Rebalancing Your Investment Portfolio: The Key to Sustainable Growth

The number worth opening with on how to rebalance portfolio drift in 2026 is not the cadence and not the threshold. It is the after-tax alpha figure: Vanguard's July 2024 research puts the annual after-tax return uplift from disciplined tax-loss harvesting paired with rebalancing at 0.45% to 0.95% per year, with a broader range up to 1.27% under the firm's Advisor's Alpha framework. What that number actually measures is the cumulative after-tax return improvement from running rebalancing and tax-loss harvesting as a single integrated practice rather than two separate tasks. What it does not tell us is whether that range applies to any specific household — the variance is wide depending on volatility, contribution cadence, account mix, and tax bracket.

The reason to lead with that figure is that it is the largest analytical fact in the rebalancing literature that does not appear on Vanguard's own consumer-facing rebalancing page. It is also the fact that should reframe how a thoughtful investor approaches the question. The traditional rebalancing question is "how often" and "at what threshold." The modern question is "how do I rebalance and harvest losses in the same operation, with the right account-type sequencing, and what is the after-tax outcome." The first question is a mechanic. The second is the actual strategy.

This is a guide to how to rebalance your portfolio in 2026 — when to do it, the drift mechanics that drive the trigger, a worked dollar example through a real time window, the methods compared with their actual trade-offs, the 401(k) rebalancing rules that most retail content gets wrong, the integration with tax-loss harvesting, and the manual-vs-robo decision math.

How often should you rebalance your portfolio?

The answer that has hardened across institutional research over the last two years: annually, with a threshold-based override.

Vanguard's 2026 guidance now explicitly identifies annual rebalancing as optimal for most investors, with monthly and quarterly framed as too frequent (transaction-cost and tax friction without commensurate return improvement) and biennial as too infrequent (drift accumulates beyond intended risk tolerance). The case for annual is structural: it captures the bulk of the diversification benefit, aligns with the tax-year calendar, and matches most investors' tolerance for maintenance work.

The threshold override layers on top: rebalance early, regardless of where you are in the calendar, if any allocation drifts more than 5 percentage points from its target. This is the 5% rule, and it is the dominant institutional standard. Vanguard's canonical example is a 70/30 portfolio drifting to 76/24, which is a 6 percentage-point deviation in equities — past the 5pp threshold and a trigger.

The institutional rebalancing automation that retail investors interact with has moved further. Wealthfront monitors allocations daily and triggers rebalances when drift exceeds threshold; Guideline triggers 401(k) auto-rebalance at 5% drift. Daily monitoring is not the same as daily trading — the system checks daily and acts only when the threshold is breached. For DIY investors, weekly or monthly checking is more than sufficient given annual cadence as the baseline.

The four inputs that actually drive a household's rebalancing answer:

- Target allocation. What is the portfolio supposed to look like.

- Current drift. How far has it moved from target, in percentage-point terms.

- Tax wrapper. Is this a 401(k)/IRA (no current tax cost) or a taxable brokerage account (15-23.8% capital gains plus state tax on realized gains).

- Cash flow availability. Can incoming contributions or dividends close the drift without selling.

The first three determine what the math says. The fourth determines how to execute it without paying more tax than necessary.

The mechanics of drift: what 5 percentage points actually means

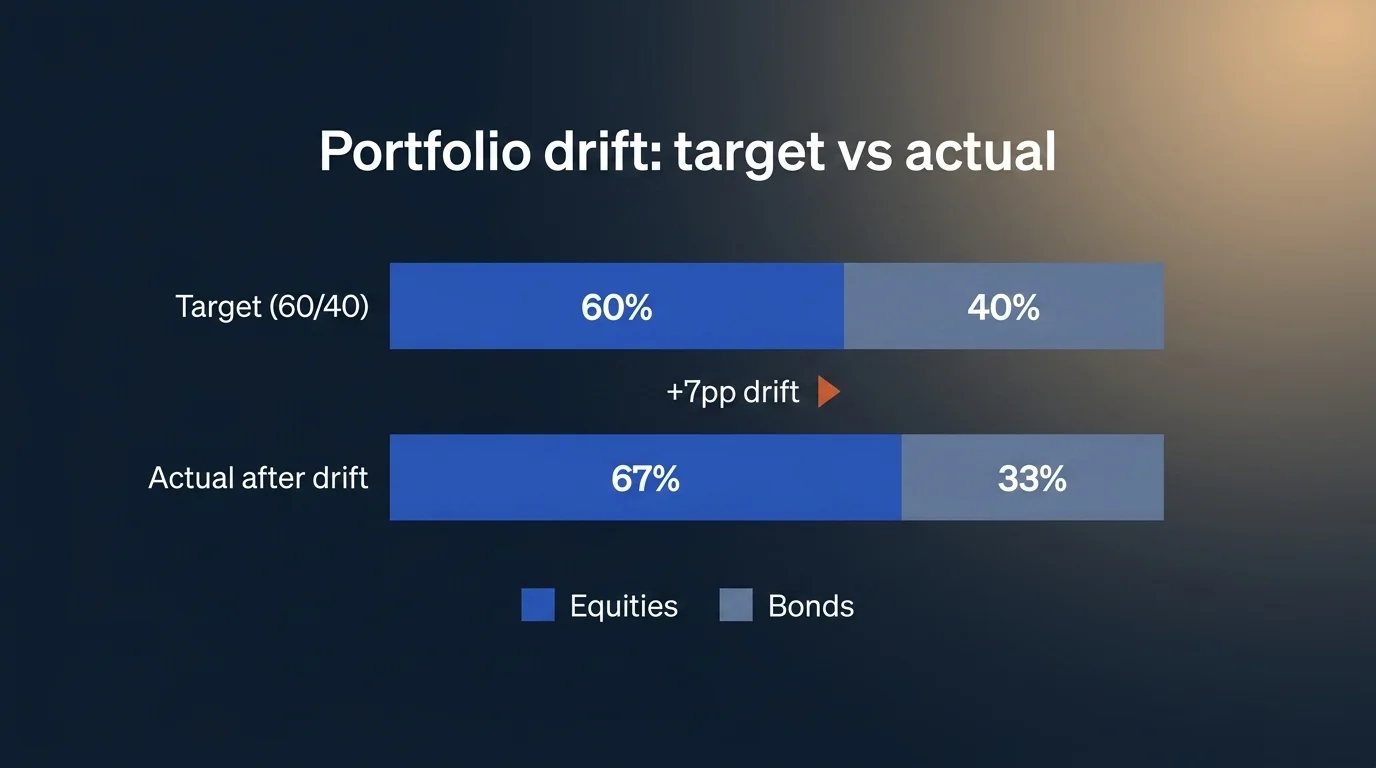

Drift is the difference between current allocation and target allocation in percentage-point terms. A 60/40 portfolio that drifts to 65/35 has 5 percentage points of equity drift. A 60/40 portfolio that drifts to 67/33 has 7 percentage points of drift — past the threshold and clearly a trigger. The same 7-percentage-point absolute drift could come from a strong equity rally, a fixed-income drawdown, or both at once.

Two important nuances most retail explainers skip:

- Absolute vs relative drift. A 5-percentage-point drift on a 60% allocation is roughly 8% relative. A 5-percentage-point drift on a 5% allocation would be 100% relative — the position has doubled. The institutional refinement is the 5/25 rule: rebalance when the drift exceeds 5 percentage points absolute OR 25% relative, whichever triggers first. Smaller positions are governed by the relative rule. Larger positions by the absolute rule.

- Drift is not symmetrical in cost. Drift in a tax-advantaged account costs nothing to correct — sell, rebuy, done. Drift in a taxable account triggers capital gains. Two portfolios with identical drift profiles can have very different rebalancing costs depending on where the drifted assets sit.

The drift threshold is the trigger. The mechanics of how to close it are the rest of the work.

A worked example: $500K 60/40 portfolio drifting through 2024–2026

Abstract examples teach less than a worked one. Consider a hypothetical $500,000 portfolio at the start of January 2024, allocated 60% equities ($300,000) and 40% bonds ($200,000). Inside the equity sleeve, $200,000 sits in a tax-advantaged account (an IRA holding a total-market index ETF) and $100,000 sits in a taxable brokerage account (a similar ETF). Inside the bond sleeve, $200,000 sits in the IRA.

Through 2024 and into early 2026, equities outperformed bonds. The 2025 tariff drawdown took equities down nearly 20% from mid-February through early April 2025 before recovering — a round-trip — while bonds delivered modest positive returns. By April 2026, the portfolio looks roughly like this:

| Sleeve | Account | Jan 2024 value | Apr 2026 value | Apr 2026 % |

|---|---|---|---|---|

| Equity (broad) | IRA | $200,000 | ~$285,000 | ~50.0% |

| Equity (broad) | Taxable | $100,000 | ~$143,000 | ~25.1% |

| Bonds | IRA | $200,000 | ~$210,000 | ~36.8% |

| Total | $500,000 | ~$638,000 | 100% |

Equity allocation has drifted from 60% to ~75% (15 percentage points absolute, well past the 5pp trigger). Bond allocation has drifted from 40% to ~33%. The portfolio is meaningfully more equity-heavy than the target risk profile.

The rebalance to restore 60/40 from a $638,000 base requires:

- Target equity at 60%: $382,800. Current equity: $428,000. Reduce equity by ~$45,200.

- Target bonds at 40%: $255,200. Current bonds: $210,000. Increase bonds by ~$45,200.

The right execution sequence is account-type-first. The IRA holds $285,000 in equity; sell ~$45,200 of the IRA equity and buy bonds. Tax cost: zero. The IRA sale realizes no current taxable gain.

Compare that to the wrong sequence — selling from the taxable equity position. The taxable equity has appreciated from $100,000 to ~$143,000 over the period; selling $45,200 of it would realize approximately $13,500 in long-term capital gains. At a 15% federal long-term rate plus the 3.8% Net Investment Income Tax for higher earners, that is up to $2,500 in unnecessary tax cost on a single rebalance — money that could have stayed compounding if the IRA had been used instead.

This is the entire reason "rebalance in tax-advantaged accounts first" is the 2026 consensus framing. The drift was identical across accounts. The cost of correcting it was not.

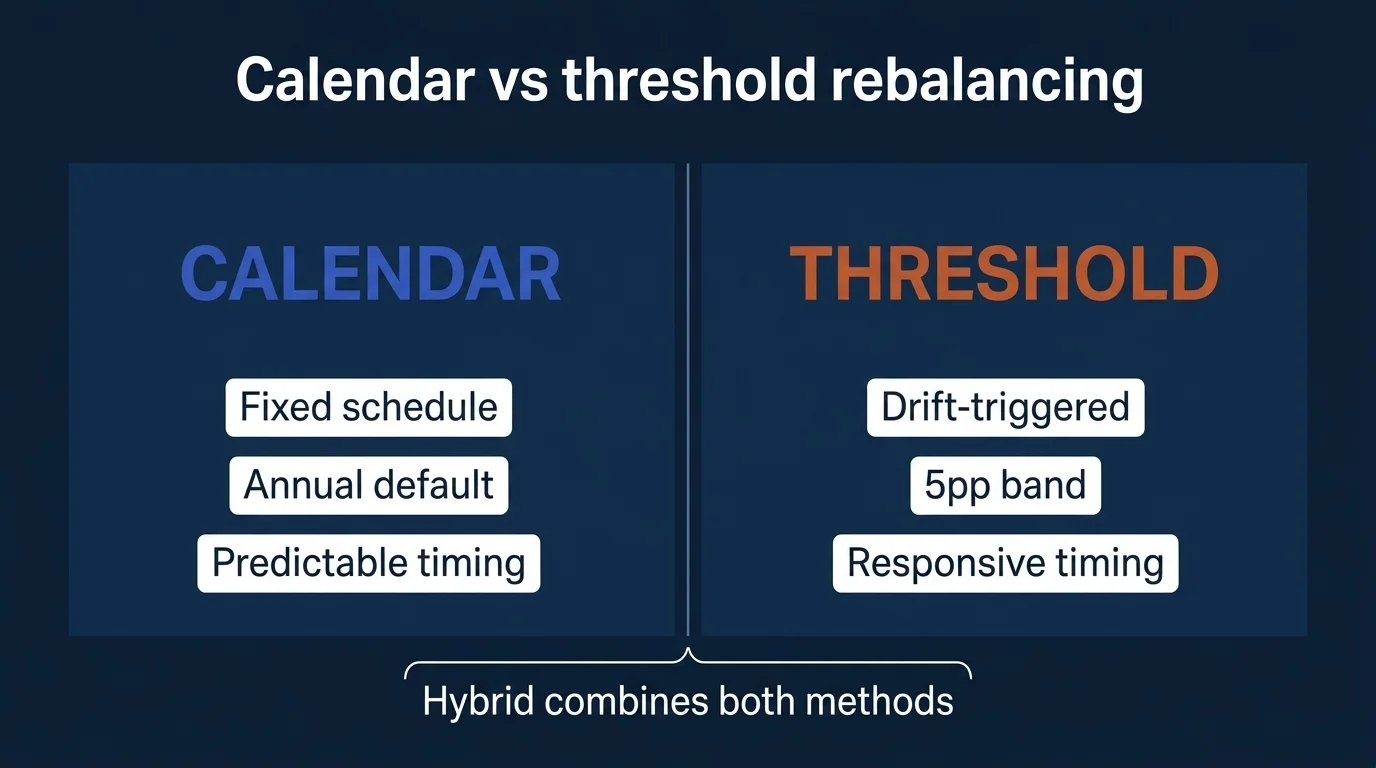

Calendar vs threshold vs hybrid: a comparison

Three named methods dominate the literature, plus a fourth that uses cash flow rather than rebalancing trades.

| Method | How it works | Best for | Tax efficiency | Effort level |

|---|---|---|---|---|

| Calendar | Rebalance on a fixed schedule (e.g., every January) | Simple portfolios, set-and-forget investors | Medium | Low |

| Threshold | Rebalance when any allocation drifts past a 5pp band | Volatile markets, drift-sensitive investors | Medium-high | Medium |

| Hybrid | Annual review + threshold override | Most investors — captures both benefits | High | Low-medium |

| Cash-flow | Direct new contributions to underweight sleeves | Accumulation-phase investors with regular contributions | Highest | Lowest |

The hybrid approach is the institutional default for a reason: it captures the predictability of the calendar method (you know roughly when to look) and the responsiveness of threshold (you act when drift actually warrants action, not just when the calendar arrives). For an investor still in the accumulation phase, the cash-flow approach is the most efficient — directing payroll contributions, dividend distributions, and tax-refund reinvestments toward whichever sleeve is underweight rebalances without realizing gains and without disrupting holdings.

A note on transaction costs: in the era of zero-commission ETF trading at major brokerages, transaction costs are essentially zero for retail-sized rebalancing trades. The remaining costs are tax (in taxable accounts only), bid-ask spreads on less-liquid funds, and time. The bid-ask cost is small for major broad-market ETFs (typically 1-2 basis points) and larger for sector or factor ETFs (5-15 bps). It rarely changes the rebalancing math, but it is worth knowing exists.

Rebalance in your 401(k) first

This is the single most underserved topic in the rebalancing literature, and it is also the one with the highest practical leverage. The mechanics of 401(k) rebalancing differ from taxable rebalancing in three structural ways that change the optimal strategy.

First, 401(k) trades are tax-free. Inside a 401(k) (and inside an IRA), rebalancing trades — selling overweight, buying underweight — generate zero current tax cost. The capital gains are deferred until withdrawal in retirement. This is the asymmetric advantage that drives the 2026 advisor consensus that taxable households should rebalance in tax-advantaged accounts FIRST and use new contributions to nudge taxable accounts toward target rather than realize gains.

Second, modern 401(k) plans typically offer plan-level auto-rebalance. Most large recordkeepers (Fidelity, Empower, Vanguard, Guideline, Human Interest, others) include an auto-rebalance toggle that resets allocations to your selected targets on a fixed cadence (commonly quarterly or annually). Guideline-managed 401(k) plans monitor allocations daily and trigger auto-rebalance at 5% drift. The toggle is usually buried two or three menus deep in the participant portal. Find it. Set targets. Enable auto-rebalance. The plan does the work for free.

Third, fund menu constraints are real. A taxable brokerage account gives you the entire universe of ETFs and mutual funds. A 401(k) gives you the funds your plan's investment committee selected. The implication: your target allocation must be expressible in the funds available, even if the funds available are less optimal than what you would pick for a brokerage account. Pick the closest available proxies. The cost of "imperfect funds in a tax-advantaged account" is almost always less than the tax cost of trying to optimize the asset mix in a taxable wrapper instead.

The order-of-operations rule for households with both 401(k) and taxable accounts:

- Set 401(k) auto-rebalance with target percentages chosen to absorb most of the drift work.

- Direct new payroll and bonus contributions to whichever sleeve is currently underweight.

- Use IRA rebalancing trades for any drift the cash-flow method cannot close.

- Realize taxable-account gains last, and only when steps 1-3 are insufficient.

Following this sequence, most households can rebalance an entire portfolio annually with zero realized tax cost.

Rebalancing + tax-loss harvesting: the integrated practice

Tax-loss harvesting is the deliberate sale of an investment at a loss to realize the loss for tax purposes — the loss can then offset realized gains elsewhere (reducing capital gains tax) and, up to $3,000 per year on individual returns, offset ordinary income, with any unused losses carried forward indefinitely.

The 2025-2026 advisor framing is that TLH and rebalancing are the same operation, not two separate ones. When a portfolio has drifted because some holdings ran ahead while others fell, the rebalance trade — selling overweight winners, buying underweight underperformers — naturally produces realized gains AND realized losses simultaneously. Pair them. The harvested loss offsets the realized gain, the net tax cost approaches zero, and the portfolio returns to target allocation.

Vanguard's research puts the after-tax alpha from this disciplined approach at 0.45% to 0.95% per year, with a broader Advisor's Alpha range up to 1.27%. On a $500,000 portfolio that is $2,250 to $4,750 of additional after-tax return per year, compounded indefinitely. That is meaningful.

The mechanic that requires care is the IRS wash-sale rule: if you sell a security at a loss and buy the same or "substantially identical" security within 30 days before or after the sale, the loss is disallowed for tax purposes. The loss is added to the basis of the replacement security, which means it is not lost forever — it is just deferred. But for current-year TLH, the loss is gone.

The standard workaround is to replace the harvested fund with a similar-but-not-identical fund, then optionally swap back after 31 days. Common pairs that are similar in exposure but not "substantially identical" under the IRS standard:

- VTI ↔ ITOT (Vanguard Total Stock Market vs iShares Core S&P Total U.S. Stock Market)

- VOO ↔ IVV (Vanguard S&P 500 vs iShares Core S&P 500)

- BND ↔ AGG (Vanguard Total Bond Market vs iShares Core U.S. Aggregate Bond)

- VEA ↔ IDEV (Vanguard FTSE Developed Markets vs iShares Core MSCI International Developed Markets)

These are illustrative — the specific funds and tax treatment of substitution belong to a tax professional who knows your situation. The wash-sale rule applies across all your accounts (including a spouse's account in some cases), which is the trap most DIY harvesters miss.

A practical note: TLH only applies in taxable accounts. Inside a 401(k) or IRA, losses are not deductible because gains are not currently taxed — the wrapper does the same job for you, asymmetrically.

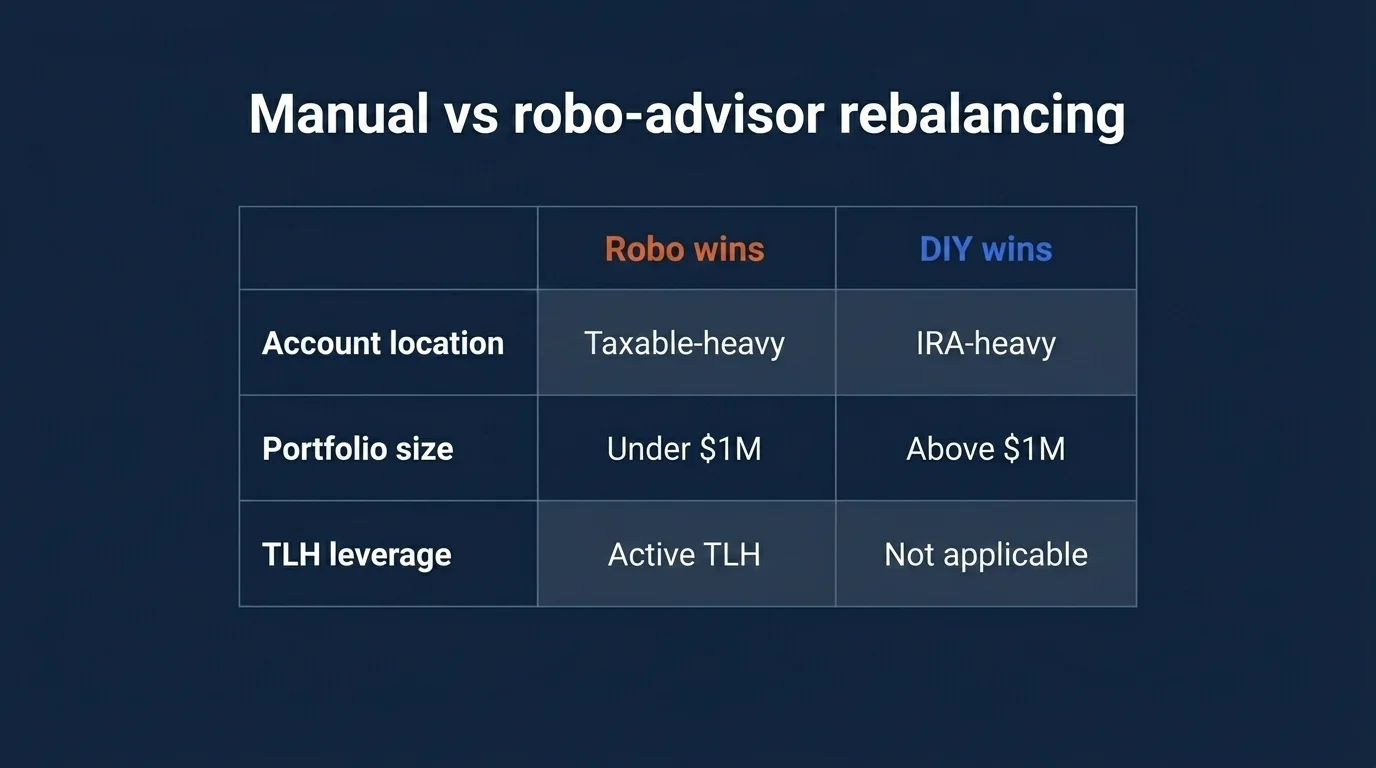

Manual vs robo-advisor rebalancing

Robo-advisors (Wealthfront, Betterment, and others) typically charge 25 basis points (0.25%) per year for managed-portfolio services that include daily-drift-monitored automated rebalancing and tax-loss harvesting. The break-even math against DIY is straightforward, but the inputs vary by household.

On a $100,000 portfolio: 25 bps = $250 per year. That is the explicit cost of the robo service.

Robo wins when:

- The investor would otherwise skip rebalancing entirely (the cost of skipping the 1% TLH alpha alone — $1,000/year on $100K — easily dominates the $250 fee).

- The investor would not run TLH on their own (robos do it daily and at the lot level; DIY usually does it manually and quarterly at best).

- Time is genuinely scarce. A few hours per year saved at a meaningful billable rate covers the cost.

- The portfolio is held in taxable accounts where TLH has actual leverage.

DIY wins when:

- The portfolio is mostly in 401(k)/IRA wrappers where TLH does not apply and plan-level auto-rebalance is free.

- The investor already runs annual rebalancing reliably on a simple 2-3 fund portfolio.

- Cost-sensitivity at scale matters: 25 bps on a $1M portfolio is $2,500/year, and the marginal value of robo TLH may not scale linearly with portfolio size.

The honest middle ground for most households is DIY in tax-advantaged accounts (using auto-rebalance), robo or advisor for taxable accounts where TLH adds material value, with the choice driven by portfolio size and time availability. There is no universal answer; this is a household-by-household calculation.

Q4 / year-end rebalancing checklist

Q4 has consolidated as the default rebalancing window in the 2026 advisor consensus, driven by tax-year-end planning and the fact that most realized losses (for tax purposes) need to be booked before December 31. The minimum checklist a thoughtful investor walks through in November or December:

- Verify the current allocation versus target across all accounts. Calculate drift in percentage points.

- Check 401(k) auto-rebalance settings. Ensure targets are current and the toggle is on.

- Identify any taxable-account positions sitting on losses worth harvesting before year-end.

- Plan the rebalance trade list, sequencing through tax-advantaged accounts first.

- For any taxable rebalancing, identify the wash-sale-safe substitute funds and the 31-day re-entry calendar.

- Direct any year-end bonus, RMD distributions, or dividend reinvestments toward the underweight sleeve as a final cash-flow rebalance.

- Confirm the $3,000 ordinary-income offset is captured if there are excess realized losses.

- Document the trades and tax cost for the next year's review.

This is not exotic work. It is annual maintenance, and the after-tax alpha from doing it well compounds.

What would change my view on the 2026 framework

In keeping with how I approach any analytical thesis: here is the single variable that, if it changed, would invalidate the framework above.

The framework rests on the assumption that rebalancing — at annual cadence with a 5pp threshold override, sequenced through tax-advantaged accounts first, paired with TLH where applicable — produces a meaningful after-tax alpha versus a do-nothing baseline. If the IRS materially changed the wash-sale rule's mechanics, eliminated the indefinite carry-forward of capital losses, or removed the long-term/short-term capital-gains distinction, the math underlying TLH-as-rebalancing-multiplier would have to be redone from scratch. None of those changes is on the legislative docket as of April 2026. None has been seriously proposed. But tax-policy regimes change, and a discipline that depends on a specific tax treatment is a discipline whose math has to be re-run when the treatment changes.

The second variable is structural correlation. If equity-bond correlation flipped to persistently positive (the way it did briefly in 2022), the diversification benefit that rebalancing locks in would weaken. The trade discipline still works — you are still systematically buying low and selling high inside the chosen allocation — but the volatility-suppression rationale weakens, and the right target allocation itself may need to widen toward a third sleeve (alternatives, real assets, or cash) to restore the original risk-adjusted profile.

I am watching both. Neither has happened yet. Both are plausible enough to know the framework's load-bearing assumptions.

That is the rebalancing playbook for 2026 as I would teach it to a new analyst on day one. None of it is individual financial advice. All of it is starting material for the conversation a household should have with the licensed advisor who can translate it into a plan for their specific situation.

Frequently Asked Questions

Annual rebalancing is optimal for most investors per Vanguard's 2026 guidance, with a threshold override: rebalance early if any allocation drifts more than 5 percentage points from target. This hybrid approach captures both the predictability of calendar rebalancing and the responsiveness of threshold rebalancing. Daily-monitored automated rebalancing (used by Wealthfront, Guideline, and most modern 401(k) plans) is functionally similar — it just removes the manual checking step.

The 5% rule is the dominant threshold trigger across institutional providers: rebalance whenever an asset class drifts more than 5 percentage points from its target. A 70/30 portfolio drifting to 76/24 (a 6pp deviation in equities) triggers a rebalance. The refined version is the 5/25 rule — rebalance at 5pp absolute drift OR 25% relative drift, whichever triggers first.

Most 401(k) plans offer plan-level auto-rebalance that resets allocations to your targets on a fixed cadence (often quarterly or annually). Set targets in the participant portal, enable the toggle, and the plan does the work for free. Because 401(k) trades are tax-free, rebalance there before touching taxable accounts. Modern plans like Guideline monitor allocations daily and trigger at 5% drift.

Yes — that is exactly when rebalancing matters most. A drawdown drifts the portfolio toward overweight bonds (which held up) and underweight equities (which fell). Rebalancing forces a 'buy low' discipline that is psychologically hard but historically rewarded. Use cash flow first — direct new contributions to the underweight sleeve. If drift is too large for cash flow alone, sell bonds in a tax-advantaged account and buy equities.

Pair the sale of overweight winners with realized losses from underperforming positions in the same window. Vanguard research finds disciplined TLH adds 0.45%-0.95% in annual after-tax return, with a broader Advisor's Alpha range up to 1.27%. Watch the IRS 30-day wash-sale rule — if you sell a security at a loss and buy the same or 'substantially identical' security within 30 days, the loss is disallowed. Use similar-but-not-identical replacements (VTI → ITOT, VOO → IVV, BND → AGG).

At 25 basis points, Wealthfront and Betterment cost roughly $250 per year on a $100,000 portfolio. Worth it if you would otherwise skip rebalancing or want automated daily-drift TLH on a meaningful taxable balance. DIY makes sense for disciplined investors with simple 2-3 fund portfolios held mostly in tax-advantaged accounts where TLH does not apply.

Calendar rebalancing operates on a fixed schedule (e.g., every January) regardless of drift. Threshold rebalancing operates only when an allocation drifts past a band (typically 5 percentage points). Hybrid combines both — review annually as a default, but rebalance early if the threshold is breached. The hybrid approach is the institutional consensus.