The Great Depression and Personal Finance: Lessons from a Crisis

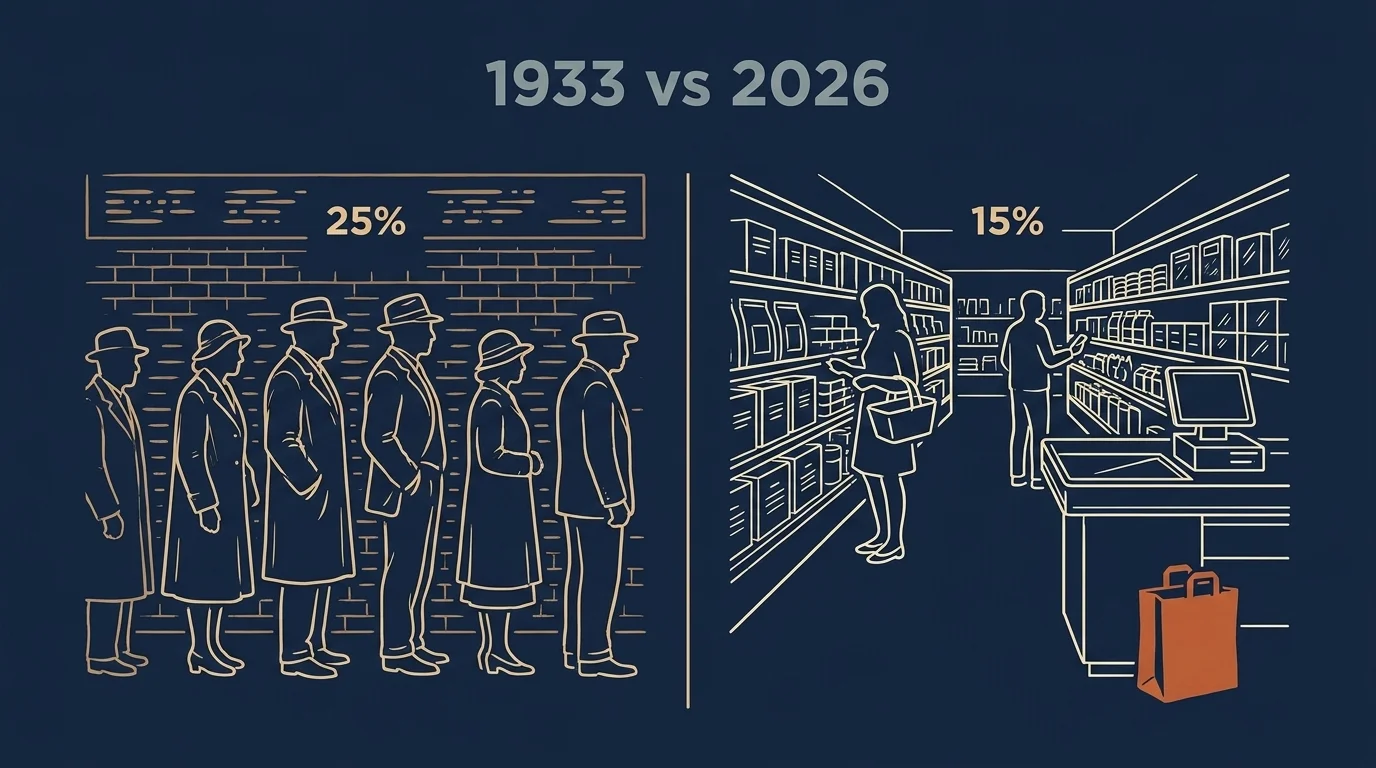

The great depression lessons that still matter in 2026 sit on top of one hard frame: it is now ninety-seven years since the 1929 crash, and the next generation of investors is the first since 1933 to be running active financial plans under serious macro stress. Unemployment hit 25% at the trough in 1933, roughly 9,000 banks failed between 1930 and 1933, and the average unemployment spell in that period ran well over a year. The Pandemic-era peak was 15% in 2020. Forecasters including the Calcalist economist analysis published in late 2025 now describe a "Depression-scale recession by the end of the decade" as a plausible scenario driven by compounding macro pressures rather than any single trigger. Whether the forecast is right is not the point of this article. The point is that the Great Depression lessons that survived the intervening century are the same ones that work in 2026 — and most of the financial media writing about them is missing the substance.

I am going to walk through twelve specific lessons, with the numbers I would name across the desk to a real household. None of this is individual financial advice. Each lesson is a starting point for a conversation with a fiduciary planner who can see your specific situation — your tax bracket, your time horizon, your household balance sheet — that no general article can address.

Lesson 1: cash is the only liquidity that compounds in a crisis

The Great Depression's hardest household lesson was that in a deflationary collapse, cash gets more valuable, not less. The investors who held leveraged equity positions in 1929 lost most of their capital by 1933. The investors who held cash — even at zero nominal return — could buy assets in 1933 at a fraction of their 1929 prices. The math of the crash advantaged liquidity in a way that almost no other historical period has matched.

For a 2026 household, the operational version of this lesson is not "hold all your money in cash". It is "the cash portion of your portfolio is itself a position, and it pays off in the scenarios that matter most." The cash sleeve is what lets you not sell equities at the bottom of a recession. It is what lets you take a job offer at lower pay when the alternative is unemployment. It is what lets you act when everyone else cannot.

Lesson 2: panic selling permanently destroys capital

The single most expensive behavior of 1929-1932 was selling at the bottom. The Dow fell roughly 89% from its September 1929 peak to its July 1932 trough. Investors who sold during the worst of that decline locked in losses that, even with the eventual recovery, took decades to recover. Investors who held — or who continued to buy through the trough — captured the entire recovery.

This is not a market-timing argument. I do not believe in market timing. It is an argument that the modern equivalent — dollar-cost averaging through the bad years, holding equity allocations through drawdowns, refusing to interrupt retirement contributions during recessions — is the discipline that compounds. Most financial outcomes are determined by what you do during the worst three quarters of any given decade. The Depression taught this once, the 2008 crisis taught it again, the 2020 COVID crash taught it a third time. Most retail investors learn it once per cycle and forget by the next.

Lesson 3: institutions matter — FDIC, SEC, and Glass-Steagall

The reason a literal repeat of the Depression is structurally less likely in 2026 than it was in 1929 is not that human nature has changed. It is that the institutional infrastructure has. The Federal Deposit Insurance Corporation (FDIC) was created in 1933 in direct response to the 9,000 bank failures. The Securities and Exchange Commission (SEC) was created in 1934 to regulate the public-equity markets that produced the 1929 speculation. The Glass-Steagall Act of 1933 separated commercial and investment banking — a separation that was later largely repealed but whose deposit-insurance core survives.

The operational point for any household is that the institutions are not optional knowledge. FDIC coverage runs to $250,000 per depositor per insured bank. SIPC coverage on brokerage accounts runs to $500,000 (with a $250,000 cash sub-limit). Below those thresholds, your money is insured against institutional failure. Above them, you need a deposit-diversification strategy (see Lesson 6). The 1929 saver had none of that protection. The 2026 saver who stays inside the limits has all of it.

Lesson 4: multiple income streams are a balance-sheet defense

The Depression households that held together were rarely the ones with the highest pre-1929 income. They were the ones with diversified income — a small farm plot, a side trade, a rental room, a working spouse, an extended family of contributing members. Income diversification did the same work for the household balance sheet that asset diversification does for the portfolio: when one source failed, others continued.

The 2026 version of this is the second income source — freelance work, a side business, rental property, dividend or interest income, intellectual-property royalties. Two income streams do not double household income; they significantly reduce the probability that household income drops to zero. For any household where both adults work full-time in the same industry, the income concentration is the same risk profile as a single-stock portfolio. The fix is not necessarily a career change. It is a deliberate plan for what the household does if either of the primary streams ends.

Lesson 5: liquidity before leverage

The credit lesson of the Depression is uncomfortable because credit is sold to American households as a virtue. The Depression demonstrated that credit is a tool with one mode in good times (acceleration) and a different mode in bad times (destruction). Households that had financed their 1929 stock purchases on margin lost everything by 1932. Households that had financed their 1929 home purchases on mortgages they could only service with continued employment lost their homes when unemployment hit.

The principle that survives translation is: liquidity before leverage. Build the cash position first. Build the emergency fund first. Hold a margin of safety on any debt service against your actual income, not your expected income. The 1929 household that violated this principle could not recover; the 1929 household that kept it intact could buy the same assets in 1933 at one-tenth the price.

Lesson 6: diversification across assets AND across banks

The asset-diversification argument has been made for so long it is almost background noise. The bank-diversification argument is the same argument applied to deposit risk, and it is the lesson the 1933 FDIC was specifically designed to address.

The operational rule is the FDIC $250,000 limit per depositor per insured bank. A household with substantial cash savings well above the FDIC cap should not hold all of it at one institution; it should be distributed across multiple insured banks (or use insured cash sweep products that distribute deposits programmatically). On the brokerage side, SIPC coverage caps at $500,000 per separate-customer-relationship, with $250,000 for cash. Holding both retirement and taxable accounts at the same broker counts as one customer relationship for SIPC purposes — splitting brokers above the cap is the structural defense.

For 2026 households with significant cash positions, the most under-implemented version of this lesson is sitting at a single high-yield savings account well above $250,000. The fix is administrative, not strategic — but the protection only exists if you actually do it.

Related Article: The Art of Financial Planning for Young Professionals: Building Wealth from the Start

Lesson 7: build an emergency fund of 6-12 months

The standard pre-2008 emergency-fund rule was three to six months of household expenses. The post-Depression, post-2008, post-COVID consensus has moved to six to twelve months — anchored in the empirical reality that the Depression-era average unemployment spell ran well over a year, and the COVID-era spells were sustained by exceptional federal transfer payments that may not recur.

For a typical middle-class household, the twelve-month version translates into roughly a year of essential expenses held in liquid cash. That is a large number. It is also the number that lets the household avoid selling equity holdings during a recession, avoid cashing out retirement accounts under stress, and avoid taking the first available lower-paying job offer just to keep the bills paid. The cost of holding cash is the opportunity cost of the foregone return. The cost of not holding cash is everything that happens in the bad scenarios.

Lesson 8: frugality tactics that still work

The Wise Bread version of this list is the longest in the SERP, and most of it is durable. A few that are worth naming because they survive 2026 grocery prices intact.

- Substitute lentils for ground beef in volume cooking. Dried lentils run under $2 per pound; ground beef runs $4-$6 per pound. Spaghetti, chili, and Bolognese-style dishes accept a 50/50 lentil-to-beef ratio without meaningful taste impact. Multi-pound substitutions matter at scale.

- Mend rather than replace. A $4 hem repair extends a $40 garment by years. The break-even is immediate.

- Garden what you eat. Even a small home garden of high-volume produce (lettuce, tomatoes, herbs) produces nontrivial savings against grocery prices, and the time investment is moderate.

- Buy in bulk on shelf-stable staples. Rice, beans, oats, canned goods, and toilet paper have minimal storage cost and meaningful per-unit savings at warehouse-club volume.

- Layer clothing before raising the thermostat. Each degree of thermostat reduction in winter is a measurable saving on annual heating costs.

These are not poverty tactics. They are habits that produce meaningful household savings whether or not the macro environment is a Depression. The 1933 household used them because it had no choice. The 2026 household using them by deliberate choice has the savings redirect to retirement contributions, debt service, or the emergency fund.

Lesson 9: what we learned in 2008, and what we didn't

The most analytically honest framing of the Depression's modern legacy comes from Christina Romer's Berkeley lecture on lessons for policy today. The Friedman-Schwartz argument that the Federal Reserve's failure to act as lender of last resort in 1930-1933 was the central policy failure of the Depression was applied directly in 2008-2009. Ben Bernanke, then Fed chair, was a Friedman-Schwartz scholar by training and explicitly cited the Depression playbook in the Fed's 2008 liquidity response.

The 2008 response, on the Fed liquidity side, worked. The post-2008 European austerity response — which prioritized fiscal consolidation in a depressed economy — is now consensus-cited as evidence that the same intellectual generation had not learned the Depression's full lesson. The Depression's twin policy failures were monetary (the Fed) and fiscal (the Hoover-era austerity that delayed the New Deal). The 2008 response fixed the first. It did not fully fix the second.

The household implication is that the regulatory and monetary infrastructure of 2026 is structurally better than 1929. The fiscal-political infrastructure remains contested, and that is the dimension where the next macro stress will most likely be tested.

Lesson 10: the generational health and economic legacy

The single least-quoted research finding on this topic comes from the Center for Retirement Research at Boston College: Depression-era childhood stress measurably accelerated biological aging after age 75, with explicit implications for the children of the 2008-2009 Great Recession and the toddlers of the 2020 COVID downturn. The economic costs of recessions are not bounded by the recessions themselves. They show up in cohort health outcomes decades later.

For a household with children, the financial-preparedness work is not only self-protective. It is a multi-generational obligation. The 1929 children who grew up in households that maintained stability — even at reduced consumption — had measurably better life-long health outcomes than the children who did not. The same will likely prove true for cohorts that experienced 2008 and 2020 during formative years, and the same will be true for any 2026 cohort that experiences serious macro stress. The emergency fund and the income diversification are tools that protect the next generation, not just the current one.

Lesson 11: insurance and liquidity

The Depression-era lesson on insurance is that whole-life insurance with accumulated cash value was, for some households, the single most useful liquidity asset they held. The cash-value loan provision allowed households to borrow against the policy at relatively low rates when no other credit was available.

The 2026 version of this lesson is more nuanced. Whole-life and indexed-universal-life insurance products are sometimes oversold as wealth-accumulation vehicles when they are more accurately liquidity vehicles. For most households, term life insurance plus a separate cash position is more efficient than a bundled whole-life product. But for higher-net-worth households with maxed-out tax-advantaged space, a permanent policy can play a legitimate role in the liquidity stack — particularly for business owners whose other capital is illiquid in operating assets.

This is one of the conversations that is genuinely better held with a fee-only planner who has no commission interest in selling you a specific policy. The product complexity is high, the regulatory framework varies by state, and the sales channel is structurally biased.

Lesson 12: sequence-of-returns risk if you retire into a downturn

This is the lesson I will give the most attention to, because it is the one financial media is most reliably wrong about, and because it is closest to my own practice.

If you retire at the start of a sustained bear market, the math of withdrawals compounds against you in a way that a good market later cannot fully repair. A portfolio that takes a deep drawdown in year one of retirement, with a fixed-dollar withdrawal, is drawing from a base that has fallen substantially — and the same dollar withdrawal is now a much larger percentage of the new base. The portfolio that survives this is the one that has held a specific number of years of living expenses in short-duration fixed income at the point of retirement, so that the retiree is not forced to sell equities at a loss to eat.

A 1929 retiree experienced this in its most extreme form. The 2026 retiree who has internalized the lesson holds a significant cash and short-bond reserve — typically two to five years of essential expenses — at the front edge of retirement, with the equity allocation continuing to compound through the drawdown. The specific size depends on the household: spending flexibility, Social Security and pension income, longevity assumption, and risk tolerance. The number is not an article-level answer. It is a planner-level answer.

What I would tell a household sitting across the desk

If you take three things from this list, take these.

First, the Depression's lesson is not that catastrophe is coming. It is that the households which survived the catastrophe were the ones that had liquidity, low leverage, diversified income, and a willingness to hold equities through the worst years. None of those positions is exotic. All of them are work.

Second, the institutional infrastructure built after 1933 — FDIC, SEC, the Federal Reserve's lender-of-last-resort doctrine — significantly reduces the probability of a literal repeat. That does not eliminate the possibility of a serious recession. It does mean that the household preparation work is what determines how that recession lands on your specific balance sheet.

Third, the work is multi-generational. The Center for Retirement Research finding on Depression-era childhood stress should be enough to anchor the preparedness conversation as something that protects your children's health outcomes, not just your own retirement timeline. That framing changes how the work gets done.

None of this is individual financial advice. The right size of your emergency fund, the right asset allocation, the right insurance configuration, and the right retirement timeline all depend on facts I cannot see — your tax bracket, your time horizon, your specific account types, your household balance sheet. Treat the twelve lessons above as the structure of a serious conversation with a fiduciary planner. The lessons are the frame. The planning is the work, done with care, household by household, for as long as the cycles keep coming. They will.

Frequently Asked Questions

Six to twelve months of essential household expenses is the contemporary consensus. The Depression-era reality was that the average unemployment spell ran well over a year, and the COVID-era spells were sustained by exceptional federal transfer payments that may not recur. For a household with $7,000 a month in essential expenses, the twelve-month version is $84,000 in liquid cash. The cost of holding that cash is the opportunity cost of forgone return; the cost of not holding it is everything that happens in the bad scenarios.

Most economists view a literal repeat as structurally unlikely because of the FDIC, the SEC, and the Federal Reserve's lender-of-last-resort doctrine — all created in direct response to the 1929-1933 failures. The Calcalist economist analysis published in late 2025 warns that a Depression-scale recession by end-of-decade is plausible from compounding macro pressures, not a single trigger. The institutional infrastructure is the structural reason this is no longer the 1929 problem; the political-fiscal infrastructure is where the next stress is most likely to be tested.

Liquidity before leverage. Households that held cash and limited debt in 1929 survived the Depression intact and were positioned to buy assets at 1933 prices. Households that leveraged into stocks or mortgages they could only service with continued employment lost everything in months. The modern translation is to build the cash position first, hold an emergency fund of 6-12 months, and stress-test any debt service against your actual income rather than your expected income.

The Great Depression produced 25% peak unemployment in 1933, roughly 9,000 bank failures between 1930 and 1933, and a Dow Jones decline of approximately 89% from its 1929 peak to its 1932 trough. Individual households lost wealth in stock holdings, savings in failed banks, homes through mortgage default, and incomes through unemployment that for many households lasted multiple years. The compounding loss across all four dimensions is what makes the Depression a structurally different event from any subsequent US recession.

Investor fear drove the most expensive behavior of the entire period — selling at the bottom. Investors who sold during the worst of the 1929-1932 decline locked in losses that took decades to recover, while investors who continued to hold or buy through the trough captured the full recovery. The lesson is not that markets always recover quickly; the lesson is that the act of selling at the bottom permanently destroys capital, and that disciplined approaches like dollar-cost averaging and maintaining equity allocations through drawdowns produce better outcomes than emotion-driven selling.

The New Deal created the institutional infrastructure that distinguishes modern American household finance from the 1929 environment. The Federal Deposit Insurance Corporation (FDIC) insures bank deposits up to $250,000 per depositor per insured bank, ending the bank-run dynamic that destroyed savings in 1930-1933. The Securities and Exchange Commission (SEC) regulates public-equity markets. The Glass-Steagall Act separated commercial and investment banking. The Social Security Act of 1935 added retirement and disability protection. Together, these institutions reduced the probability that a future recession compounds into a Depression-scale household catastrophe.

Credit operates in two distinct modes: acceleration in good times and destruction in bad times. The Depression demonstrated that households who financed 1929 stock purchases on margin or financed home purchases on mortgages they could only service with continued employment lost everything when unemployment hit. The principle that survives is liquidity before leverage — build the cash position and the emergency fund first, hold a margin of safety on any debt service against actual rather than expected income, and recognize that the same credit that accelerates wealth-building in expansion can destroy a household balance sheet in contraction.

Three durable strategies came out of the post-Depression era. First, asset diversification — across asset classes (equities, bonds, cash, real estate) and within asset classes (broad index exposure rather than concentrated single-stock positions). Second, sequence-of-returns risk management — holding two to five years of essential expenses in short-duration fixed income at the front edge of retirement so the household is not forced to sell equities at a loss. Third, the discipline of continued investment through downturns rather than panic-selling at the bottom. All three remain the foundation of modern portfolio theory and fiduciary financial planning.

Check Out These Related Articles

Redefining Financial Literacy through Interactive Social Media Initiatives

Financial Wisdom through the Ages: Learning from Ancient Philosophers and Modern Financial Gurus

Ethical Considerations in Personal Finance and Healthcare Nexus