Mastering the Art of Tax-Efficient Investing

The number worth opening with on tax-efficient investing in 2026 is not a return figure or a savings projection. It is the after-tax alpha figure that Vanguard's July 2024 research paper assigned to disciplined tax-loss harvesting paired with rebalancing: 0.45% to 0.95% per year, with a broader Advisor's Alpha range up to 1.27%, and a typical outcome near +1% in cumulative after-tax return. What that range actually measures is the cumulative return uplift from running tax mechanics deliberately rather than ignoring them. What it does not tell us is how the range maps to any specific household — the variance is wide depending on volatility, contribution cadence, account mix, and bracket.

The reason to lead with that figure is that it reframes what tax-efficient investing actually is. It is not "find the magic strategy that minimizes taxes." It is the disciplined mechanical execution of standard moves — account priority, asset location, tax-loss harvesting, account-type sequencing, withdrawal sequencing — across years and tax events, with each move sized to the specific tax environment of its year. This guide walks through the 2026 version of those mechanics. None of it is individual tax or financial advice; tax decisions belong with a CPA or licensed advisor who knows your full situation.

What changed for tax-efficient investing in 2026

Three things changed between 2024 and 2026 that rewrite parts of the standard tax-efficient investing playbook.

TCJA brackets are now permanent. The One Big Beautiful Bill Act, signed July 4, 2025, eliminated the December 31, 2025 sunset on the 2017 Tax Cuts and Jobs Act ordinary-income brackets. The 10/12/22/24/32/35/37% structure is now permanent. For Roth conversion math, this removes the "convert now while rates are low" urgency that drove much of 2023–2025 conversion activity. The brackets are no longer scheduled to revert. The case for Roth conversions still exists — RMD avoidance, surviving-spouse trap, tax diversification — but the time-pressure framing has weakened.

Mandatory Roth catch-up for high earners. Starting January 1, 2026, workers age 50 or older who earned more than $150,000 in FICA wages in 2025 must make all 401(k) and 403(b) catch-up contributions on a Roth (after-tax) basis. Pre-tax catch-up contributions are no longer permitted at this wage level. This is the single largest structural change in account-type strategy this year. Catch-up dollars that previously reduced current taxable income now arrive in a Roth bucket, taxed at the marginal rate today in exchange for tax-free withdrawals later. The implication: high earners with strong current cash flow now have meaningfully more Roth assets accumulating than they would have otherwise.

Super catch-up for ages 60-63. Workers aged 60 through 63 can contribute an enhanced $11,250 catch-up (instead of the standard $8,000), bringing their 2026 401(k) total to $35,750. The window is age-bounded — it drops back to the standard catch-up at age 64. For investors in their early 60s with significant earnings runway, this is a one-time structural opportunity to push more retirement savings into tax-advantaged wrappers.

These three changes interact. A 60-year-old earning $250,000 in 2026 must contribute their entire $11,250 super catch-up as Roth (above the $150K wage trigger). The combined effect is a meaningfully larger Roth allocation in a meaningfully shorter window than retirement-planning content from 2024 anticipated.

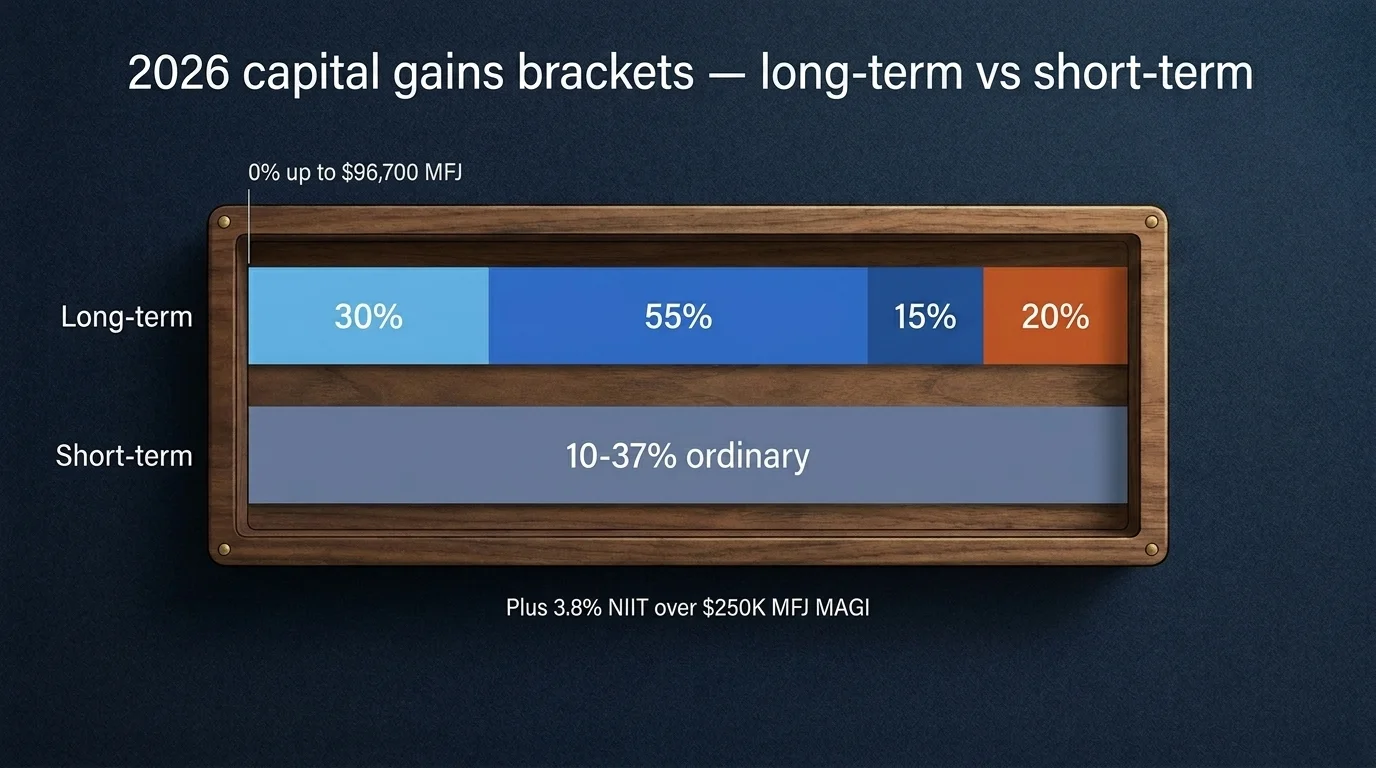

Capital gains mechanics in 2026

Most tax-efficient investing guidance is downstream of one fact: long-term capital gains and qualified dividends are taxed at lower rates than ordinary income. The 2026 rates and thresholds:

| Income range (MFJ taxable income) | Long-term capital gains rate | Short-term capital gains rate |

|---|---|---|

| Up to ~$96,700 | 0% | Ordinary (10/12%) |

| ~$96,700 to ~$600,050 | 15% | Ordinary (22-35%) |

| Above ~$600,050 | 20% | Ordinary (37%) |

- Long-term holding matters quantitatively. Selling a $50,000 gain in the 24% bracket as a short-term gain produces a $12,000 federal tax bill. The same gain held over one year and qualifying as long-term costs $7,500 at the 15% rate. The difference — $4,500 — is the cost of selling 11 months too soon.

- The 0% LTCG bracket is a planning lever. A married couple with $90,000 of taxable income in a sabbatical year, an early-retirement year, or a low-income year can realize approximately $6,700 of long-term capital gains at 0% federal tax. This is gain harvesting — the inverse of loss harvesting — and it is almost completely absent from mainstream tax-efficient investing guidance.

The 3.8% Net Investment Income Tax (NIIT) sits on top of the long-term capital gains rate for households above $200,000 MAGI single or $250,000 MFJ. These thresholds have not been indexed for inflation since 2013, which means more dual-income households cross them every year. The effective top federal LTCG rate is therefore 23.8% (20% + 3.8% NIIT) for high earners, not 20%.

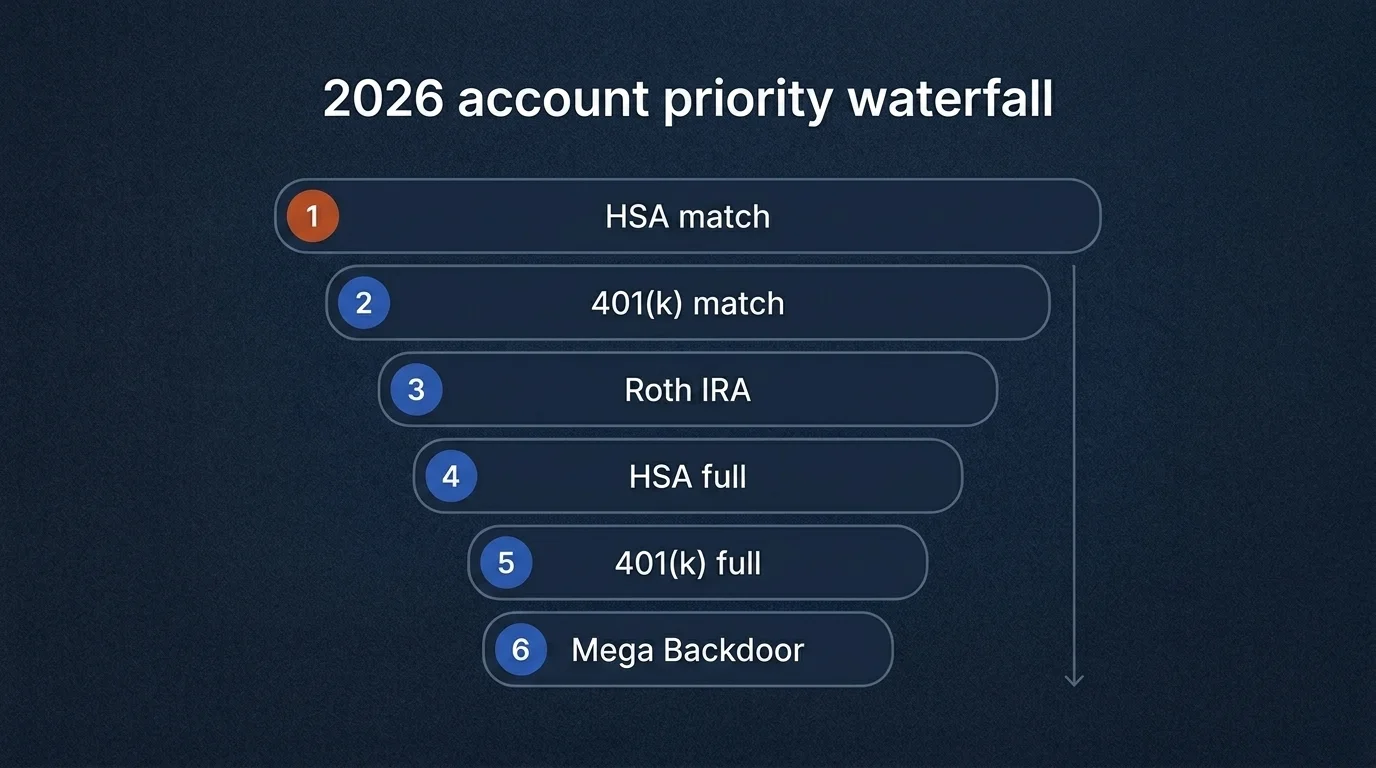

The account priority waterfall

The order in which an investor funds different account types matters more than the specific allocation inside each. The 2026 account priority waterfall, with reasoning:

- HSA up to any employer contribution. The HSA's triple tax advantage (deductible going in, tax-free growth, tax-free out for qualified medical) is the only such wrapper in the U.S. tax code. If an employer puts dollars in your HSA, take them.

- 401(k) up to the employer match. The match is a 50–100% immediate return; nothing else competes. 2026 limit is $24,500 + $8,000 standard catch-up + $11,250 super catch-up for ages 60–63; start with whatever percentage captures the full match.

- Roth IRA or Backdoor Roth. 2026 limits are $7,500 + $1,100 catch-up at 50+, with phase-outs at $153,000–$168,000 single MAGI and $242,000–$252,000 MFJ MAGI. Above the phase-out, the backdoor Roth (non-deductible IRA contribution + immediate conversion) remains the workaround.

- HSA full-year contribution. 2026 HSA limits are $4,400 self-only and $8,750 family, plus a $1,000 catch-up at 55+. Treat the HSA as a stealth retirement account: pay current medical expenses out of pocket if cash flow allows, let the HSA compound.

- 401(k) full year. The remaining elective deferral. Consider Roth vs traditional based on current vs expected retirement marginal bracket. (For high earners with FICA wages over $150K, all catch-up dollars must be Roth in 2026.)

- Mega Backdoor Roth (if your plan allows) or taxable brokerage. Mega backdoor allows after-tax 401(k) contributions converted to Roth, dramatically expanding the Roth bucket — but only if your plan offers in-service withdrawals or after-tax contributions with auto-conversion. Otherwise, taxable brokerage with attention to asset location.

The waterfall is a starting framework. Individual circumstances — high deductible health plan eligibility, plan-level constraints, marginal bracket shape — modify the order. The decision belongs in a CPA or fiduciary planner's hands, not a blog post's.

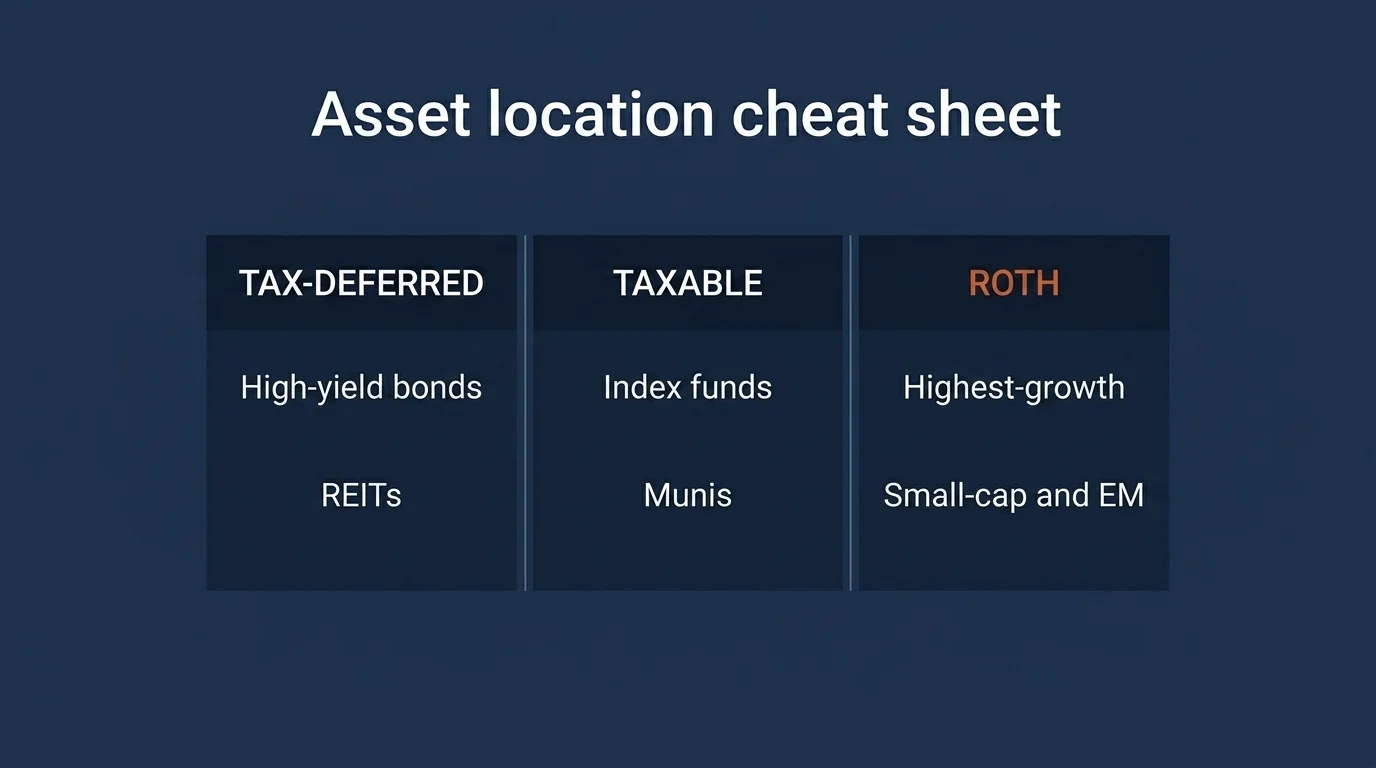

Asset location: the textbook tax efficiency lever

Asset location is the practice of holding different asset classes in different account types based on their tax characteristics. Most retail tax-efficient investing content gestures at this without naming the term, which is unfortunate because the gains compound meaningfully over decades.

The textbook framework, simplified:

| Tax-deferred (Traditional 401(k)/IRA) | Taxable brokerage | Roth (IRA/401(k)) |

|---|---|---|

| High-yield bonds | Broad-market stock index funds | Highest-conviction growth holdings |

| TIPS | Tax-managed equity funds | Small-cap and emerging markets |

| REITs (high ordinary-income distributions) | Municipal bonds | Volatile holdings with long horizons |

| Actively-managed mutual funds with high turnover | Individual stocks held >1 yr | Anything you expect to grow significantly |

The reasoning is mechanical:

- Tax-deferred wrappers convert ordinary-income distributions into deferred-gain treatment. A bond fund or REIT inside an IRA produces no current-year tax. The same fund inside a taxable account produces ordinary-income tax annually on every distribution.

- Taxable wrappers benefit from the long-term capital gains rate. Holding broad-market index funds for years allows realized gains to qualify at the 15% or 20% LTCG rate rather than ordinary income. Municipal bonds in taxable accounts produce federally tax-exempt interest, which is its own asymmetric advantage for high-bracket filers.

- Roth wrappers maximize tax-free growth. Anything held in Roth grows tax-free indefinitely and exits tax-free. The highest-expected-return assets belong here because the wrapper rewards growth most.

The size of the asset-location effect is debated empirically. Vanguard research has historically estimated the long-run benefit at 0.20% to 0.50% of annual after-tax return for portfolios where it is implementable. That is not enormous in a single year. Compounded over 30 years on a $1 million portfolio, it is meaningfully larger than a single year's tax bill.

Tax-loss harvesting: the integrated practice with rebalancing

Tax-loss harvesting (TLH) is the deliberate sale of an investment at a loss to realize the loss for tax purposes. The realized loss can offset realized gains elsewhere (reducing capital gains tax) and, up to $3,000 per year on individual returns, offset ordinary income, with any unused losses carried forward indefinitely.

The 2025–2026 framing across institutional research is that TLH and rebalancing operate as one practice, not two. When a portfolio drifts because some holdings ran ahead while others fell, the rebalance trade naturally produces realized gains and realized losses simultaneously. Pair them. The harvested loss offsets the realized gain, the net tax cost approaches zero, and the portfolio returns to target allocation. Vanguard's research puts the after-tax alpha from this disciplined approach at 0.45% to 0.95% per year, with a broader Advisor's Alpha range up to 1.27%.

A worked example: a $50,000 broad-market ETF position purchased in 2024 has fallen 15%, sitting at $42,500. Selling realizes a $7,500 long-term loss. At the 24% federal bracket plus 3.8% NIIT, the tax benefit is $7,500 × 27.8% = $2,085, plus $3,000 of the loss can offset ordinary income that year for an additional $720 federal benefit. Net tax savings: roughly $2,800 from a single TLH trade.

The mechanic that requires care is the IRS wash-sale rule: if you sell a security at a loss and buy the same or "substantially identical" security within 30 days before or after the sale (a 61-day window total), the loss is disallowed for current-year tax purposes. The disallowed loss is added to the basis of the replacement security, which means it is not lost forever — only deferred until that replacement is sold.

The 2026 clarification most retail investors miss: the wash-sale rule applies across all accounts under the taxpayer's control, including IRAs and Roth IRAs. Selling at a loss in your taxable account and rebuying the same security in your IRA does NOT avoid the wash sale — it permanently disallows the loss because there is no basis adjustment in the IRA. This is the most-missed trap in DIY harvesting.

The standard workaround is to replace the harvested fund with a similar-but-not-identical fund. Common pairs that are economically similar without being "substantially identical" under IRS standards:

- VTI ↔ ITOT ↔ SCHB (broad U.S. equity)

- VOO ↔ IVV ↔ SPLG (S&P 500)

- BND ↔ AGG (broad U.S. bond)

- VEA ↔ IDEV (developed international)

These are illustrative; the specific funds and tax treatment of any particular substitution belong in a tax professional's hands.

Roth conversions in 2026

A Roth conversion is the deliberate transfer of pre-tax (Traditional) IRA or 401(k) dollars into a Roth IRA, paying ordinary income tax on the converted amount in the year of conversion in exchange for tax-free growth and withdrawals afterward.

The bracket-fill approach: convert in years where your taxable income is low (the gap between leaving a job and starting Social Security; sabbaticals; early retirement years) up to the top of a target bracket without spilling into the next. A 58-year-old in the 12% federal bracket who expects to land in the 22% bracket after RMDs at 73 can convert each year up to the top of the 12% bracket — paying 12% today to avoid 22% later — and meaningfully reduce their RMDs by 73 because the traditional balance has been partially drained.

The IRMAA constraint matters in the years approaching age 63 (because Medicare uses the prior-year MAGI as the lookback). The 2026 IRMAA threshold is $109,000 MAGI for single filers and $218,000 for MFJ. A conversion that pushes MAGI above the threshold triggers Medicare Part B and Part D surcharges that can cost $1,000–$5,000 per year for one to two years. The right conversion size in a given year is the largest conversion that stays under both your target marginal rate ceiling AND the IRMAA threshold.

For a 45-year-old in the 32% bracket, conversions are typically NOT favorable — paying 32% today to potentially save 24% later is locking in a higher rate. The honest framing: Roth conversions are a bracket-arbitrage tool. They work when current marginal rate is meaningfully lower than projected retirement marginal rate. They do not work universally.

Direct indexing: the next layer of tax-loss harvesting

Direct indexing means owning the underlying individual stocks of an index in a separately managed account (SMA), instead of owning a single ETF or mutual fund wrapper. The mechanical advantage for tax-efficient investing: with hundreds of individual positions, you can harvest losses on the specific stocks that fall in any given period — even when the index itself is flat or up. ETF-level harvesting cannot surface those individual losses because the wrapper averages them out.

Vanguard, Fidelity, and Schwab now offer direct indexing products with minimums down to $5,000 (Fidelity FidFolios) and $100,000 (Vanguard Personalized Indexing). Long/short tax-aware variants pioneered by AQR, Quantinno, and others are emerging at the high-net-worth tier.

The decision matrix for whether direct indexing is worth the fee:

- Account size: typically $250,000+ in taxable assets. Below that level, the fee burden often exceeds the marginal harvesting benefit over basic ETF-level TLH.

- Marginal bracket: 24%+ federal. Lower brackets see less dollar benefit from harvested losses.

- Time horizon: 5+ years. Direct indexing's benefits compound over time as harvested losses accumulate.

- Existing TLH effort: investors who already run robo-advisor or manual TLH on broad ETFs see a smaller incremental benefit. Investors who would otherwise skip TLH entirely see a large incremental benefit.

The honest framing: direct indexing is genuinely useful for the right account. It is not a universal upgrade. The Vanguard 0.45–0.95% TLH alpha figure is for ETF-level harvesting. Direct indexing can extend that range modestly higher in the right circumstances, at the cost of additional fees that need to be netted out before the comparison is fair.

QSBS / Section 1202: the founder and early-employee opportunity

Qualified Small Business Stock under Section 1202 of the Internal Revenue Code provides a meaningful exclusion from federal capital gains tax for investors who hold qualifying C-corporation stock for at least five years.

The mechanics:

- The company must be a C-corporation at the time the stock is issued, not an LLC or S-corp.

- The company's gross assets must be under $50 million at the time of issuance.

- The investor must hold the stock for at least five years before sale.

- The exclusion is the greater of $10 million OR 10x the basis in the stock at issuance.

- The company must be in an active trade or business, not a service business (law, accounting, consulting), banking, financing, or hospitality.

The relevance is concentrated. QSBS is most valuable to founders, early employees, and angel investors in venture-backed C-corp startups. It is rarely relevant for traditional public-market investors. But for the subset of TycoonTrail readers in or adjacent to startup equity, the dollars are meaningful — a $5 million capital gain on qualifying QSBS is fully excluded from federal capital gains tax.

The 5-year clock and the C-corp requirement are the most-missed disqualifiers. Stock issued by an LLC that later converted to a C-corp typically does not qualify for the period before the conversion. Stock acquired through an exercise of options that occurred before the company was a C-corp typically does not qualify. The structure has to be right at issuance.

If you hold equity in a private company and think QSBS may apply, the conversation belongs with a tax attorney before you sell anything. The structuring choices made years before the sale determine whether the exclusion is available.

Withdrawal sequencing in retirement

The flip side of accumulation-phase tax-efficient investing is decumulation-phase withdrawal sequencing. The wrong order of withdrawals can cost meaningfully more in lifetime taxes than the wrong asset location.

The traditional textbook ordering — taxable first, then tax-deferred, then Roth — minimizes early-retirement tax liability but often produces a tax spike in the RMD years (age 73 or 75) when the tax-deferred balances have grown unchecked.

The proportional-draw alternative — pulling roughly evenly from all three buckets each year — keeps marginal brackets stable across retirement and produces lower lifetime tax under most projections.

The Roth-conversion-laddered approach — using the early retirement decade (before Social Security and RMDs) to convert tax-deferred dollars to Roth at the lowest marginal rates available — captures the best of both: lower early-retirement taxable income (good for ACA subsidies if applicable) and substantially smaller traditional balances by RMD age.

The right sequencing depends on your full balance-sheet picture, your tax bracket trajectory, and your specific goals (legacy, charitable giving, longevity-protection). Specialized retirement-planning software runs the projections; a CFP or CPA familiar with retirement income planning interprets them.

What this guide does not tell you

In keeping with my own rule about disclosing the limits of any analysis:

- Whether to make any specific tax-driven decision today. That belongs with a CPA or licensed tax professional who knows your full tax situation, including state income tax and any unusual items (NIIT exposure, AMT, K-1 income, large carryforwards).

- Whether tax law will continue to look like 2026. It will not, in every detail. The TCJA brackets are now permanent under OBBBA, but specific provisions (NIIT thresholds, contribution limits indexed to inflation, IRMAA brackets, capital gains brackets) shift annually or by legislation. The mechanics described above are 2026-specific. Re-run the math when the year changes.

- Whether crypto-specific tax mechanics will hold. Crypto is currently classified as property and is not subject to the wash-sale rule under Section 1091. Multiple legislative proposals over 2024–2026 have sought to extend Section 1091 to digital assets. If that change passes, the tax-loss-harvesting playbook for crypto changes materially.

- The state tax dimension. Federal-level analysis is one layer. State income tax stacks on top, and many strategies that work cleanly federally have second-order state effects that vary by state. Multi-state filers face additional complexity that this guide does not cover.

What would change my view on the framework above: a meaningful change to the wash-sale rule's mechanics, the elimination of the indefinite carry-forward of capital losses, the removal of the long-term/short-term capital-gains distinction, or the loss of the QSBS Section 1202 exclusion. None of these are on the legislative docket as of mid-2026. None has been seriously proposed. But tax-policy regimes change, and a discipline that depends on a specific tax treatment is one whose math has to be re-run when the treatment changes.

That is tax-efficient investing in 2026 as I would walk through it for an analyst on day one. None of it is individual tax or financial advice. All of it is starting material for the conversations with the licensed professionals who can translate the framework into a plan for your specific facts.

Frequently Asked Questions

The 2026 401(k) elective deferral limit is $24,500 with a standard age-50 catch-up of $8,000. Workers ages 60-63 get an enhanced 'super catch-up' of $11,250 under SECURE 2.0. IRA and Roth IRA limits are $7,500 with a $1,100 catch-up at age 50 or older. HSAs are $4,400 self-only and $8,750 family with a $1,000 catch-up at 55+.

For investors in the 22%+ federal bracket with at least $25,000 in a taxable account, yes. Vanguard's July 2024 research puts the long-run boost at 0.45% to 0.95% of annual after-tax return, with a broader Advisor's Alpha range up to 1.27%. On a $200,000 taxable portfolio, that's $900-$1,900 a year, plus the $3,000 ordinary-income offset and indefinite carryforward of unused losses.

If you sell a security at a loss and buy a 'substantially identical' security within 30 days before or after the sale (a 61-day window total), the IRS disallows the current-year loss. Avoid it by buying a similar-but-distinct fund: sell VTI, buy ITOT or SCHB. The IRS applies the rule across all your accounts including IRAs and Roth IRAs.

As a default, hold high-yield bonds, TIPS, and REITs in tax-deferred accounts (IRA/401(k)) because their distributions are taxed as ordinary income. Hold tax-efficient stock index funds and municipal bonds in taxable accounts, where long-term capital gains rates apply and muni interest is federally tax-exempt. Hold your highest-conviction growth holdings in Roth, where future appreciation is tax-free.

For most 24% bracket filers, splitting contributions roughly 50/50 between pretax and Roth is reasonable — it preserves bracket flexibility in retirement. But if you earn $150,000 or more in FICA wages, your 2026 catch-up contributions MUST be Roth under SECURE 2.0; pretax catch-up is no longer an option for that segment.

Direct indexing means you own the individual stocks that make up an index inside a separately managed account, instead of owning a single ETF or mutual fund wrapper. The advantage: when one stock falls while the index is flat or up, you can harvest that individual loss. It typically pays for itself at $250,000+ in taxable assets and a 24%+ federal bracket. Providers include Fidelity FidFolios ($5K min), Vanguard Personalized Indexing ($100K min), and Schwab Personalized Indexing.

Qualified Small Business Stock is C-corporation stock issued by a company with under $50 million in assets at issuance and held for at least five years. Qualifying gains are excluded from federal capital gains tax up to the greater of $10 million or 10x basis. Most relevant for founders, early employees, and angel investors. The 5-year clock and C-corp status are the most-missed disqualifiers.

Long-term capital gains (assets held over one year) are taxed at 0%, 15%, or 20% depending on taxable income. A married couple filing jointly stays in the 0% bracket up to about $96,700 of taxable income. Short-term gains (held one year or less) are taxed as ordinary income, up to 37% federal. High-income investors also pay an additional 3.8% Net Investment Income Tax above $200,000 single MAGI or $250,000 MFJ MAGI.

Check Out These Related Articles

Finance Mentor vs Sponsor: What Actually Compounds a Career

Youth-Led Financial Revolutions: Crowdsourcing as a Catalyst for Investment Innovation

Red vs. Blue: The Battle of Colors in Investment Marketing