The Morality Maze: Ethical Dilemmas in Wealth Management and Investment

The number worth opening with is not the bitcoin price equivalent for ethical investing. It is the outflow data: US ESG-designated mutual funds and ETFs have now posted 14 consecutive months of net outflows through January 2026, with $935 million leaving in that month alone. Total US ESG assets stood at $598.16 billion in March 2026, down $32.86 billion over the trailing period, with roughly $27 billion flowing out in Q4 2025. One hundred ESG-labeled funds in the United States closed in the twelve months ending January 2026 — a 12% year-over-year contraction in the labeled-fund universe.

What this measures is the institutional retreat from products carrying the ESG label specifically. What it does not measure is investor interest in the underlying ideas. Morgan Stanley's 2026 survey, cited by NerdWallet, found 92% of individual investors continued to express interest in sustainable investing during the same period. The label is unwinding. The behavior — picking investments with some moral or social criterion in addition to expected return — is not.

This is a working guide to ethical investing in 2026: what the words mean (and where they overlap), the four screening approaches anyone in the category is actually using, the specific funds and ETFs worth knowing by name, what the 2025-2026 regulatory shift actually changed, what the performance data does and does not say, and a 4-step walkthrough for a beginner who wants to start building a portfolio under these criteria. It is education, not personalized advice. Verify any expense ratio or top-holdings figure with the fund issuer before you act on it; the data in this article is current at the time of writing and will drift.

The terminology, briefly: ESG, SRI, impact, ethical

Four words get used as if they meant the same thing, and they do not. The distinctions matter when you read a prospectus.

- ESG investing scores companies on environmental, social, and governance metrics — usually based on third-party ratings (MSCI, Sustainalytics, Morningstar). It is the broadest category and the one that has driven most of the institutional product flow since 2018.

- Socially responsible investing (SRI) is the older umbrella term and typically refers to exclusionary screening — leaving out tobacco, weapons, fossil fuels, alcohol, gambling, adult content. It pre-dates ESG by decades and is closer to "negative screening" than to integrated scoring.

- Impact investing is the most demanding of the four. It targets measurable real-world outcomes (units of affordable housing built, megawatts of clean energy deployed, water-treatment capacity added) and accepts that some impact-targeted positions will have lower expected returns than the market. Impact investors care about additionality — whether the investment caused the outcome, or whether the outcome would have happened anyway.

- Ethical investing is the broadest informal umbrella — used to cover all of the above and also faith-based investing, values-based investing, and SRI-style exclusionary screens that fall outside the standard ESG taxonomy.

The headline read for a retail investor: the four words describe different rigor levels along a spectrum. Exclusionary SRI is the cheapest and broadest. ESG integration is the most common in institutional portfolios. Impact investing is the highest-conviction and the hardest to verify. Use the word that actually describes the methodology of the fund you are holding, not the word the marketing brochure uses.

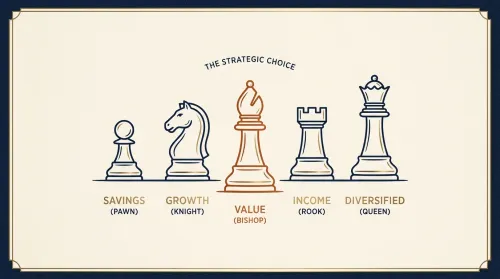

The four approaches to ethical investing

Most coverage of ethical investing collapses into a single approach (usually ESG integration) and then judges the entire category by how that one approach performs. The cleaner taxonomy, used in academic and institutional literature for over a decade, has four distinct approaches. A fund picks one (sometimes two), and the right approach depends on what the investor is actually trying to do.

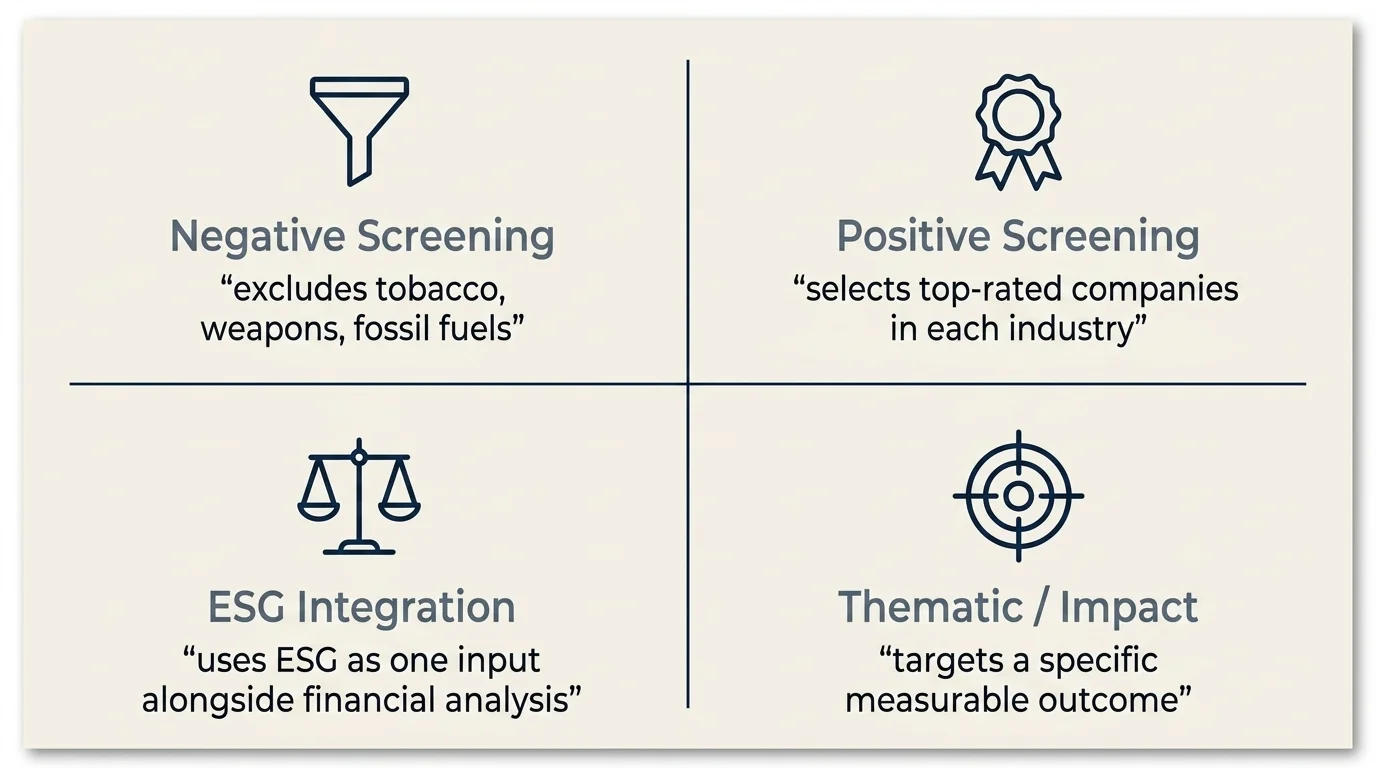

| Approach | What it does | What it does not do | One example fund |

|---|---|---|---|

| Negative / exclusionary screening | Excludes specific industries (tobacco, weapons, fossil fuels, adult content) from a broad-market portfolio | Does not actively select for positive impact — it just removes the worst offenders | iShares MSCI KLD 400 Social ETF (DSI) — broad-market US equities minus the worst-rated companies on ESG |

| Positive / best-in-class screening | Selects companies that score in the top tier on ESG criteria within each industry | Does not exclude entire industries — a top-tier oil company can still be held | Parnassus Core Equity (PRBLX) — large-cap US equities selected on a quality-plus-ESG screen |

| ESG integration | Uses ESG factors as one input alongside traditional financial analysis; no explicit exclusion or selection rule | Does not commit the portfolio to a particular ethical outcome — ESG is one signal among many | Vanguard ESG US Stock ETF (ESGV) — broad-market US equities with ESG-screen overlay |

| Thematic / impact investing | Targets a specific outcome (low-carbon, clean water, affordable housing, financial inclusion) with measurable metrics | Does not promise market-equivalent returns — by design, accepts tracking error against the broad market | iShares MSCI ACWI Low Carbon Target ETF (CRBN) — global equities tilted toward lower carbon-intensity firms |

A few honest caveats worth pulling out of that table. First: most funds carrying an "ESG" label are doing ESG integration or positive screening, not impact investing. The label "ESG" tells you the category. It does not tell you the rigor. Second: within the impact column, sector-specialized funds exist for clean energy, water infrastructure, financial inclusion, and healthcare — for the healthcare-specific niche of ethical investing, the sibling piece on ethical dilemmas in healthcare financing covers the named funds and sector-specific screening criteria. Third: the four approaches can be combined inside a single portfolio. A reasonable retail allocation might use ESGV for the broad-market core, PRBLX for a quality-tilt slice, and CRBN as the climate-specific position — three approaches, one portfolio.

Specific ethical ETFs and funds to know (2026)

The list below is not a buy recommendation. It is the working roster of named funds across the four approaches that a retail investor researching the category should at least know exists. Verify the current expense ratio, top holdings, and methodology document on the fund issuer's site before any decision — fund data drifts, and the 2025-2026 retreat means some funds are also actively repositioning. Tickers and approximate expense ratios as of the research window:

- Vanguard ESG US Stock ETF — ESGV — ESG integration; broad-market US equities; expense ratio around 0.09%. The cheapest broad-market ESG-screened US equity ETF.

- iShares ESG Aware MSCI USA ETF / iShares MSCI USA ESG Select — SUSA — positive screening; large-cap US equities selected on best-in-class ESG criteria.

- iShares MSCI KLD 400 Social ETF — DSI — exclusionary screening; the oldest broad-market socially-screened US-equity index ETF, with a 1990 inception (predates the term "ESG"). Drops the lowest-rated companies and entire excluded industries.

- iShares MSCI ACWI Low Carbon Target ETF — CRBN — thematic/impact; global equities tilted toward lower carbon-intensity firms within each sector.

- Parnassus Core Equity — PRBLX — positive screening combined with a quality factor; one of the older mutual-fund options in the category with a defensible long-term track record.

- Calvert US Large-Cap Core Responsible Index — CSXAX (and similar Calvert vehicles) — positive screening; large-cap US equities selected on Calvert's proprietary ESG framework.

Faith-based options sit in their own column and use distinct screens — covered in a separate section below.

Verify before you act. Fund expense ratios, top holdings, and methodology change. The data in this article is current at the time of writing and will drift. Read the prospectus and the current fact sheet on the fund issuer's website, and remember that this article is education — not personalized investment advice. For your specific household, talk to a licensed advisor who can see your tax bracket and full balance sheet.

What changed in 2025-2026: the ESG retreat

A retail investor who has not been following the policy news may not know how much the regulatory scaffolding underneath ESG investing has changed in the past eighteen months. The headlines worth knowing:

- The SEC withdrew the proposed ESG disclosures rule. In February 2026, the Commission formally withdrew the proposed ESG-disclosures rule and the shareholder-submissions proposal outright. The compliance-driven scaffolding that pushed ESG adoption from 2021 through 2023 is no longer being built.

- The SEC is moving to rescind the climate-disclosure rule. The Commission told the Court of Appeals it will no longer defend the Biden-era climate-disclosure rule and is moving toward formal rescission.

- The Fund Names Rule is under review. Rule 35d-1, which was supposed to crack down on funds calling themselves "ESG" without an 80% asset match, was placed under review by the SEC in March 2026. One of the main anti-greenwashing tools is now in limbo.

- ESG shareholder proposals dropped 47% in the 2026 proxy season — 184 proposals filed by mid-March 2026 versus 355 the prior year, after SEC guidance on Rule 14a-8(i)(5) made social and ethical proposals easier for companies to exclude.

- Anti-ESG state legislation has passed in 20+ states by 2026, with pension funds in Texas, Florida, West Virginia, and Oklahoma mandating divestment from BlackRock, State Street, and Vanguard ESG products. The same Harvard Law CorpGov forum analysis tracks the state-by-state pattern.

- A fiduciary-duty litigation line has opened. Emerging cases in 2025-2026 test whether ESG mandates carry "unconstitutional vagueness" under ERISA fiduciary standards — the legal claim is that ESG criteria lack the objective definition fiduciary duty requires. The case law is unsettled.

- "Greenhushing" has replaced greenwashing as the dominant corporate behavior. The Conference Board reports that 80% of large US and multinational firms revised ESG strategies in 2025. Companies are systematically deleting the word "ESG" from filings — Target, for example, went from 62 ESG mentions in its 2023 corporate filings to zero in 2025.

What this means for the retail ethical investor is not "ethical investing is dead." It is "the label is unreliable as a discovery shortcut, and the regulatory disclosure trail is thinner than it was two years ago." The job of identifying a fund whose holdings actually advance the outcome the investor cares about has gotten harder, not impossible. The methodology document inside the prospectus is doing more of the work the fund name and the regulatory filings used to do.

It is also worth noting, against the headline retreat: global ESG AUM was still approximately $35.48 trillion in 2025 and is projected to reach $42.16 trillion in 2026 (Precedence Research), with North America holding about 37% of the share. The US retail and labeled-product retreat is happening against a global base that is still growing. The story is "US labeled flows reversed," not "the category collapsed."

Related Article: Finance Mentor vs Sponsor: What Actually Compounds a Career

Do ethical funds underperform?

The honest answer, with the data: not on average over multi-year windows, and yes in specific dispersion years.

The cleanest cross-asset signal is IEEFA's 2025 analysis, which found ESG equity and fixed-income funds matched or outperformed traditional peers across most time horizons through 2025. The single most-cited individual-investor-relevant data point is Morgan Stanley's 2026 analysis (cited via NerdWallet): $100 invested in a representative sustainable fund in 2018 grew to roughly $162 by early 2026, against $152 for a comparable traditional fund. Roughly a one-percentage-point annualized advantage over an eight-year window.

What that data does not tell you is how the category performed in specific dispersion years. 2022 is the obvious one — energy stocks ran sharply, and most ESG funds, which underweight or exclude fossil fuels, lagged the S&P 500 by material margins that year. The aggregate eight-year number absorbs that dispersion; an investor who looked at a one-year window of 2022 alone would have seen meaningful relative underperformance. The honest framing is that ethical-screened portfolios have produced market-comparable returns across multi-year horizons but will continue to have sector-tilt years in which they lag, particularly when energy or other excluded sectors lead.

What the data also does not tell you is whether any individual fund's stated screening methodology actually corresponds to its holdings. That is the methodology-document question, not the performance question, and it is where the work has actually moved post-2024.

Faith-based investing as its own column

Faith-based investing predates ESG as a category by decades and uses screens that often overlap with but do not equal ESG screens. The named fund families worth knowing:

- Catholic — Ave Maria Funds (Ave Maria Catholic Values Fund and others) screens against companies involved in abortion, pornography, Planned Parenthood support, and certain stem-cell research; Knights of Columbus Asset Advisors offers a parallel set of products built on US Conference of Catholic Bishops guidelines.

- Christian (broad) — Timothy Plan (one of the older Christian-screen fund families, with screens covering abortion, alcohol, gambling, pornography); GuideStone Funds, originally serving Southern Baptist pension assets, with screens consistent with conservative Protestant values.

- Islamic / Sharia-compliant — Amana Funds (Amana Income, Amana Growth — the largest US Sharia-compliant fund family); SP Funds (SPUS is the largest Sharia-compliant US-equity ETF). Both screen against interest-bearing securities (no banks or financial-services companies whose primary revenue is interest), conventional insurance, alcohol, tobacco, pork, weapons, gambling, and adult content. They also typically purify a small portion of dividend income corresponding to incidental non-compliant revenue.

The screens are stricter and more specific than typical ESG screens, and the resulting portfolios are concentrated by construction — a Sharia-compliant US-equity portfolio simply does not own most banks and consumer-finance companies, which materially affects sector exposure. Faith-based investors usually accept that concentration as a feature, not a bug.

Related Article: Youth-Led Financial Revolutions: Crowdsourcing as a Catalyst for Investment Innovation

Greenwashing to greenhushing: how to vet a fund now

The 2018-2023 problem in ethical investing was greenwashing — funds calling themselves ESG without the holdings to back it. The 2025-2026 problem is greenhushing — companies and funds removing the word "ESG" from filings to avoid political and regulatory friction while continuing to operate the underlying screens. The result is that the label is now an unreliable signal in both directions: a fund with "ESG" in its name may have weak screening, and a fund without "ESG" in its name may still be running rigorous ESG methodology.

The working due-diligence checklist that survives the label problem:

- Read the methodology document inside the prospectus. Not the marketing one-pager. The actual SEC-filed statement of additional information or fund methodology document — what is excluded, what threshold scores are used, who supplies the ESG ratings (MSCI, Sustainalytics, Morningstar, proprietary), and on what review cadence.

- Pull the top 10 holdings and the sector weights. Compare them to a broad-market index. If the top 10 holdings of an "ethical" fund are nearly identical to the S&P 500's top 10, the ethical screen is doing very little of the work the fund name promises.

- Check the third-party ESG rating of the fund itself. Morningstar Sustainability Rating, MSCI ESG Fund Rating, and Sustainalytics Fund Rating each score the underlying portfolio. The fund's own marketing may or may not align with what the third-party raters see.

- Note what was added or removed in the past 24 months. Funds rebrand. A fund that quietly dropped "ESG" from its name in 2024-2025 may still be running the same screen — or may have substantially loosened it. The prospectus amendments tell the story.

- For impact-marketed funds, ask the additionality question. Did the investment cause the outcome, or would the outcome have happened anyway? Impact funds with measurable, reported outcomes (CO2 avoided, units of affordable housing built, MW of renewable energy deployed) are doing the harder work. Impact funds with no measurable outcome report are mostly marketing.

The pattern: methodology beats label, holdings beat marketing, third-party rating beats issuer self-rating. None of this is new advice. It is just more important than it was when the label itself carried more disclosure weight.

A beginner's 4-step walkthrough

For a reader who has not yet held an ethical-screened position and wants to start:

- Pick the account type first. Taxable brokerage, Roth IRA, Traditional IRA, or workplace 401(k) — the tax wrapper is upstream of the security selection. Long-horizon ethical positions usually fit best in tax-advantaged accounts; rebalancing inside a tax-advantaged account does not generate capital-gains tax friction.

- Choose DIY or robo. Robo-advisors with ethical portfolios (Betterment's SRI portfolios, Wealthfront's socially responsible portfolios, Merrill Edge Guided Investing's ESG options) handle screen choice and rebalancing for a wrap fee — typically 0.25% on top of the underlying fund expenses. DIY using individual ETFs is cheaper but requires picking the screen approach yourself.

- Choose the approach. Negative screening (cheapest, broadest), positive/best-in-class (modest active component), ESG integration (most common institutional default), or thematic/impact (highest conviction, accepts tracking error). Most beginners are well-served by ESG integration with a broad-market ETF like ESGV as the core position.

- Build a simple 3-fund ethical portfolio. A defensible starting allocation looks like: a broad-market ESG-screened US equity ETF (ESGV or SUSA), a broad-market international ESG-screened equity ETF, and a sustainable bond ETF appropriate to the household's age and risk capacity. Specific allocations depend on the household. Three positions are sufficient to start; the fourth and fifth come later, deliberately, after the portfolio has run for a year and the household has seen its own behavior at the next drawdown.

The point of starting with three positions is the point of starting with anything in investing — too much complexity at the beginning produces neither better returns nor a more durable habit. The simple version that gets implemented beats the elegant version that does not.

Related Article: Red vs. Blue: The Battle of Colors in Investment Marketing

What would have to change for my view to change

For Elena to revise the framework above, two things would have to shift materially.

First: if greenhushing reaches a tipping point where the disclosure trail goes dark — where methodology documents are routinely stripped from prospectuses, third-party ESG raters lose access to portfolio data, and even the holdings-level analysis above stops working — then the "methodology, not label" discipline gets much harder to apply. The retail tools available are the methodology document, the holdings disclosure, and the third-party rating. If two of those three become unreliable, the category becomes less navigable for a self-directed retail investor, and the case for a fiduciary advisor with institutional research access strengthens substantially.

Second: if the fiduciary-duty litigation line resolves against ESG criteria being legally permissible inputs for ERISA-governed accounts, the workplace-401(k) shelf of ethical options will narrow materially. That would not change the underlying category, but it would change which accounts a household can use to express ethical preferences without legal friction. Most US retirement assets sit in ERISA-governed accounts; this is the part of the regulatory landscape worth watching most closely over the next eighteen months.

What this article does not tell you, and what it should not pretend to tell you, is what allocation, what specific tickers, or what wrap of tax-deferred versus tax-free accounts is right for your household. The category is navigable in 2026 with care and reading; the personalization is not. For decisions of any size, talk to a licensed fee-only advisor who can see the household's tax bracket, time horizon, and obligations alongside the methodology documents this article only summarizes. This is education, not personalized investment advice.

Frequently Asked Questions

Ethical investing means choosing investments based on moral or social criteria — environmental impact, labor practices, governance, faith principles — alongside expected return. It includes ESG investing, socially responsible investing (SRI), impact investing, and faith-based investing, each using different screening methods to select or exclude companies.

Not on average over multi-year windows. A Morgan Stanley 2026 analysis cited by NerdWallet found $100 invested in a representative sustainable fund in 2018 grew to about $162 versus $152 in a comparable traditional fund. IEEFA's 2025 analysis found ESG funds matched or beat traditional peers across most asset classes. Individual years — notably 2022 when energy stocks led — can lag because most ESG funds underweight excluded sectors.

ESG investing scores companies on environmental, social, and governance metrics, typically using third-party ratings. SRI is the older umbrella term and typically excludes 'sin' industries (tobacco, weapons, fossil fuels). Impact investing targets measurable real-world outcomes (units of affordable housing built, megawatts of clean energy deployed) and accepts that some positions will have lower expected returns. ESG is the broadest; impact is the most demanding.

Common broad-market ethical ETFs include Vanguard ESG US Stock (ESGV), iShares MSCI USA ESG Select (SUSA), iShares MSCI KLD 400 Social (DSI), iShares MSCI ACWI Low Carbon Target (CRBN), and Parnassus Core Equity (PRBLX). Faith-based options include Amana Funds (Islamic) and Ave Maria Funds (Catholic). Always verify current expense ratios and top holdings on the fund issuer's site before investing.

Yes, if you separate the politics from the product. US ESG-labeled funds posted 14 straight months of outflows through January 2026 and 100+ funds closed, but the underlying portfolios (clean energy, sustainable agriculture, well-governed companies) still exist — many are quietly rebranding as 'quality' or 'long-term' funds, a trend called greenhushing. The job is to read the methodology document and the holdings, not the label.

Greenhushing is the 2025-2026 corporate pattern of removing 'ESG' from filings and marketing to avoid political and regulatory friction while continuing to operate the underlying screens. Target, for example, went from 62 ESG mentions in its 2023 filings to zero in 2025. It is the opposite of greenwashing — and makes label-based fund discovery less reliable in both directions.

Negative or exclusionary screening (excludes specific industries like tobacco or weapons); positive or best-in-class screening (selects top-rated companies within each industry); ESG integration (uses ESG as one input alongside traditional financial analysis); and thematic/impact investing (targets a specific outcome like low-carbon or affordable housing with measurable metrics). Most ESG-labeled funds are doing integration or positive screening; impact investing is the most demanding.