Ethical Considerations in Personal Finance and Healthcare Nexus

A genuinely useful disconnect to open with: Morgan Stanley's global survey, surfaced in A&O Shearman's 2026 Sustainability Outlook, found that 88% of individual investors globally remain interested in sustainable and ethical investing. The same year, the US ESG-fund category posted approximately $27 billion in Q4 2025 outflows, and 192 anti-ESG bills were proposed across US state legislatures during 2025 alone (Britannica Money). The interest in the underlying ideas is not collapsing. The labeled-product flows are.

That gap matters more in healthcare than in most other sectors. Healthcare-related companies sit on the most-contested ethical territory in modern public markets — insulin pricing, opioid litigation, EpiPen-style monopoly pricing, private-equity ownership of hospitals, supply-chain labor practices in medical devices, animal testing protocols — and the standard ESG-labeled fund is rarely doing the sector-specific work a thoughtful retail investor would actually want done. The 2025 greenhushing trend has made it harder, not easier, to know whether a fund's screen actually matches what its marketing implies.

This piece is the healthcare-sector companion to the broader ethical investing primer for 2026, which covers the canonical four approaches (negative screening, positive/best-in-class, ESG integration, thematic/impact) and the cross-sector ETF universe. Here, the question narrows: how does a retail investor actually screen the healthcare exposure inside their portfolio against the specific ethical questions the sector raises — and which funds and tools make that screen possible without an institutional research budget?

The healthcare-sector ethical investing question, specifically

Most coverage of ethical investing treats it as a portfolio-level decision: which broad-market ESG fund to hold instead of a broad-market index fund. The healthcare-sector version of the question is genuinely different, for two reasons.

First, the headline ethical controversies in healthcare cluster differently than in other sectors. A retail investor concerned about, say, fossil-fuel exposure can express that preference cleanly through a broad-market ESG screen that excludes energy producers. A retail investor concerned about insulin pricing practices or opioid-litigation exposure or private-equity hospital roll-up strategies is asking a much more granular question — one that broad-market ESG screens rarely answer at the level of resolution that matters.

Second, healthcare-sector funds are mostly NOT ESG-screened. The sector exists as a discrete allocation in most retail portfolios (XHE, IHF, IXJ, IBB), and the standard sector ETFs hold the same controversial names that a thoughtful ethical-screen investor might want to exclude. The healthcare allocation in a retail portfolio is, by default, the un-screened version. The screening work has to be added — it does not come for free with the sector exposure.

What that means in practice is that the healthcare-sector ethical-investing question is less "which fund do I hold instead" and more "do I want explicit healthcare exposure, and if so, what screen am I applying on top of the sector?"

Pharma-specific ethical dilemmas a sector fund makes you own

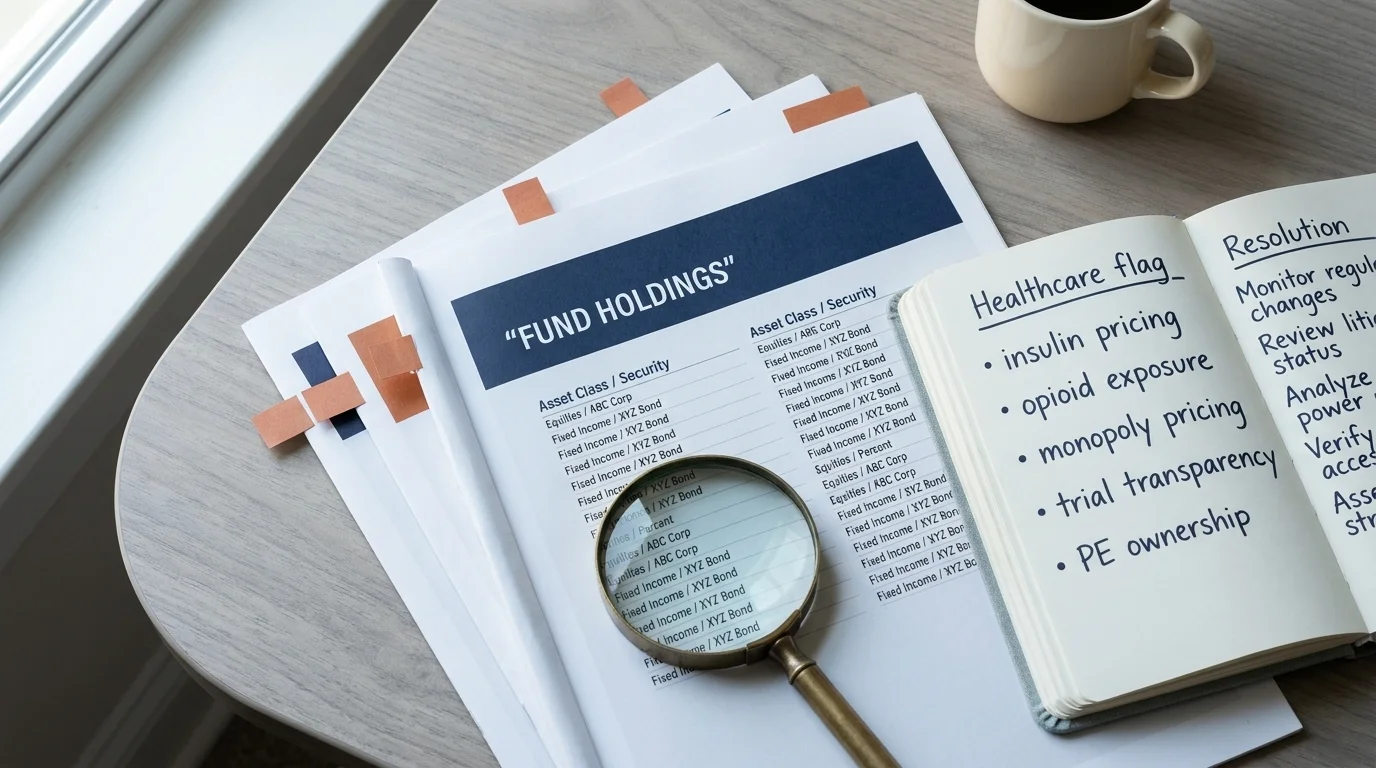

A representative healthcare-sector ETF (XHE for equipment, IHF for providers, IXJ for global healthcare, IBB for biotech) holds positions across pharma, devices, providers, payers, and biotech. The ethical-screen questions that most often surface in planning conversations with healthcare-sector investors:

- Insulin pricing. Companies in the insulin supply chain have been at the center of pricing-litigation cycles for over a decade. The retail investor holding a large-cap pharma ETF holds those names, regardless of personal view on insulin pricing.

- Opioid litigation exposure. Several large pharma and pharmacy-distributor names have been parties to multi-billion-dollar opioid settlements. The exposure flows through to broad-market funds and sector ETFs alike. The ethical question is not whether to acknowledge the litigation — it is whether to continue funding the companies through equity ownership after the settlements close.

- EpiPen-style monopoly pricing. The Mylan / Pfizer EpiPen pricing controversy is the most-cited canonical example, but the pattern (single-supplier essential medication, price elasticity dominated by life-or-death demand, settlement-and-continue) recurs across multiple categories.

- Drug-trial transparency. Clinical-trial registration, outcome reporting, and access-after-trial questions all sit inside the ESG-G (governance) column for most ratings agencies. Some pharma names have substantially worse track records on these than others.

- Animal testing protocols and supply-chain labor. For investors with religious or values-based screens, the supply chain of large-cap pharma and medical devices is a screen point that the standard sector ETF does not address.

Naming the specific controversies matters because the sector-fund retail allocation is, by default, a vote of confidence in every company in the index — not just the ones the investor would have actively chosen. A thoughtful screen does not require the household to become a sector analyst. It does require the household to know which of the above questions matter most to them, so the screen can be calibrated to address those questions specifically.

Private equity in healthcare: the ethics question retail investors miss

The fastest-growing ethical question in healthcare investing in 2025-2026 is the role of private equity in healthcare ownership — emergency-medicine staffing, hospice, nursing-home chains, dialysis providers, dermatology and gastroenterology practice roll-ups. The 2024-2025 academic literature has converged on a finding that matters for the retail investor: PE ownership in healthcare correlates with worse patient outcomes, higher costs, and reduced access. Both the Georgetown Law Denny Center and the AMA Journal of Ethics issue on Private Equity in Health Care document the pattern in peer-reviewed terms.

The retail-investor relevance is two-fold. First: most retail investors do not directly hold private-equity funds, so they assume PE healthcare exposure is not their problem. It is. The publicly-traded PE firms (the largest names in the alternative-asset-manager category) are themselves held by broad-market funds and large-cap index funds — and the publicly-traded healthcare facility operators that are PE-acquired or PE-influenced flow into the same funds. Direct PE ownership is the institutional layer; PE-adjacent equity exposure flows through every standard portfolio.

Second: the screen that surfaces PE-healthcare exposure inside a retail portfolio is not standard. Few retail-facing ESG screens explicitly flag PE ownership of healthcare facilities as a screen criterion. The investor who cares about the question has to either (a) hold a thematic impact fund that explicitly screens against the practice, (b) accept the exposure and use shareholder engagement, or (c) reduce the broad-market exposure deliberately. None of those is straightforward and all involve a real trade-off.

Healthcare-relevant ESG and sector funds in 2026

The roster below is the working catalog of funds a retail investor exploring the healthcare-ethical-investing question would benefit from knowing. None of these is a recommendation. Verify the current expense ratio, top holdings, and methodology on the fund issuer's site before investing — fund data drifts and the 2025-2026 retreat is repositioning many funds actively.

The most important distinction in the table is the column on the right: which funds are sector funds (healthcare-specific exposure, no ethical screen) and which are ethical / impact funds with healthcare-specific theses. Most retail healthcare exposure comes from the first column. The second column is small.

| Fund | Category | Approach | Notes for the ethical-screen investor |

|---|---|---|---|

| SPDR S&P Health Care Equipment ETF — XHE | Sector ETF (equipment) | No explicit ethical screen | Pure-play medical-equipment exposure; the ethical screen has to be added separately |

| iShares US Healthcare Providers ETF — IHF | Sector ETF (providers) | No explicit ethical screen | Includes payors and provider chains; PE-adjacent exposure flows through |

| iShares Global Healthcare ETF — IXJ | Sector ETF (global) | No explicit ethical screen | Global pharma and device exposure; includes the named insulin/opioid exposure |

| iShares Biotechnology ETF — IBB | Sector ETF (biotech) | No explicit ethical screen | Wider drug-trial-transparency questions sit here at scale |

| Vanguard ESG US Stock ETF — ESGV (reference) | Broad-market ESG | ESG integration | Holds healthcare names within the broader ESG screen; not healthcare-specific. Mentioned for context. |

| Impact / thematic healthcare funds (small category) | Thematic impact | Explicit impact thesis (health equity, drug access, infectious disease) | The genuinely-impact-screened slice of the healthcare opportunity; smaller AUM, more demanding methodology |

Verify before you act. Fund expense ratios, top holdings, and methodology change. The data in this article is current at the time of writing and will drift. Read the prospectus and the current fact sheet on the fund issuer's website, and remember that this article is education — not personalized investment advice. For your specific household, talk to a licensed advisor who can see your tax bracket and full balance sheet.

The cleanest read on the table is the structural one: the broad sector funds (XHE, IHF, IXJ, IBB) are the default retail healthcare exposure, and they do not screen on any of the ethical criteria discussed above. The retail investor who wants the screen has to do the screen — either by adding a layer of methodology evaluation on top of the sector fund, by selecting a broader ESG-integrated fund with healthcare exposure inside it, or by selecting a thematic impact fund whose explicit thesis matches the investor's preferred screen criteria.

How to actually screen a healthcare holding ethically (a 6-step checklist)

The screening framework below is healthcare-specific. For the broader four-approaches framework (negative screening, positive/best-in-class, ESG integration, thematic/impact), see the parent ethical investing primer — the four approaches apply to healthcare funds the same way they apply to broad-market funds, but the sector-specific work happens at the level of the holdings.

- Read the methodology document inside the prospectus, not the marketing page. Pull the SEC-filed methodology or statement of additional information. What exactly does the fund exclude (entire industries, specific companies, ratings thresholds)? Who supplies the ESG ratings (MSCI, Sustainalytics, Morningstar, proprietary)?

- Pull the top 25 holdings. Compare them against the major US healthcare-sector ETFs (XHE, IHF, IXJ, IBB). If a fund's "ESG" healthcare holdings are nearly identical to the unscreened sector ETF, the screen is doing very little of the work the fund name promises.

- Check exposure to the five healthcare-specific ethical flashpoints. Insulin pricing (which manufacturers? Eli Lilly, Novo Nordisk, Sanofi are the canonical three). Opioid litigation exposure (which manufacturers and distributors are named in active or recently-settled litigation?). Single-supplier essential-medication pricing (EpiPen-style cases). Drug-trial transparency record. PE-adjacent hospital or provider chain exposure.

- Check the fund's voting record on shareholder resolutions. Funds that vote on shareholder proposals related to drug pricing transparency, prescription affordability, and healthcare-access disclosure are doing engagement work alongside the screen. Funds that do not vote, or vote consistently with management, are running passive exposure with marketing.

- Check the third-party ESG rating of the fund itself. Morningstar Sustainability Rating, MSCI ESG Fund Rating, and Sustainalytics Fund Rating each score the underlying portfolio. The fund's own marketing may or may not align with what the third-party raters see.

- Check what changed in the past 24 months. Funds rebrand. A fund that quietly dropped "ESG" from its name in 2024-2025 may still be running the same screen — or may have substantially loosened it. The prospectus amendments tell the story.

The pattern across all six steps: methodology beats label, holdings beat marketing, third-party rating beats issuer self-rating. None of these is novel discipline. They are just more important in healthcare than in most sectors because the underlying ethical questions are more granular than a broad-market screen is designed to handle.

Greenhushing and healthcare: what your fund's prospectus may not say

The Conference Board reported in June 2025 that 80% of large US and multinational companies were revising their ESG strategies — and many were quietly dropping the "ESG" terminology from filings, marketing, and earnings materials while continuing to operate the underlying screens. The pattern is called greenhushing, and it has changed the practical work of vetting a healthcare ESG fund in 2026 in two specific ways.

First: the fund-name signal that worked in 2018-2023 ("look for 'ESG' or 'sustainable' in the fund name") works much less well now. A fund whose 2023 marketing was built on ESG branding may have removed the language while keeping the screen — or may have removed the language and loosened the screen, with the lower visibility making the change less noticeable to retail investors. The work has moved from the name to the methodology document and the holdings list.

Second: third-party ratings (Morningstar Sustainability, MSCI Fund ESG) have become more important precisely because the issuer's own marketing has become less informative. A fund's MSCI ESG Fund Rating is a published, externally-calculated number based on holdings-level analysis. It is harder to greenhush a third-party rating than a marketing page.

For the healthcare-sector investor specifically, the greenhushing implication is that the most rigorous ESG-healthcare funds available in 2026 are not necessarily the ones with the most prominent ESG marketing. Some of the most thoughtful sector-and-screen alignments are now being run inside funds whose marketing leans heavily on "quality" or "long-term" framing rather than "ESG" or "sustainable" framing. The discipline is the same: methodology, holdings, third-party rating.

ARHI and Ethisphere: institutional shortlists worth knowing

Two concrete current institutional resources worth knowing about as starting points (not endpoints) for a retail screen:

The Association for Responsible Healthcare Investment (ARHI) launched in February 2025 as a coalition of private-capital healthcare investors committing to patient-centered standards. The public member list is a useful starting reference for the retail investor evaluating which institutional capital pools at least publicly claim ethical guardrails on their healthcare positions — recognizing that membership in an industry coalition is a claim, not a substitute for due diligence.

Ethisphere's World's Most Ethical Companies list has named approximately 138 honorees across 17 countries in its 2026 cohort. Among the publicly-traded healthcare names on the list: HCA Healthcare was named to the 2026 cohort — one of the few large publicly-traded hospital operators on the list. The list is a starting filter for individual-company exposure within a sector fund; it is not a buy signal, and it does not address sector-fund-level decisions.

Both resources are starting points. Both are also subject to the same critique that applies to any third-party recognition program: the underlying screen criteria are public, the application work is real, and the result is informative without being dispositive.

The performance question, honestly

The 2024 Morningstar data, summarized by Britannica, found that the US Sustainability Index outperformed conventional counterparts over 1-, 3-, and 10-year periods. In early 2025, the sustainability index trailed (-6.20% vs -8.96% for the broader market) — but the framing matters: the sustainability index fell less during a market drawdown that hit fossil-fuel-light portfolios less than fossil-fuel-heavy ones. The early-2025 data, read honestly, undercuts rather than supports the "ESG underperforms" narrative.

For the healthcare-sector investor specifically, the cross-sector performance data above is suggestive rather than dispositive. A healthcare-screened thematic fund will have its own performance dispersion, driven by sector-specific dynamics (drug-pipeline outcomes, regulatory decisions, payer reimbursement changes) that the cross-sector ESG performance comparison does not capture. The honest framing is: there is no general performance penalty for ethical screening that the data supports, and healthcare-specific funds will have their own performance volatility driven by sector dynamics that the screen does not change.

The honest planning conversation is not "do I accept lower returns for ethics." The historical data does not support that framing. The honest planning conversation is "which combination of broad-market exposure, sector exposure, and screen criteria fits my household's actual goals, time horizon, and ethical priorities."

Related Article: The Art of Financial Planning for Young Professionals: Building Wealth from the Start

What to actually do this quarter

For a reader who has gotten this far:

- Identify your existing healthcare exposure. Pull the top 10 holdings of every fund in your portfolio. Calculate the percentage of total portfolio exposure to the named pharma, device, biotech, hospital, and PE-adjacent healthcare names. Most retail investors are surprised by the number.

- Decide which of the five healthcare-ethical-flashpoints matter most to your household. Insulin pricing, opioid litigation, EpiPen-style monopoly pricing, drug-trial transparency, PE-in-healthcare. Not all of them have to matter. The discipline is to know which ones do, so the screen is calibrated.

- Run the 6-step screening checklist on your largest healthcare position. Methodology, top holdings, exposure to the five flashpoints, voting record, third-party rating, recent changes. Twenty minutes of work that most retail investors never do.

- Bring the analysis to your planner. Fee-only, fiduciary. The conversation is materially more productive when the household has done the screening work first — the planner can then focus on the tax, allocation, and account-structure variables that change the implementation of the screen, rather than building the screen from scratch in the meeting.

The broader question — how to think about ethical investing at the portfolio level, across all four approaches and the cross-sector ETF universe — sits in the parent ethical investing primer. The healthcare-sector work documented above sits on top of that broader framework.

None of this is individual investment advice. The right healthcare-sector exposure for your household depends on your tax situation, time horizon, existing portfolio, and the specific ethical priorities only you can name. For decisions of any size, talk to a licensed fee-only advisor who can see the household specifics this article cannot. The framework is the input to the planning conversation, not a replacement for it.

Frequently Asked Questions

It depends on which specific controversies matter most to the household. Insulin pricing (Eli Lilly, Novo Nordisk, Sanofi), opioid litigation exposure (multiple large pharma and pharmacy-distributor names), EpiPen-style monopoly pricing, and drug-trial transparency are the most common flashpoints. A retail screen evaluates exposure to each on a per-company basis rather than treating 'pharma' as a single ethical category.

The 2024 Morningstar data showed the US Sustainability Index outperformed conventional counterparts over 1-, 3-, and 10-year periods. The early-2025 sustainability index fell less than the broader market during a drawdown — the opposite of what 'ESG underperforms' critics often claim. There is no general performance penalty for ethical screening that the data supports.

Read the prospectus methodology document, pull the top 25 holdings, and check exposure to the five healthcare-specific ethical flashpoints (insulin pricing, opioid litigation, single-supplier monopoly pricing, drug-trial transparency, PE-adjacent healthcare ownership). Compare the fund's holdings against unscreened sector ETFs to verify the screen is actually doing the work the fund name implies.

ARHI launched in February 2025 as a coalition of private-capital healthcare investors committing to patient-centered standards. The public member list is a useful starting reference for the retail investor evaluating which institutional capital pools publicly claim ethical guardrails on healthcare positions — coalition membership is a claim, not a substitute for due diligence.

No — 88% of global retail investors still report interest in sustainable investing per Morgan Stanley's 2026 survey, despite roughly $27 billion in Q4 2025 ESG-fund outflows and 192 anti-ESG bills proposed across US state legislatures during 2025. The greenhushing trend changed how fund marketing is positioned more than how the underlying screens operate. The work has moved from the label to the methodology document.

The 2024-2025 peer-reviewed literature (Georgetown Law Denny Center, AMA Journal of Ethics) documents that PE ownership in healthcare correlates with worse patient outcomes, higher costs, and reduced access. Most retail investors do not directly hold PE funds, but the publicly-traded PE firms and PE-acquired healthcare facility operators flow into broad-market funds and large-cap index funds, so the exposure is often indirect rather than absent.