Embracing Rational Decision-Making: The Psychology of Prudent Financial Choices

The FINRA Foundation's Sixth Wave National Financial Capability Study, released in July 2025, measured something worth pausing on: only 44% of US adults reported it was easy to pay their bills in 2024, down from 54% in 2021. Twenty-six percent of US adults spend more than they earn. Only 46% have a three-month emergency fund, down from 53%. Household financial stress is at a multi-year high in a measurable way, and the dominant advice on financial decision making is still some version of "make better decisions" — without the framework for how.

The harder, more honest framing is that financial decision-making is not a personality trait. It is a process. Households that hold to a process across both rising and falling markets, across both calm and stressed cash-flow periods, materially outperform households that do not — not because the process is sophisticated, but because the process is the same in every condition. The framework below is the one I would walk a planning client through in their first meeting. It is borrowed from a model the St. Louis Fed published in April 2026 for the personal-finance-education context, adapted for the actual money decisions households make. It is boring, and it works.

What financial decision making actually is

Financial decision making is the deliberate process of weighing alternatives against your goals, timeline, risk tolerance, and tax situation — using a repeatable framework instead of reacting to the latest market headline or marketing pitch. The emphasis on the word repeatable is the part that matters most. The point of a framework is not that any one decision becomes optimal; the point is that the process is the same in every condition, which is what keeps a household from making the worst version of a decision under stress.

"Rational" in this context does not mean Spock-like or emotion-free. It means a decision that weighs your specific situation — your tax bracket, your time horizon, your household obligations, the information you actually have — with deliberate attention to what each variable is contributing. Bounded rationality is not a failure to live up to a theoretical ideal. It is the working condition every household and every planner actually operates inside. The framework is built for it.

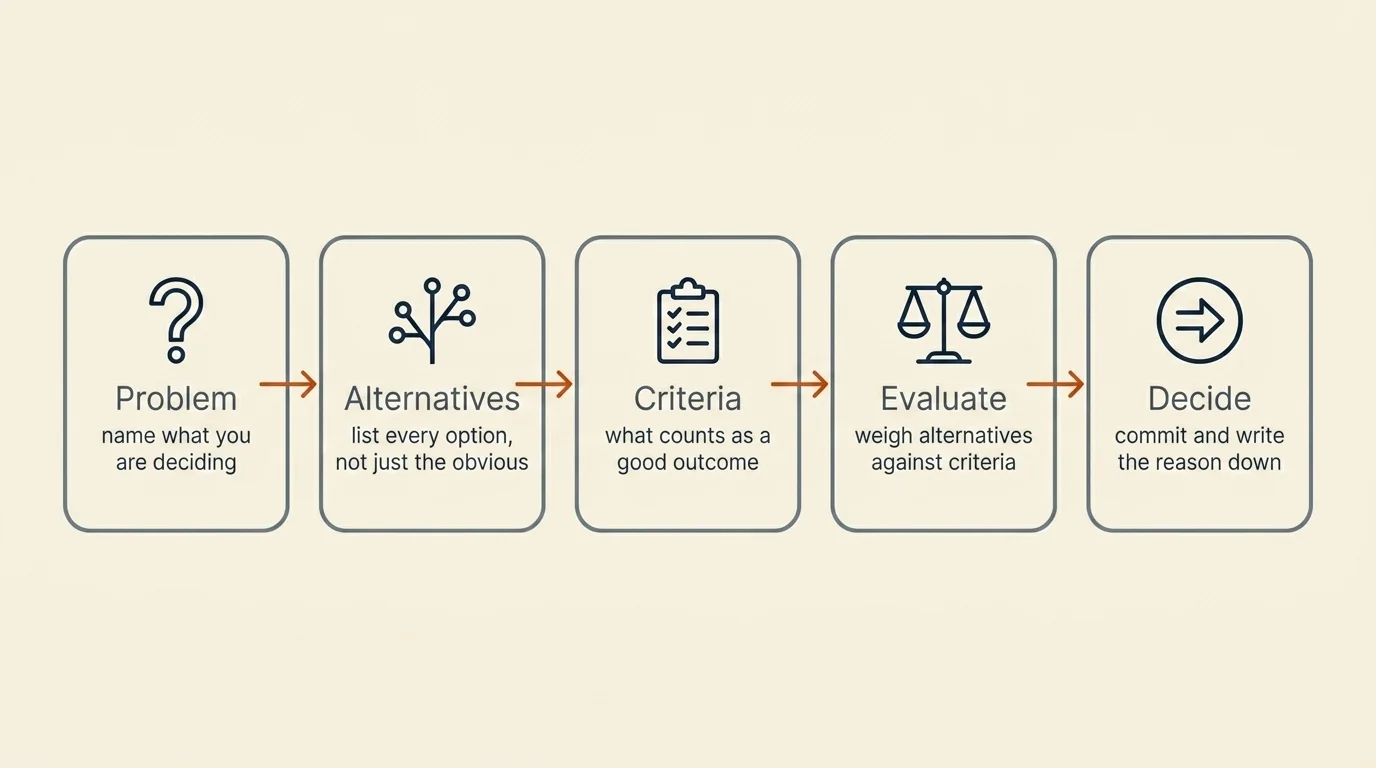

The PACED-adapted money decision framework

The St. Louis Fed's Open Vault piece from April 2026 uses the PACED model — Problem, Alternatives, Criteria, Evaluate, Decide — to teach economic reasoning in the personal-finance-curriculum context now mandated in 39 US states. The five steps map cleanly onto the household money decision and onto the planning conversation. The version below adds the planner-grade variables (tax, timeline, risk capacity) that the educational version is too general to name.

| Step | What the step actually is |

|---|---|

| Problem | State the decision out loud, in one sentence. "We need to choose between contributing $7,000 to a Roth IRA or paying down the $7,000 remaining on the auto loan." Not "what should we do about money." |

| Alternatives | Enumerate every viable option, including doing nothing and including the boring middle path. Most household decisions are framed as binary when they are actually three or four options. |

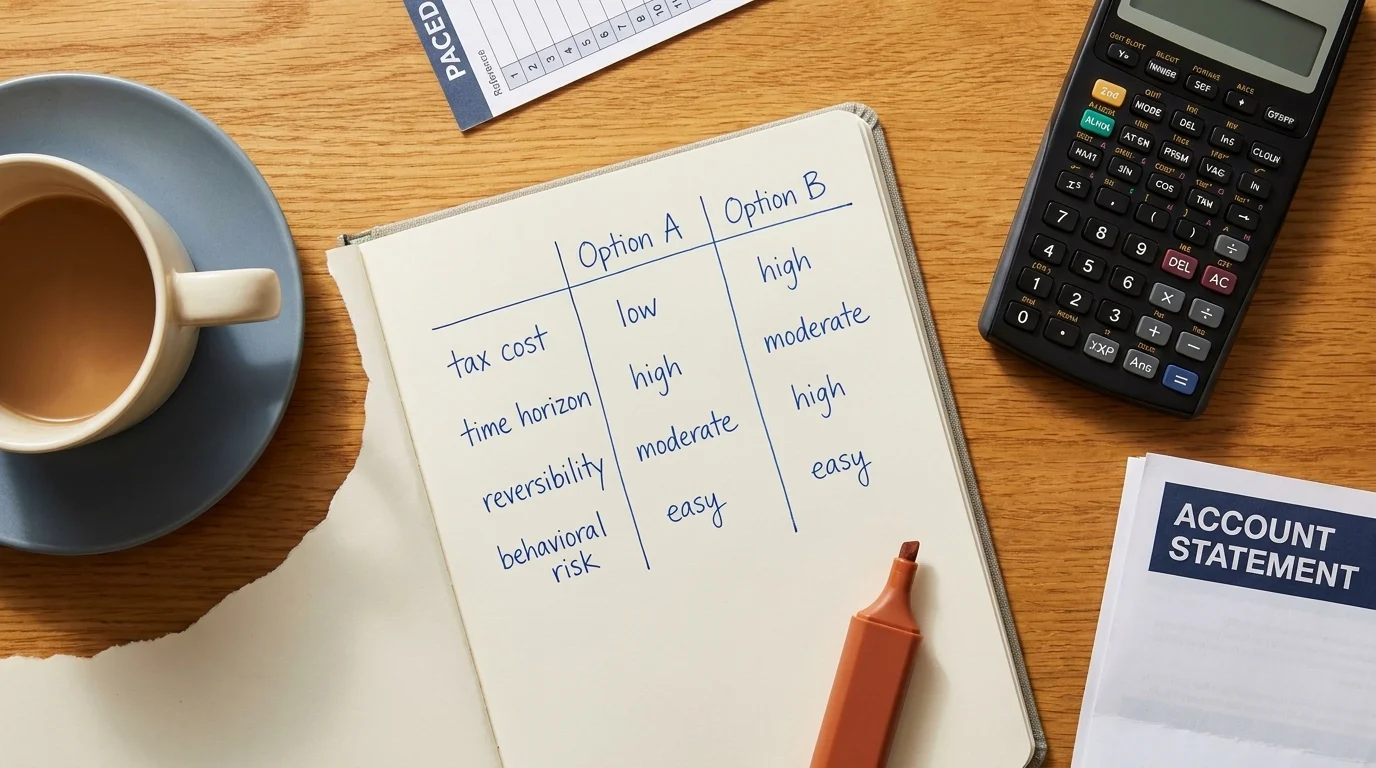

| Criteria | Write down the variables that matter. For most household decisions: marginal tax rate, time horizon, after-tax return, behavioral risk (what is the household actually going to do under stress), reversibility. |

| Evaluate | Score each alternative against each criterion. A back-of-envelope worked example almost always beats a vague "it feels right." Numbers do not have to be perfect to be useful. |

| Decide | Make the choice in writing, with the date and the trigger that would cause you to revisit it. The trigger is the part that survives changes in market conditions and household circumstances. |

A few honest caveats about the framework. First: it is not a substitute for the planning conversation. It is the structure that makes the planning conversation more productive. A client who walks into the office with the four criteria already written down has a different conversation than one who walks in with "we need to figure out money." Second: the framework works in proportion to how seriously the "decide in writing" step is taken. A decision held in the head is a decision the household has not actually made. Third: the trigger is the part most households skip and the part that prevents the most regret. Naming, in advance, what would cause you to revisit a decision is how you keep yourself from re-deciding it under stress every quarter.

Related Article: Ethical Considerations in Personal Finance and Healthcare Nexus

Six cognitive biases that derail money decisions (with worked examples)

The biases below are the ones I see most often across a planning desk. Each is named, each is connected to a worked household example, and each has a structural correction that does not require the household to be smarter — only to put the structure in place before the bias has the chance to operate.

- Anchoring — the tendency to weight the first number you see more than any subsequent number. Example: A house listed at $480,000 sets an anchor that makes $440,000 feel like a discount and $510,000 feel like a stretch — regardless of whether either number reflects fair value. Correction: write down your independent estimate of the fair number before you see the seller's price. Then compare. This is the same discipline a serious appraiser uses and the same one most household buyers skip.

- Loss aversion (Kahneman & Tversky, 1979) — losses hurt roughly 2.25 times as much as equivalent gains feel pleasant. Example: A household holds a losing stock position for three years past when the underlying thesis broke, because selling makes the loss "real." Correction: write down, in advance, the price or fundamental condition that would trigger the sell. The pre-commitment is the discipline. The pain of the loss at the moment of sale does not go away — but the household acts on the rule it wrote earlier, not the feeling it has now.

- Recency bias — overweighting the most recent twelve to twenty-four months of returns when projecting forward. Example: A household assumes the AI-stock returns of 2024-2025 will continue indefinitely and overweights the sector to 40% of investable equity. Correction: use a 10-year base-rate horizon, not a 12-month one, for any return projection. Twelve-month projections are not analysis; they are extrapolation.

- Mental accounting (Richard Thaler's contribution from Misbehaving) — treating different "buckets" of money as having different risk rules. Example: A household receives a $10,000 year-end bonus and treats it as "play money" — invests it in a speculative position — while simultaneously underfunding the 401(k). The same dollars in the bonus and the salary, allocated by different rules, produce different outcomes for no good reason. Correction: aggregate every account onto one balance sheet, then apply one allocation framework. The label on the dollar does not change what the dollar should do.

- Confirmation bias — preferentially seeking information that supports the conclusion you already reached. Example: After deciding to buy a position, the household reads only the bullish analyst notes and dismisses bearish ones. Correction: before any meaningful position, write down the single piece of evidence that would change your mind. Then watch for that specific signal, not for the supporting signals you are predisposed to notice.

- Sunk-cost fallacy — continuing to commit resources to a losing decision because of what has already been spent. Example: A household keeps renovating a money-losing rental property because of the $80,000 already invested, rather than evaluating whether the next $80,000 would have a positive expected return. Correction: at any decision point, evaluate the next dollar in isolation. The dollars already spent are not coming back; they are not part of the analysis.

Each of these is documented in the foundational behavioral-finance literature (Behavioral Economics overview, Daniel Kahneman's Thinking, Fast and Slow, Richard Thaler's Misbehaving). The discipline is not to not have the biases — every adult planner has them too. The discipline is to put structures in place that route around the bias before it has the chance to operate.

Four worked examples

The framework and the bias glossary are useful only inasmuch as they apply to actual decisions. Four worked examples worth running through the PACED structure in practice:

1. Budgeting tradeoff: 50/30/20 vs zero-based. The 50/30/20 framework (50% needs, 30% wants, 20% savings) is a fast heuristic and is well-suited to a household that has not previously budgeted at all. The zero-based budget (every dollar gets a category before the month begins) is more demanding and is well-suited to a household whose problem is "the money disappears and we don't know where." The criteria that decide: does the household actually need visibility into where the money goes (zero-based wins), or does it primarily need a fast guardrail it can hold to (50/30/20 wins). Neither is universally better. Pick the one whose default behavior changes the actual problem the household has.

2. Debt payoff order: avalanche vs snowball. Avalanche (pay highest-rate first) is mathematically optimal. Snowball (pay smallest balance first) is behaviorally optimal for many households because it produces faster psychological wins that maintain the discipline. The criteria that decide: how durable is the household's commitment to the payoff plan. A household that will stick to the math regardless of motivation should run avalanche. A household whose history suggests it will give up partway through should run snowball — the slightly higher total interest cost is worth paying for the higher probability of completing the plan. Be honest about which household you actually are.

3. Investing allocation: lump sum vs dollar-cost averaging. The empirical evidence (from Vanguard's recurring analyses and others) favors lump-sum investing about two-thirds of the time, because markets rise more often than they fall and time-in-market beats market-timing on average. The criterion that overrides the average: the household's actual behavior. A household that will panic-sell after a 20% drawdown immediately following a lump-sum investment will produce a worse outcome than the same household that DCA'd into the position and rode the same drawdown without selling. The right answer depends on the household's behavioral risk capacity, not just the expected-return math. Discuss with your planner — the answer is genuinely household-specific.

4. Major purchase: lease vs buy vs delay. The criteria that matter for a car purchase: total cost of ownership over the expected hold period (not monthly payment in isolation), the household's time horizon for the vehicle, the after-tax cost of capital (for cash purchases) or the loan rate (for financing), and the depreciation curve of the specific vehicle. Lease usually wins when the household plans to replace the vehicle in three years and wants predictable monthly cost. Buy usually wins when the household plans to keep the vehicle six-plus years. Delay almost always wins for the household that has not run any of the above analysis. Boring, but load-bearing.

AI-era decision biases (and why a process matters more, not less)

The bias inventory above is the classical Kahneman-and-Thaler set. The 2025 academic literature has been adding new categories specifically shaped by the integration of AI tools into the household financial workflow. The cleanest summary is F1000Research's 2025 systematic review of behavioral finance literature 2020–2025, which names automation bias, algorithmic deference, and digital overconfidence as additions to the classical set. The PYMNTS reporting on AI as the new point of financial execution confirms what the academic literature is naming: AI has moved from a recommendation tool to a decision agent that, in some retail and consumer-finance settings, executes the decision before the user has time to evaluate it.

The three biases, briefly:

- Automation bias — over-trusting an algorithmic recommendation because it is algorithmic. The signal that the recommendation came from a model gets weighted as evidence of correctness, beyond what the model's actual track record warrants.

- Algorithmic deference — declining to override an algorithmic recommendation even when the user has private information the model lacks. The household sees an AI-generated allocation that does not account for a specific obligation only the household knows about, and accepts it anyway.

- Digital overconfidence — overestimating one's own decision quality because the workflow runs through a clean interface with charts and ratings. The professionalism of the UI is read as evidence of the quality of the underlying decision.

The framework above is the structural defense against all three. The criteria step explicitly forces the household to name the variables that matter for the specific decision — including the variables an algorithmic tool does not see. The evaluate step forces a written comparison that surfaces whether the AI's recommendation actually matches the household's situation. The decide step forces the trigger that would cause the household to revisit the decision — including the trigger that would override the algorithm.

For the specific question of which behavioral-finance apps' nudge architecture actually aligns with the framework above (and which apps' architecture works against it), the companion piece on behavioral finance apps maps named apps against the bias they are designed to address — and notes the apps whose mechanics, on the data, push households the wrong direction.

What to actually do this quarter

For a reader who has gotten this far and wants a concrete next step:

- Pick one upcoming household decision. Not all of them. One. The next significant money decision the household is actually going to make in the next ninety days.

- Run it through the PACED framework, in writing. Problem, alternatives, criteria, evaluate, decide. Twenty minutes, with the household member who will be co-responsible for the decision sitting at the same table. The writing is the part that matters.

- Identify the single bias most likely to operate on this specific decision. Anchoring on a list price. Loss aversion holding a position. Mental accounting on a windfall. Whichever one applies, write down the structural correction before the decision moves to the implementation step.

- Bring the written analysis to the planning conversation. Fee-only, fiduciary. The conversation is materially more productive when the household has done the PACED work first — the planner can then focus on the specific variables (tax bracket, time horizon, household obligations) that change the answer, rather than building the entire decision from scratch in the meeting.

The Schwab 2025 Modern Wealth Survey reports that 39% of Gen Z now have a written financial plan, versus 26% of boomers — and that Americans now believe it takes $839,000 to feel financially comfortable, up from $778,000 the previous year. The deciding variable in whether a household closes the planning gap is rarely income. It is process. The framework above is the cheapest, most durable version of that process I know.

None of this is individual financial advice. The right answer for any specific household depends on facts a blog post cannot see — the tax bracket, the time horizon, the household structure, the specific obligations on either side of the balance sheet. For decisions of any size, the framework is the input to the conversation with your own licensed advisor, not a replacement for it.

Frequently Asked Questions

The deliberate process of weighing alternatives against your goals, timeline, risk tolerance, and tax situation — using a repeatable framework (like PACED: Problem, Alternatives, Criteria, Evaluate, Decide) instead of reacting to the latest market or marketing pitch.

Slow the decision down, separate the trigger emotion from the choice, run the decision through a written framework, and stress-test the worst-case outcome before committing. FINRA's 2024 NFCS shows household stress is at a multi-year high — having a process matters more now than ever.

Anchoring (latching onto the first price you see), loss aversion (refusing to sell a loser, where the pain is roughly 2.25× the equivalent gain), recency bias (chasing last year's winners), confirmation bias (only reading what agrees with you), sunk-cost fallacy (throwing good money after bad), and mental accounting (treating bonus money differently from salary). 2025 research adds automation bias — over-trusting algorithmic recommendations.

It can — but only if you understand the inputs and the trade-offs. AI tools introduce their own bias (automation bias, algorithmic deference, digital overconfidence). The rational move is to use the tool as a second opinion, not a substitute for your own framework. The companion piece on behavioral finance apps maps named apps to the bias each one is built to address.

Rational decisions weigh facts, timeline, and trade-offs against your goals. Emotional decisions react to short-term feelings (fear, FOMO, regret). The goal isn't to suppress emotion — it's to notice it, slow down, and run the choice through a process before committing.

PACED stands for Problem, Alternatives, Criteria, Evaluate, Decide — a five-step decision framework taught in the St. Louis Fed's personal-finance-education resources (April 2026). Adapted for household money decisions, it adds the planner-grade variables (marginal tax rate, time horizon, after-tax return, behavioral risk, reversibility) the educational version is too general to name.

Check Out These Related Articles

The Great Depression and Personal Finance: Lessons from a Crisis

Redefining Financial Literacy through Interactive Social Media Initiatives

Financial Wisdom through the Ages: Learning from Ancient Philosophers and Modern Financial Gurus