ESG ETFs have largely matched or modestly beaten conventional peers in 2026. The 2022 ESG underperformance during the energy spike was real; the longer-horizon record is closer to comparable returns at lower fossil-fuel exposure.

ESG integrates environmental, social, and governance factors into financial analysis as risk inputs. SRI (socially responsible investing) screens out specific industries (tobacco, weapons) on values grounds. Impact investing targets measurable positive outcomes alongside returns, often through illiquid instruments. Sustainable investing is the current umbrella rebrand. Responsible investing is the fastest-rising successor term (+182% monthly searches in 2026). The underlying strategies overlap substantially; the labels increasingly do not.

Yes, for personal accounts (IRA, taxable brokerage, employer 401(k)). State anti-ESG laws — which now exist in approximately 16 states including Texas and Florida — restrict ESG criteria in public pension and state-contract decisions, not individual investment choices. Your broker continues to offer ESG ETFs and mutual funds regardless of your state's stance, and your personal account holdings are not subject to state-level restrictions on retail investors.

Check Out These Related Articles

Finance Mentor vs Sponsor: What Actually Compounds a Career

Youth-Led Financial Revolutions: Crowdsourcing as a Catalyst for Investment Innovation

Red vs. Blue: The Battle of Colors in Investment Marketing