Leveraging Technology: The Future of Financial Services

The question I get more often than I expected from clients in 2026 is some version of fintech vs traditional banking: should I move my checking account to a fintech, or stay with my bank? The honest answer is that it depends on four things — the kind of services you actually use month-to-month, the deposit-insurance posture of the institution holding your money, whether your fintech provider is a chartered bank or a partner of one, and how the rest of your financial plan (taxes, planning, advice, the human-judgment work) fits around the account. The market return on your savings cash next month is not on that list. It almost never is.

This is a guide to the impact of fintech on financial services for a U.S. household in 2026 — what fintech actually is, how the offerings differ from a traditional bank, the eight or so sub-sectors most readers will encounter, what artificial intelligence is doing inside the products, what embedded finance means in practical terms, where the open-banking rule actually sits with regulators today, and what the investor angle is (without recommending a single ticker, because that is not what a planner does in a blog post). Where individual circumstances matter most, the right answer is the one your own planner gives you after looking at your full situation.

What fintech actually is (and what it isn't)

Fintech — short for financial technology — is the application of software, data, and modern user-experience design to the delivery of banking, payments, lending, investing, and insurance services. It is not a single industry or a single company; it is a layer of capability that has accumulated across many products. Some fintechs are chartered banks. Most are not — they partner with chartered banks for the FDIC-insured deposit account behind the app. That distinction matters, and I will come back to it.

Fintech investment recovered in 2025 after a three-year slump. Global fintech funding hit $116 billion across 4,719 deals in 2025, up from $95.5 billion in 2024 — the first up-year since 2021, with the Americas leading at $66.5 billion. There are now 313+ fintech unicorns globally as of January 2026. The segment is not a flash in the pan, but it is also not uniformly successful — funding concentrated heavily into AI bets while overall deal volume hit a post-2017 low. The shape of the market in 2026 is fewer, larger, AI-focused fintech investments rather than a wide-spray scaling phase.

What fintech is not is a substitute for financial planning. A great app is not a financial plan, and a 12-second account-opening flow is not the same thing as a tax-aware decision about where to hold a given asset. Both can be true at once: fintech improves the product layer, and a household still needs the planning layer. Most of the mistakes I see come from confusing the two.

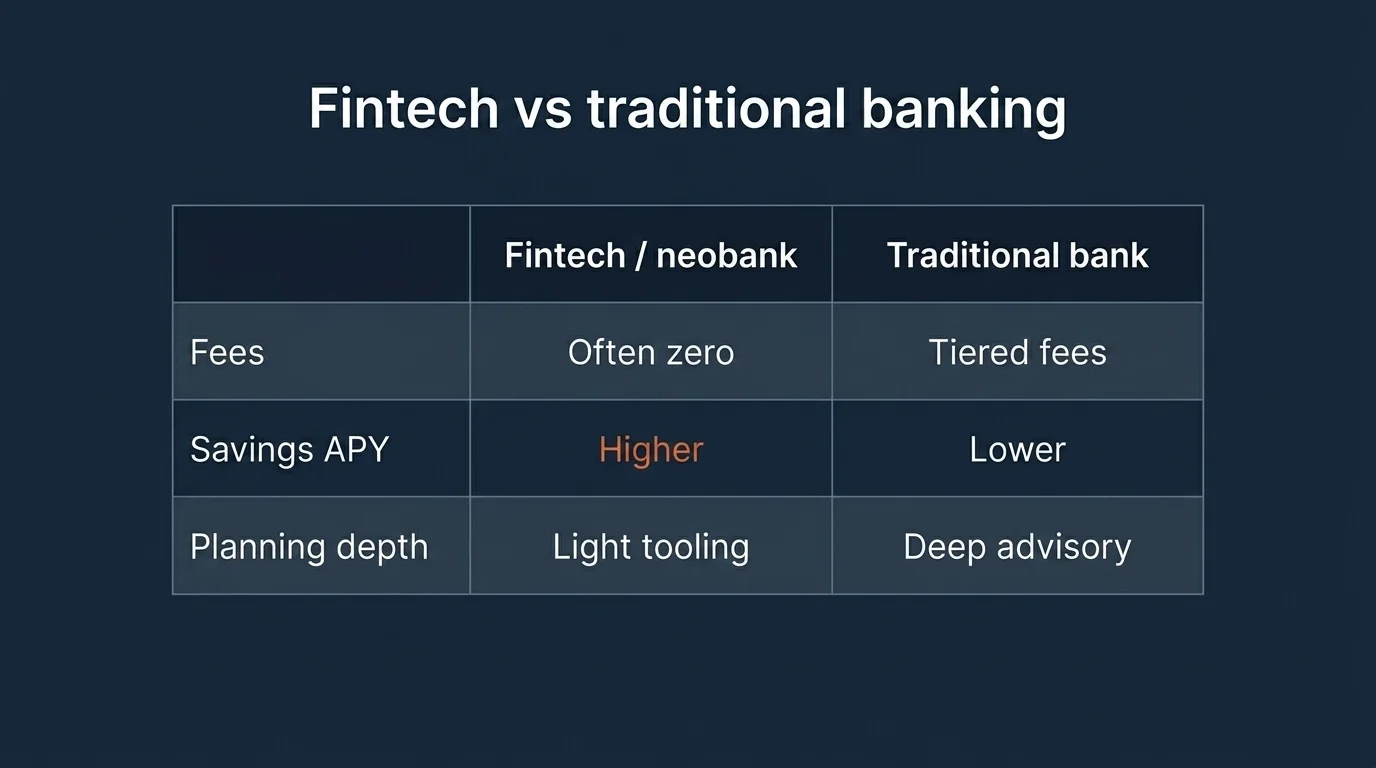

Fintech vs traditional banking: a household comparison

The "fintech vs traditional banking" framing is largely retired inside the industry, where the answer is increasingly "both, and they are converging." Traditional banks have acquired roughly 150 fintech firms over the past decade, and the consumer experience most readers have today already involves fintech infrastructure inside a bank product (or a bank's balance sheet inside a fintech product). For a household decision, the framing is still useful, but the trade-offs are not what they were five years ago.

| Dimension | Fintech / neobank | Traditional bank |

|---|---|---|

| Account opening | Minutes, fully digital | Often in-branch or multi-day digital with paperwork |

| Monthly fees | Frequently zero on basic accounts | Tiered; fee waivers tied to balance or direct deposit |

| ATM and branch access | App-based ATM finder; rarely owns branches | Branch network; ATM network; cash deposits |

| Savings APY | Often higher than national bank averages | Often lower; high-yield options exist but require activation |

| Customer service | Chat, in-app messaging, sometimes 24/7 | Phone, branch, app — usually in business hours |

| Deposit insurance posture | Through partner bank; verify coverage in disclosures | Direct FDIC coverage on chartered-bank deposits |

| Planning and advisory depth | Limited — robo and tooling, light human advice | Deeper for HNW segments; private banking, trust, and CFP relationships |

| Lending breadth | Strong on personal lending and BNPL; thinner on mortgages and small business | Full breadth — mortgage, HELOC, small business, credit |

The cost story is real. Neobanks operate roughly 60% cheaper than traditional banks daily, and digital bank spin-offs have cut operating costs by up to 70%. That cost advantage shows up partly as fee-free checking and higher savings APY, and partly as the funding base for product velocity. Fintech revenue grew roughly 21% in 2024 versus about 6% for the broader financial sector, and fintech is forecast to grow 15% annually through 2028 against 6% for traditional banks.

The "what is your money sitting in" question matters more than most readers realize. When a fintech is not itself a chartered bank, the FDIC-insured deposit account is held at a partner bank, and the FDIC coverage runs to that bank — not to the fintech as a brand. If the fintech fails but the partner bank does not, your deposit is generally fine. If the fintech's record-keeping is bad enough that ownership cannot be reconstructed cleanly (this has happened), recovery becomes complicated even when the underlying deposit is technically insured. Read the disclosures. The phrase to look for is "Fintech name is a financial technology company, not a bank. Banking services provided by Partner Bank, Member FDIC."

Plaid's 2026 fintech survey reports that 77% of consumers say their bank must connect to the apps they already use. That number is the structural answer to the "fintech vs banking" question: most households end up with both, connected through data-sharing, and the boundary between them is increasingly an interface choice rather than a switching choice.

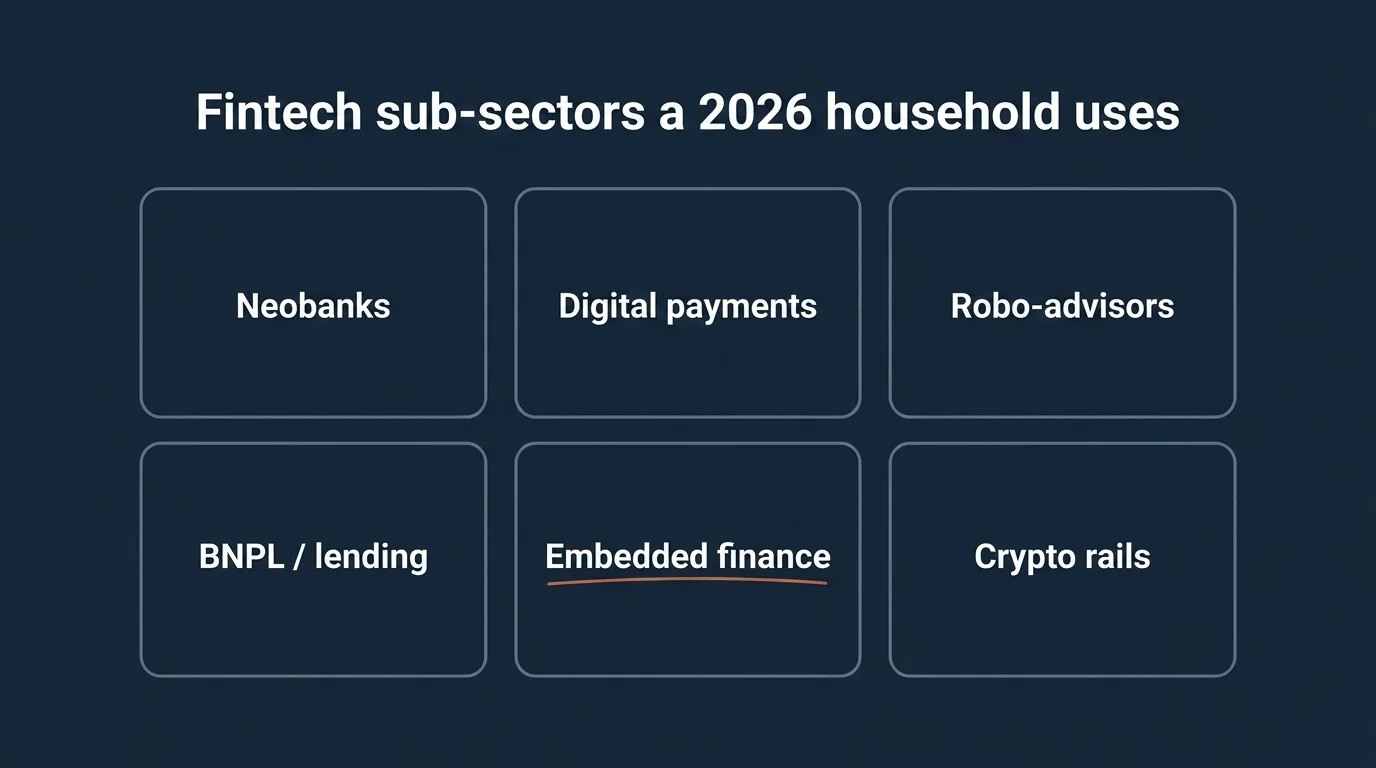

The fintech sub-sectors a 2026 household actually uses

It helps to break "fintech" into the categories you will actually encounter, because the household calculus is different in each. The named companies below are illustrative — they are the brands you will see most often in coverage of each sub-sector. None of this is a recommendation. Sizing any one of them in your portfolio or financial plan belongs to a planner who knows your full situation.

- Neobanks — digital-first checking and savings without a branch network. Chime is the largest U.S. neobank with more than 22 million users and is expected to IPO in 2026; Revolut, the European-origin equivalent, hit a $75 billion valuation in November 2025, up from $33 billion the year before. Nubank dominates Latin America. The household question with a neobank is not "is the app good" — it usually is — it is "is this the right institution for my emergency fund and my main paycheck account, given the planning layer I want around it?"

- Digital payments — payment infrastructure used by merchants and, in some cases, directly by consumers. Stripe, Block (the parent of Cash App), Adyen, and Wise are the names that show up most often. For most households, the relevance is that these companies sit behind the checkout flows and peer-to-peer transfers you already use.

- WealthTech and robo-advisors — automated portfolio construction and rebalancing. Robo-advisors are good at the basics: index-based asset allocation, automated rebalancing, low fees, and basic tax-loss harvesting. They are weaker on the parts of planning that require human judgment — Roth conversion sequencing, ACA-bridge income management, multi-account asset location, decisions tied to life events the algorithm has no context for. Use them as a tool inside a plan, not as a substitute for the plan.

- Lending and BNPL (buy now, pay later) — Affirm, Klarna, Prosper, LendingClub. BNPL is the category that has done the most damage to household finances I have seen up close. The product makes a $400 dishwasher feel like four $100 decisions, and the person who took it does not always think of it as debt until the third or fourth one is open. Treat BNPL the way you would treat a credit card with no statement.

- InsurTech — Lemonade, Root, Hippo. Faster quotes, better claims-app experience, narrower product breadth than incumbents. The trade-off is usually a tighter underwriting box and a smaller agent network when something complex happens.

- RegTech — ComplyAdvantage, Chainalysis, others. You will rarely interact with these directly. They are the compliance and AML infrastructure that banks and fintechs run their operations through.

- Embedded finance infrastructure — Plaid, Marqeta, Unit, others. Again, you will not interact with these by name. They are the data-and-issuing rails that let non-financial apps offer banking-like features. Plaid in particular is the connective tissue most household budgeting apps and brokerage account aggregators use to read your bank data.

- Crypto and blockchain rails — Coinbase, and increasingly, traditional fintechs entering stablecoin and blockchain settlement. Klarna (post-IPO September 2025 at roughly $19.65 billion valuation) is launching a dollar-backed stablecoin on a Stripe-related blockchain for everyday payments. Stripe (~$106 billion valuation) is rolling out Tempo, its layer-1 blockchain, in 2026. For most households, this is background — but the rails being built will affect cross-border payments and merchant settlement in the next two to three years.

AI in fintech: what changed in 2025–2026

Generative AI moved from pilot phase to production in financial services over the last eighteen months. NTT DATA reports that 58% of banking organizations have fully implemented generative AI in at least one function (up from 45% in 2023). IBM's Global Banking Outlook reports that 78% of banks are now adopting generative AI tactically, up from 8% in 2024. The shift in 2026 is from generative to agentic AI — systems that take actions inside defined boundaries rather than only producing text — with forecasts of 20% operational efficiency gains and AI-leading banks earning 15% greater market share.

McKinsey estimates the generative AI value pool in banking at $200 billion to $340 billion annually — equivalent to 9 to 15% of operating profits. AI-driven banking savings are projected to scale from $120 billion annually in 2025 to $500 billion by 2030.

The use-case adoption numbers tell you where the technology is actually working today: 90% of institutions use AI for fraud detection, 82% for algorithmic trading, 73% of wealth firms use AI in robo-advisor portfolio management, and 64% of U.S. banks use AI for anti-money-laundering pattern detection. In dollar terms, investment into AI fintech companies grew from $12.1 billion in 2024 to $16.8 billion in 2025 across 1,334 deals.

What this means inside the product you actually use: faster fraud holds and faster releases, better-tuned credit decisions on cash-flow data instead of FICO alone, and a customer service experience that increasingly starts with a chat interface that can take action — schedule a transfer, dispute a charge, freeze a card — rather than only answering questions. The honest version: it is genuinely good for routine work and still bad for anything that requires the planning context an AI does not have. A chatbot can dispute a transaction. It cannot tell you whether a Roth conversion makes sense in your tax bracket this year.

Embedded finance explained

Embedded finance is what happens when the financial product disappears into the non-financial app or platform you were already using. Shopify offering working-capital loans to merchants directly inside the Shopify dashboard. Uber paying drivers via an in-app wallet that doubles as a debit account. The Apple Card, issued through Goldman Sachs and integrated into the iPhone Wallet. Marqeta-powered card programs inside a hundred different consumer apps you use without realizing the card processor is the same.

The transaction value involved is no longer small: embedded finance moved $2.6 trillion in 2023, with forecasts of approximately $7 trillion by 2026. BCG estimates a North America plus Europe TAM of $185 billion across payments, capital, accounts, and card issuing. McKinsey's customer-economics research finds companies offering embedded finance see 2-5x higher customer lifetime value and 30% lower acquisition costs — which is why the model is spreading.

For a household, the practical implication is that more and more of your financial activity will route through interfaces that are not branded as financial. That is convenient. It is also worth attention. The same questions that apply to a neobank apply to embedded finance: who actually holds the deposit, what are the FDIC posture and the disclosures, what is the dispute process, and what happens to the data your activity generates? Read the in-app fine print the same way you would read a bank disclosure.

US regulatory snapshot: where Section 1033 sits in April 2026

Most general explainers refer to "open banking" as if Section 1033 of the Dodd-Frank Act — the CFPB's personal financial data rights rule — has gone into effect. As of April 2026, that is not the current status, and the distinction matters for both consumer rights and embedded-finance economics.

The CFPB finalized Rule 1033 in October 2024, with phased implementation through April 2026. The rule was then placed under reconsideration: the CFPB published an Advance Notice of Proposed Rulemaking on August 22, 2025, reopening four issues — representative definition, fee assessment, data security, and privacy threat model — and is preparing an interim final rule. American Banker's reporting indicates the interim final rule may permit banks to charge fees to fintechs for consumer data access — a structural shift that would change the economics of data aggregators like Plaid, embedded-finance providers, and any fintech app that reads bank account data.

For a household reading this in 2026: the spirit of open banking — your right to share your own financial data with the apps and providers you choose — is settled policy direction. The mechanics — fee provisions, data-format standards, security requirements, dispute handling — are in flux. If you are using a budgeting app or a brokerage aggregator that relies on bank-data access, watch the next round of CFPB rulemaking. The product you depend on may change pricing or coverage when the interim rule lands.

State-level money-transmitter licensing remains the other regulatory layer to know. Most U.S. fintechs operate as state-licensed money transmitters across all states they serve, which is a patchwork compliance burden and a real reason fintech rollouts often arrive in your state before or after others. The OCC's federal fintech charter remains a smaller path that few firms have used.

Investing in fintech as a theme: what to know, what not to do

This is the section where the original version of this article wandered into ticker recommendation territory. I am not going to do that, because that is not what a planner does in a blog post.

What I can say neutrally: the publicly traded names that show up most often in fintech-sector coverage include PayPal, Block, SoFi, Affirm, Coinbase, Robinhood, Adyen, and Nu Holdings. The ETFs that bundle fintech equities — ARKF, FINX, IPAY among them — exist, with different methodologies, expense ratios, and concentrations. The 2026 IPO pipeline includes Chime (the 22-million-user neobank), and Stripe is widely covered as a pre-IPO candidate at a roughly $106 billion valuation. Plaid completed an $8 billion private round in 2026.

That is the universe. The household question is not "which of these to buy." The household questions are: how much of your portfolio do you want exposed to the fintech theme at all (versus broader U.S. or global equity that already includes most of these names); whether direct stock, an ETF wrapper, or a mutual fund is the right vehicle for your account type and tax situation; and how the answer interacts with your existing holdings, tax bracket, and time horizon. Those are sizing-and-sequencing questions, and they belong to the planner who is fiduciary to you.

A planner-side observation worth making: fintech as a sector has historically had higher beta than the broader financial sector and a much different revenue trajectory (fintech ~21% revenue growth in 2024 vs ~6% for traditional financials, with fintechs forecast at 15% annual growth through 2028). Higher growth and higher beta are not free lunches. Sizing matters more than which name.

What this means for your household

A short summary of the practical takeaways, written the way I would summarize them to a client across the desk.

- The fintech-vs-bank question is mostly a settled question. Most households end up with both, connected via data-sharing. The structural decision is not "which one" but "what sits where, and is the planning layer covered."

- A neobank or fintech account for spending and high-yield savings is reasonable for many households, if you understand the FDIC posture (chartered bank vs partner-bank) and have read the disclosures.

- Robo-advisors and AI-powered tools handle the basics well. They do not replace tax-aware planning, asset location across taxable and tax-advantaged accounts, withdrawal sequencing in retirement, or anything tied to life events. Use them as tools inside a plan.

- BNPL is a credit product. Treat it as one. The friction-removal that makes it convenient is the same friction-removal that lets it accumulate quietly in households that did not budget for it.

- Embedded finance is the direction of travel. It is fine. The disclosures it sits on are not always as easy to find. Read them.

- The "investing in fintech" question is a sizing question and a tax-aware-account question, not a ticker question. If you want exposure, the conversation belongs with your planner. If you do not have one and you are seriously deploying capital, getting one is the first step.

What I'd ask a planner before moving accounts

If you are sitting across the desk from your own planner — or interviewing one — the questions worth asking before any fintech-related move are roughly these.

- Is the fintech account holding my deposit a chartered bank itself, or is it operating through a partner bank? What is the FDIC-coverage chain and what would happen to my deposit if the fintech (not the bank) failed?

- Where does this account sit in my asset-location plan? Is it the right wrapper for the cash it holds, given my tax bracket and the alternative — a high-yield savings account at the bank, or a Treasury money-market fund in a brokerage?

- If I am using a robo-advisor, is its tax-loss harvesting actually generating value at my income level, or is it noise that complicates my tax return without enough offset?

- If I am exposed to fintech equities or a fintech ETF, what percentage of my total equity allocation is that — and does it overlap with what I already own through broad index funds?

- If I am being offered a BNPL option at checkout, is this a use of debt I would have decided to take if it had been presented as "open a $400 line of credit"? If not, why is the framing changing the answer?

These are the questions I work through with clients. None of them have a generic correct answer. All of them have a correct answer for you, and the work of finding it is what your planner is for.

That is the impact of fintech on financial services in 2026, framed for a U.S. household. None of the above is individual financial advice. All of it is starting material for the conversations you should be having with the people licensed to look at your specific facts.

Frequently Asked Questions

Fintech — short for financial technology — is the application of software, data, and modern user-experience design to the delivery of banking, payments, lending, investing, and insurance services. It is transforming the industry by lowering operating costs (neobanks operate roughly 60% cheaper than traditional banks), shortening the time and friction of routine financial activity, and embedding financial services into non-financial apps and platforms. As of 2026, fintech revenue is growing roughly 21% annually versus ~6% for traditional financial services, and global funding hit $116 billion in 2025 across 4,719 deals.

The publicly traded names most discussed in fintech sector coverage include PayPal, Block, SoFi, Affirm, Coinbase, Robinhood, Adyen, and Nu Holdings. ETFs that bundle fintech equities exist with different methodologies and concentrations. The 2026 IPO pipeline includes Chime (22M+ users) and Stripe is widely covered as a pre-IPO candidate. The relevant household questions are how much fintech-theme exposure makes sense given your existing portfolio, which vehicle fits your account type and tax situation, and how the answer interacts with your tax bracket and time horizon. Sizing and sequencing decisions belong with a licensed financial advisor.

The most consequential current item is CFPB Rule 1033 — the personal financial data rights ('open banking') rule — finalized in October 2024 with phased April 2026 implementation. As of April 2026 the rule is stayed and under reconsideration; the CFPB issued an Advance Notice of Proposed Rulemaking in August 2025 and is preparing an interim final rule that may permit banks to charge fees to fintechs for consumer data access. Other ongoing issues include state-by-state money-transmitter licensing, OCC fintech charter status, AML/KYC obligations, and SEC oversight where fintechs touch securities or crypto.

Embedded finance integrates banking, payments, lending, or insurance directly into non-financial apps and platforms — Shopify offering working-capital loans to merchants, Uber paying drivers via an in-app wallet, or the Apple Card issued through Goldman Sachs and integrated into the iPhone Wallet. McKinsey reports that companies offering embedded finance see 2-5x higher customer lifetime value and 30% lower acquisition costs. Transaction value reached $2.6 trillion in 2023 and is forecast to reach approximately $7 trillion by 2026. BCG estimates a $185 billion North America and Europe TAM across payments, capital, accounts, and card issuing.

Generative AI moved from pilot to production in 2025–2026. NTT DATA reports 58% of banking organizations have fully implemented generative AI in at least one function; IBM reports 78% of banks are adopting it tactically. Concrete use cases include fraud detection (90% of institutions), algorithmic trading (82%), AI-powered robo-advisor portfolio management (73% of wealth firms), and AML pattern detection (64% of U.S. banks). McKinsey estimates the gen AI value pool in banking at $200–$340 billion annually. The 2026 shift is from generative to agentic AI — systems that take bounded actions rather than only producing text.

No. As of April 2026 the rule is stayed and under reconsideration. The CFPB finalized Section 1033 in October 2024 with phased implementation slated for April 2026, but new agency leadership reopened the rulemaking via an Advance Notice of Proposed Rulemaking in August 2025 and is preparing an interim final rule. The interim rule may permit banks to charge fees to fintechs for accessing consumer financial data — a structural change for data aggregators and embedded-finance providers.

By valuation, the largest include Stripe (~$106B), Revolut ($75B), Nubank, Adyen, and Plaid (which completed an $8B private round in 2026). Public fintechs frequently covered include PayPal, Block, SoFi, Affirm, Coinbase, Robinhood, and Klarna (which IPO'd in September 2025 at roughly $19.65B). The 2026 IPO pipeline includes Chime — the largest U.S. neobank with 22M+ users. Globally, there are 313+ fintech unicorns as of January 2026.