Retirement Planning 101: Securing Your Financial Future

The question I hear most often from clients in 2026 is some version of: "I'm in my late fifties, I want to know if my retirement plan still works under the new rules — and what I should be doing differently this year." The honest answer is that it depends on four things you can name and ten you cannot, and most of the retirement planning strategies that actually work start with figuring out which is which. This guide is a serious 2026 walkthrough of the questions a real household actually asks: how much you need, what changed under SECURE 2.0, how the account types compare, when to claim Social Security, how to get to retirement before 59½ if you want to, and what healthcare and long-term care actually cost.

None of what follows is individual financial advice. Individual circumstances belong to a licensed planner who knows your full balance sheet, your tax situation, your health history, and your family circumstances. What I can give you is the framework — the same framework I walk through with clients across the desk — and the 2026 numbers you need to make the framework operational.

The 2026 retirement rulebook

The contribution limits, age thresholds, and policy parameters that drive every retirement decision changed enough between 2024 and 2026 that an article written before this calendar is materially out of date. Save these numbers; they are the inputs to every other decision below.

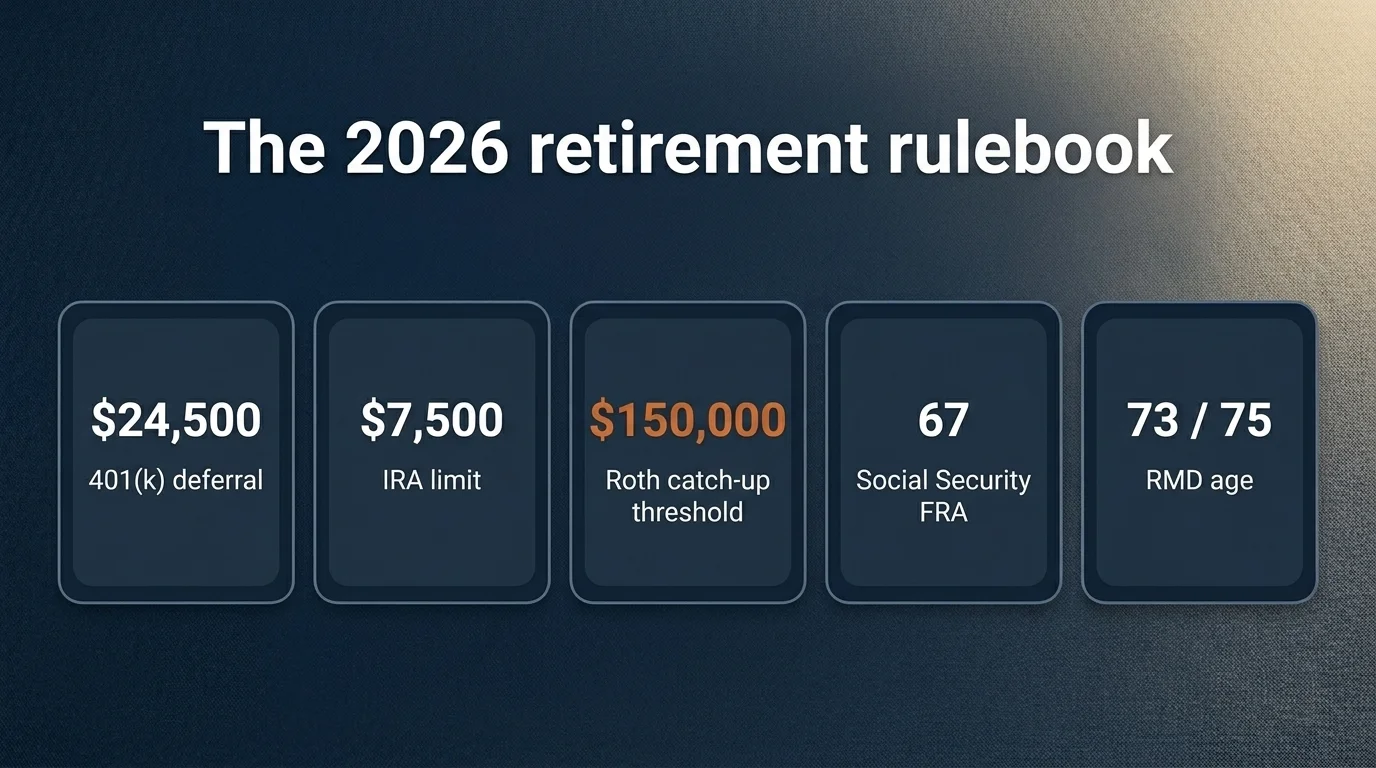

For 2026, the IRS has set the 401(k) employee deferral limit at $24,500, up from $23,500 in 2025. Workers age 50 or older can add the standard $8,000 catch-up for a $32,500 total. Workers aged 60 through 63 qualify for an enhanced "super catch-up" of $11,250 instead of the standard $8,000, lifting the total to $35,750. The IRA contribution limit is $7,500 for those under 50; $8,600 for those 50 and older.

Social Security's full retirement age finalized at 67 in November 2026 for everyone born in 1960 or later — the culmination of the 1983 amendments' phased increase. The 2026 cost-of-living adjustment is 2.8%, adding roughly $56 per month to the average retirement check.

Required Minimum Distributions are now tiered by birth year. If you were born between 1951 and 1959, your RMDs begin at age 73. If you were born in 1960 or later, your RMDs begin at age 75. The old "age 72" rule no longer applies to anyone reading this in 2026 for the first time.

The 2026 IRMAA thresholds — the income levels above which Medicare Part B and Part D surcharges kick in — are $109,000 single MAGI and $218,000 married-filing-jointly MAGI. I will come back to these in the Roth conversion ladder section because they are the constraint that shapes the conversion math.

The PLESA — pension-linked emergency savings account inside a 401(k) — caps at $2,600 for 2026, with the first four withdrawals per year tax- and penalty-free. It exists for the "I cannot lock everything in retirement accounts" objection.

These are the inputs. Now the planning.

How much do you actually need to retire?

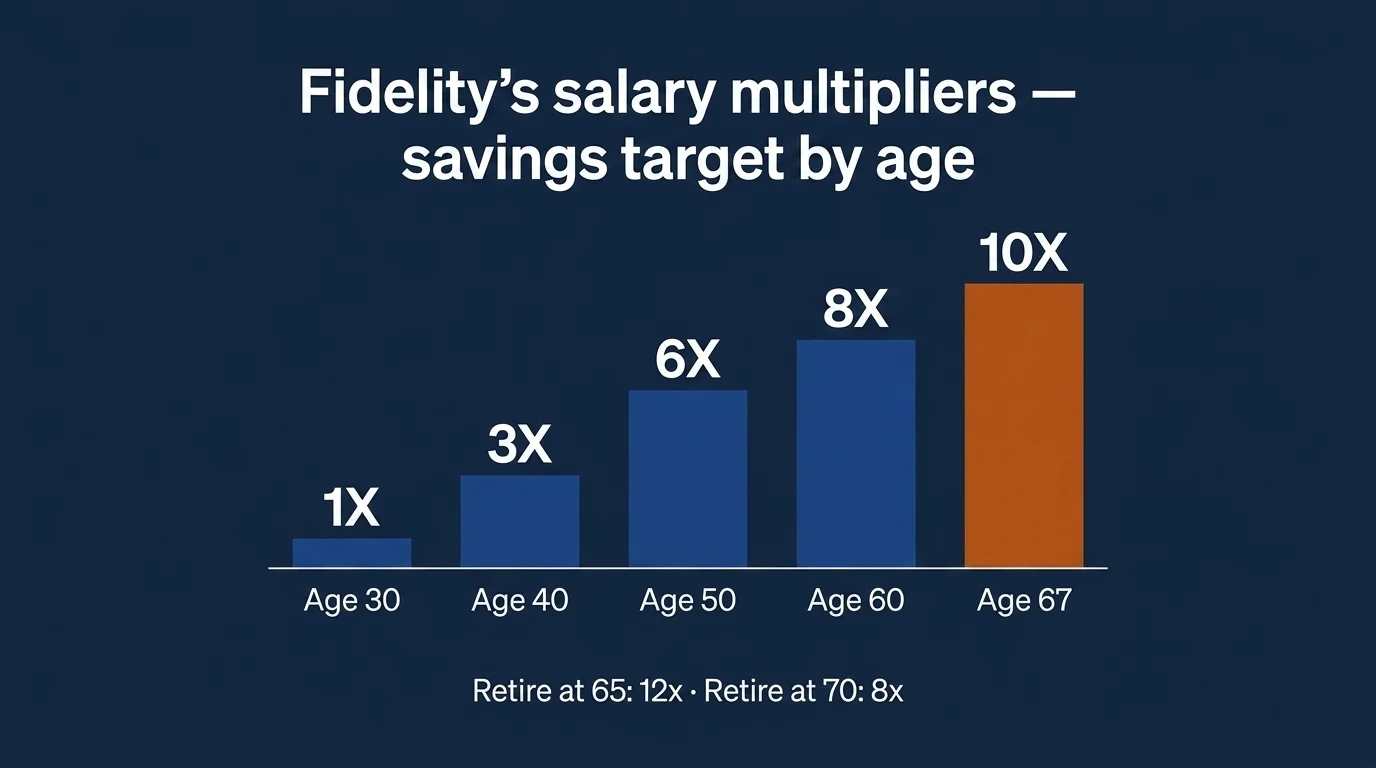

The honest answer is that the right number for you depends on your spending, not on a multiplier — but multipliers are useful as a sanity check. The most cited benchmark in U.S. retirement planning, Fidelity's salary multipliers, suggests a target of 1× your salary saved by age 30, 3× by 40, 6× by 50, 8× by 60, and 10× by age 67.

Those numbers assume retirement at full retirement age. The multiplier shifts with the retirement-age decision: retire at 65 and you should target 12×; retire at 67 and 10×; wait to 70 and 8× is sufficient. The reason is mechanical — every additional year of work is one fewer year your portfolio has to support, plus an additional year of Social Security delayed-retirement credits.

The other half of the calculation is the safe withdrawal rate. The 4% rule — Bengen's original 1994 finding that a 4% initial withdrawal from a balanced portfolio survived every historical 30-year window — is the number most retirement articles still cite. Bengen himself updated his framework in 2025: the historical worst-case rate is closer to 4.7%, with most retirement-start years supporting 5.25% to 5.5% safely. Bengen's framing in his December 2025 CNBC interview is that early retirees following the strict 4% rule may be "cheating themselves" out of usable retirement income.

A worked example with round numbers, the way I'd walk a client through it across the desk:

A household plans to retire at 67 with $1,000,000 saved. At Bengen's updated 4.7% SAFEMAX, that supports approximately $47,000 per year in inflation-adjusted withdrawals — for life — at the historical worst-case starting point. Add the household's combined Social Security benefit (let's assume $36,000/year combined, claimed at FRA), and the gross retirement income is about $83,000 per year before taxes.

Whether $83,000 is enough is the question only the household can answer, by comparing it to their projected spending. If their preferred retirement lifestyle costs $90,000 a year, they have a gap and need either more savings, lower spending, a later retirement date, or a larger Social Security claim through delay. If it costs $65,000, they have margin and can afford the 5.25% withdrawal rate Bengen described as reasonable.

The four numbers that drive whether a retirement plan works:

- Your annual spending estimate, in retirement, in today's dollars. Most households underestimate this by 10-20% because they forget healthcare, taxes, and house repairs.

- Your accumulated savings across all accounts (401(k), IRA, Roth IRA, taxable brokerage, HSA).

- Your expected combined Social Security at the claiming age you choose.

- Your longevity assumption. Default to age 95 unless you have a reason to use a different number — the cost of a too-early longevity assumption is running out of money; the cost of a too-late one is dying with assets you could have spent.

Notice what is not on that list: market returns next year. The market return over the next twelve months has materially less impact on whether your retirement works than whether you correctly named those four numbers. Boring, but load-bearing.

SECURE 2.0 in 2026: what changed

The SECURE 2.0 Act, signed in late 2022, has provisions that phase in through 2033. Several of the most consequential ones become operative in 2026, and they change the planning calculus for nearly every household I work with.

The Roth catch-up rule for high earners. Starting January 1, 2026, workers age 50 or older who earned more than $150,000 in FICA wages in 2025 must make all 401(k) and 403(b) catch-up contributions on a Roth (after-tax) basis. Pre-tax catch-up contributions are no longer permitted at this wage level. If your employer's plan does not offer a Roth option, you lose the ability to make catch-up contributions entirely. The wage threshold is inflation-indexed from the statutory $145,000 base.

For a 58-year-old in the 32% federal bracket who has been making pre-tax catch-up contributions for years to reduce current-year taxable income, this is a meaningful change. The Roth catch-up costs you the deduction today in exchange for tax-free growth and withdrawals later. Whether that trade is worth it depends on your projected retirement bracket — the same Roth conversion math I'll walk through in the next section.

Roth employer match. Per SECURE 2.0, employers can now offer matching contributions as Roth (employee elects). If your employer offers this and your plan permits, you can choose to receive matching contributions into your Roth 401(k) — paying tax on the match in the current year in exchange for tax-free retirement withdrawals. For workers anticipating a higher bracket in retirement than today (less common but real for some early-career savers), this is a new tax-diversification lever.

529-to-Roth IRA rollover. Starting in 2024 and continuing under refined 2026 rules, 529 plans that have been open for 15 or more years can roll unused balances tax- and penalty-free into a Roth IRA, up to a $35,000 lifetime cap per beneficiary. For families with leftover education savings, this converts a stranded asset into retirement capital for the beneficiary. Subject to annual Roth contribution limits and earned-income requirements.

The 10-year inherited IRA rule, fully enforced. For non-spouse beneficiaries of IRA holders who died after 2019, the inherited IRA must be drained within 10 years. The IRS finalized the RMD rules in 2024 after years of guidance confusion, and the rule is fully operative now. For families inheriting IRA wealth, this changes the tax-planning timing materially — the old "stretch IRA" strategy no longer works for non-spouses.

RMD age tiering. Already covered above, but worth reinforcing: the old age-72 rule is dead. Born 1951-59, RMDs at 73. Born 1960 or later, RMDs at 75. The two-year window pushes the question of when to start drawing down tax-deferred accounts further into retirement, which interacts with everything else.

These are not abstract policy changes. They alter the optimal withdrawal sequencing, the right amount to convert from traditional to Roth in any given year, and the case for or against pre-tax catch-up contributions for households over the wage threshold. Anyone whose retirement plan was last updated before 2024 has a plan that is partially out of date.

401(k) vs IRA vs Roth IRA vs HSA — when each wins

The four primary retirement-savings wrappers each have distinct mechanics. The most common mistake I see at intake meetings is using the wrong wrapper for the wrong purpose — usually because someone read advice optimized for a different household.

| Wrapper | Contribution treatment | Growth | Withdrawal treatment | RMDs | Best for |

|---|---|---|---|---|---|

| Traditional 401(k)/IRA | Pre-tax deduction | Tax-deferred | Ordinary income at withdrawal | Yes (age 73 or 75) | Higher current bracket than expected retirement bracket |

| Roth 401(k)/IRA | After-tax (no deduction) | Tax-free | Tax-free | None for Roth IRA; 401(k) yes (was modified by SECURE 2.0 — none for Roth 401(k) starting 2024) | Lower current bracket than expected retirement bracket |

| HSA (paired with HDHP) | Pre-tax deduction | Tax-free | Tax-free for medical; ordinary income (no penalty) for non-medical post-65 | None during life | Workers eligible for high-deductible health plans |

| Taxable brokerage | After-tax (no deduction) | Mixed (qualified div + LTCG taxed; STCG ordinary) | Capital gains rate (or ordinary if short-term) | None | Bridge funds before 59½, flexibility, no contribution cap |

The HSA is the most underused vehicle in U.S. retirement planning. It is the only account in the U.S. tax code with a triple tax advantage — tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. After age 65, non-medical HSA withdrawals are taxed as ordinary income (no penalty), which makes the HSA functionally identical to a traditional IRA for non-medical retirement spending — but with a separate contribution lane that doesn't compete with your IRA limit. If you are eligible (covered by a high-deductible health plan, no other disqualifying coverage), funding the HSA before maxing other after-tax savings is usually the right move.

The decision tree I use with clients, simplified:

- Capture every dollar of employer match in your 401(k). The match is a 50-100% immediate return; nothing else competes with that.

- If eligible for an HSA, fund it next.

- Beyond the match and HSA, choose between traditional 401(k) and Roth based on your current vs expected retirement bracket. Higher now → traditional. Lower now → Roth. Roughly equal → split.

- Once 401(k) limits are saturated, fund an IRA (Roth if income permits, backdoor Roth if not).

- Beyond all tax-advantaged wrappers, taxable brokerage for additional savings — with attention to asset location (tax-efficient investments in taxable, tax-inefficient in tax-advantaged).

The wrapper question is not the same as the asset question. You can hold the same diversified mix of equity and fixed income across all five wrappers; the wrappers determine who pays tax on what, when, and at what rate.

The Roth conversion ladder

This is the section where the FIRE community has been ahead of mainstream retirement guidance for a decade, and it is worth walking through carefully because the math actually works for far more households than the early-retirement crowd.

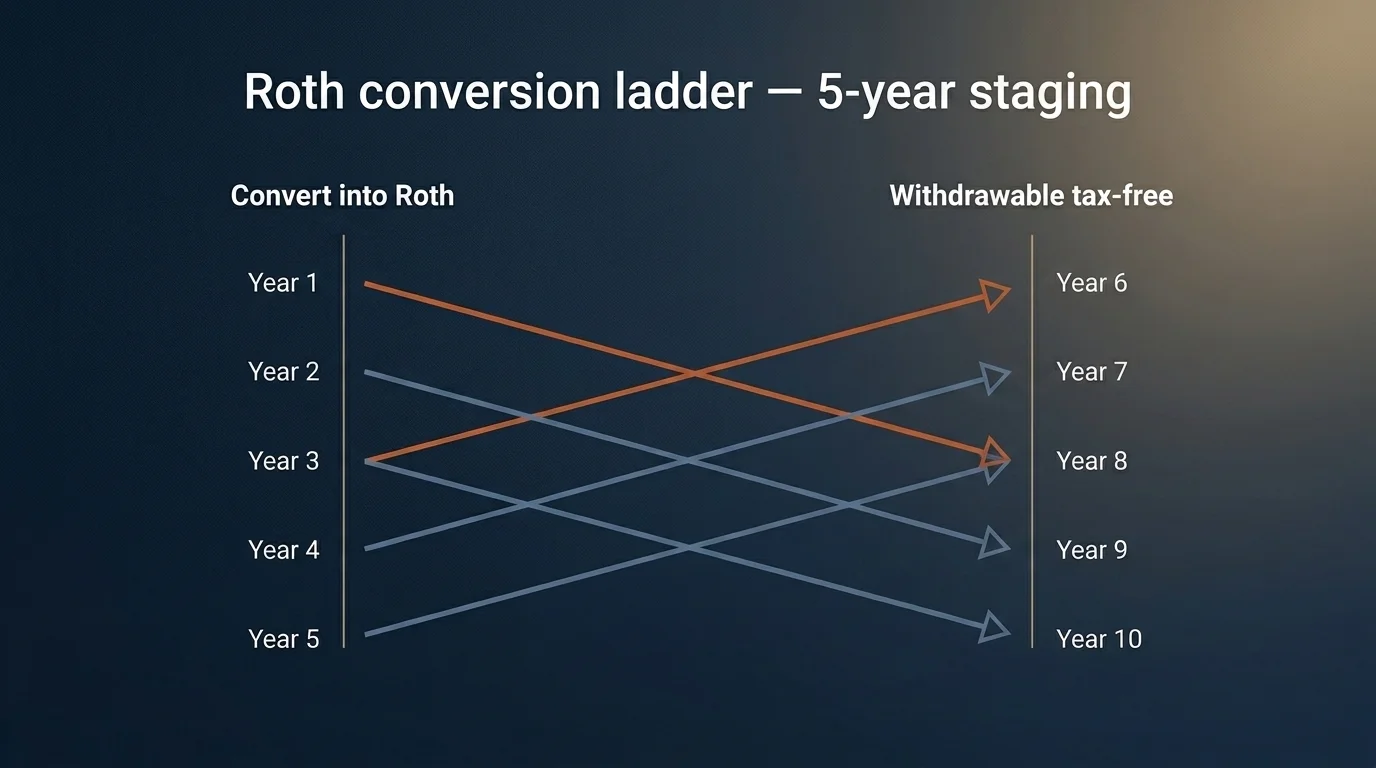

A Roth conversion ladder is a multi-year strategy of converting portions of a traditional IRA or 401(k) into a Roth IRA, paying ordinary income tax on each conversion, then waiting five calendar years for each conversion to "season" before withdrawing it tax-free and penalty-free — even if you are under age 59½.

The two structural reasons it works:

- Conversion timing. You convert in low-income years (e.g., the years between leaving a job and claiming Social Security, when your taxable income is low) at low marginal rates, and pull the money out years later when you would otherwise be facing higher rates from RMDs and Social Security stacked together.

- The 5-year clock per conversion. Each conversion has its own 5-year clock. Year 1 convert, year 6 withdraw. Year 2 convert, year 7 withdraw. Stack them and you build a tax-free income stream that becomes withdrawable at 59½ minus 5 = age 54.5 if you started early enough.

A worked example for a 58-year-old in the 12% federal bracket expecting to land in the 22% bracket after age 73 because of RMDs and Social Security: a partial conversion of, say, $50,000 each year through age 72 (filling up the 12% bracket without triggering 22% on the converted amount) is frequently sensible. By the time RMDs begin at 73, much of the traditional balance has been converted at 12%, the Roth has been growing tax-free, and the RMDs are smaller because the traditional balance is smaller.

The constraint that matters most in 2026 is the IRMAA threshold. The 2026 single-filer threshold is $109,000 MAGI; married filing jointly is $218,000. Converting too aggressively pushes Modified Adjusted Gross Income above these levels and triggers Medicare Part B and Part D surcharges that can cost $1,000-$5,000 per year depending on the bracket. The right conversion size in a given year is the largest conversion that stays under both your target marginal-rate ceiling AND the IRMAA threshold.

A planner runs these numbers using projection software. A motivated DIY-er can run them in a spreadsheet. The work is not exotic — it is filling in current taxable income, your projected post-RMD taxable income, the IRMAA threshold for your filing status, and finding the conversion size that makes the math come out best. What you should NOT do is wing it without running the numbers, because a single year's conversion mistake can cost you tens of thousands of dollars in unnecessary current-year tax or future-year IRMAA surcharge.

For a 45-year-old in the 32% bracket, a conversion ladder is frequently NOT sensible — converting at 32% to save 24% later is paying current tax to lock in a higher rate. The honest version: conversion ladders are bracket-arbitrage tools, not universal advice. They work for people whose current marginal rate is meaningfully lower than their projected retirement rate.

How to retire before 59½: Rule of 55, SEPP, the ladder, and brokerage bridges

The "is there any way to access my retirement money before 59½ without the 10% penalty" question is among the most frequent I get from clients in their early-to-mid fifties. The answer is yes — there are at least four ways, each with different mechanics and different best-for profiles.

- The Rule of 55. If you leave your employer in or after the calendar year you turn 55, you can take penalty-free withdrawals from THAT specific employer's 401(k) — but only that plan, not from IRAs and not from prior employers' 401(k)s. Income tax still applies. Public safety employees qualify at 50. The most common implementation: leave your job at 55-58, leave the 401(k) in place at the employer (don't roll to IRA, which would forfeit Rule-of-55 access), withdraw what you need from age 55 until you reach 59½ when other accounts open up.

- Substantially Equal Periodic Payments (SEPP / 72(t)). A series of equal annual withdrawals from an IRA, calculated by IRS-approved methods, that must continue for the longer of 5 years or until age 59½. Penalty-free if the rules are followed exactly; the penalty (plus retroactive interest) applies if you modify the schedule. Useful when the Rule of 55 is unavailable. Operationally rigid — the withdrawal amount cannot be changed without disqualifying the entire plan.

- The Roth conversion ladder (covered above). Five-year staged conversions provide tax-free withdrawable income from age (current age + 5) onward.

- A taxable brokerage bridge. Hold enough in a regular taxable brokerage account to cover spending from your retirement date until 59½. No penalty (it's not a retirement account), capital gains rates apply, full liquidity. The cost is forgoing the tax-advantaged wrapper for that capital.

These are not mutually exclusive. A common structure I see in early retirement plans is: brokerage bridge for the first 1-3 years, Rule of 55 from age 55 through 58, Roth ladder withdrawals starting at age 60 (assuming conversions began at 55), then 59½ unlocks IRAs and 401(k) anyway. The right combination depends on your specific situation, and it is one of the parts of retirement planning where running the projections matters most.

Social Security: 62 vs 67 vs 70

The Social Security claiming decision is among the most analyzed and least followed in U.S. retirement planning. The math is widely understood; the behavior is dominated by anxiety about Social Security's solvency, household cash flow needs, and a strong human bias toward "take what I can get now."

The mechanics:

- Claim at 62 (the earliest age for retirement benefits). Your monthly benefit is reduced by approximately 30% versus claiming at full retirement age. The reduction is permanent.

- Claim at FRA — now 67 for everyone born in 1960 or later, finalized November 2026. You receive 100% of your "primary insurance amount."

- Claim at 70. You receive approximately 124% of your primary insurance amount, thanks to delayed retirement credits of approximately 8% per year for each year of delay between FRA and 70. After 70, the credits stop accruing.

The break-even age for "claim at 62 vs FRA" sits in the late 70s for most people; for "claim at FRA vs 70" the break-even is generally around age 81-82. If you live past the break-even, claiming later wins; if you die before, claiming earlier wins. Median U.S. life expectancy at age 65 is around 84 for women and 81 for men, so for most healthy individuals, delayed claiming has positive expected value purely on actuarial grounds.

What the actuarial math doesn't capture: spousal claiming strategy, survivor benefits (the lower-earning spouse should generally claim later because the higher-earning spouse's benefit becomes the survivor benefit), the value of guaranteed inflation-indexed income at older ages, and household-specific cash flow constraints that may make early claiming a necessity rather than a choice.

The 2026 environmental considerations: the COLA is 2.8%, adding roughly $56/month to the average check; the earnings limit for those under FRA all year is $24,480 (one dollar withheld per two over); for the year you reach FRA, the limit rises to $65,160 with $1 withheld per $3 over until your FRA month.

The honest planner's framing: the right Social Security claiming age depends on your longevity, your spouse's claiming strategy, your other income sources, your tax bracket, and your risk tolerance for outliving your assets. The default for most healthy individuals is to delay claiming as long as you can afford to. Your specific answer belongs in a planner's projection software, not in a generic article.

Healthcare in retirement: the $345K elephant

Fidelity's 2025 retiree healthcare cost estimate puts the lifetime healthcare spend at $172,500 for a single 65-year-old retiree and $330,000 to $345,000 for a couple — both figures excluding long-term care. The first-year spend for a couple at 65 is roughly $12,850. These numbers are not hidden, but they are also not what most retirees walk into retirement having actually budgeted for.

Medicare eligibility begins at 65 regardless of full retirement age for Social Security. Most retirees enroll in Part A (hospital insurance, premium-free for those who paid Medicare taxes for 40+ quarters) and Part B (medical insurance, with a standard 2026 premium that varies and surcharges that escalate with income). Part D handles prescription drugs; Medigap or Medicare Advantage handles the gaps Original Medicare leaves.

The IRMAA — Income-Related Monthly Adjustment Amount — is the part most retirees miss. If your modified adjusted gross income exceeds the threshold ($109,000 single, $218,000 MFJ in 2026), Medicare adds surcharges to your Part B and Part D premiums. The surcharges are tiered, and the highest tier can add several thousand dollars per year to a high-income retiree's healthcare costs. This is the constraint that interacts with Roth conversions, RMD timing, and any large taxable-account capital gains realization in retirement.

The retire-before-65 case has its own healthcare problem: ACA marketplace coverage, with subsidies that phase out as income rises. The "ACA subsidy cliff" got softer with the 2021 American Rescue Plan provisions and subsequent extensions, but the basic dynamic is that a household retiring at 60 needs to bridge five years of healthcare before Medicare kicks in, and that bridge is meaningfully cheaper if the household keeps reported income below the subsidy phase-out levels. This is the constraint that makes Roth conversions in the early-retirement years particularly delicate — a large conversion may be worth it on the long-run tax math but disastrous on the current-year ACA subsidy.

These are the kinds of trade-offs a household-specific projection has to model. They cannot be answered correctly from a blog post.

Long-term care: the uncovered nest-egg risk

Long-term care is the single largest financial risk that is not covered by Medicare and that most retirees underestimate or assume away. The national median nursing home cost in 2026 is $315 per day for a semi-private room, or $114,975 per year. Assisted living runs $70,000 to $75,000 per year nationally, and home health aide services run $60,000 to $80,000 per year. Three years of nursing home care can wipe out the retirement savings of an otherwise well-prepared household.

Three approaches to managing this risk, in order of common usage:

- Self-insure. Set aside a dedicated reserve (commonly $300,000-$500,000) earmarked for potential long-term care. Works for households with substantial wealth above what they need for ordinary retirement spending.

- Long-term care insurance. Couple combined LTC insurance premiums run approximately $2,550 to $4,675 per year at age 60, and $4,675 to $8,575 per year at age 70. The pricing is age-sensitive, the underwriting tightens with age and health, and the policies are complicated to evaluate (benefit period, daily benefit amount, inflation adjustment, elimination period, gender-distinct or unisex pricing). The traditional LTC market has shrunk significantly over the past 20 years; many of the original carriers exited, and remaining policies are more expensive than they were decades ago.

- Hybrid life-LTC products. Life insurance policies with LTC riders that pay benefits either as a death benefit (if LTC is never used) or as LTC benefits (if needed). Increasingly the dominant product in the LTC market because they avoid the "use it or lose it" problem of traditional LTC insurance.

- Medicaid spend-down planning. For households without sufficient assets to self-insure or afford LTC insurance, the eventual reality is spending down assets to qualify for Medicaid coverage of nursing-home care. The 5-year Medicaid lookback rule applies — gifts and asset transfers within five years of applying for Medicaid coverage can disqualify the application. Estate planning attorneys handle the legal mechanics; planners coordinate the financial side.

The honest framing I use with clients: this is the risk most likely to derail a well-constructed retirement plan. A 30-year retirement that ends with three years of $115,000-per-year care costs is mathematically different from one that doesn't. Whether to self-insure, buy a policy, buy a hybrid product, or plan for Medicaid spend-down depends on your wealth level, your family situation, and your risk tolerance for spending down assets that you intended to leave to heirs. The decision is too consequential to leave undiscussed.

What I'd ask a planner before retiring

If you are sitting across the desk from a planner — or interviewing one — the questions worth asking before you set a retirement date are roughly these.

- What is my current annual spending in real terms, and what does it look like in retirement? (Most households underestimate the answer by 10-20%.)

- What is my realistic Social Security claiming strategy across both spouses, and what does the projection software say about the breakeven and survivor-benefit implications?

- What is my asset location across taxable, tax-deferred, and Roth — and is it optimized for the withdrawal sequence I'll actually use?

- Does a Roth conversion ladder make sense for me given my current bracket, my projected RMD-era bracket, and the IRMAA threshold? If yes, what is the optimal annual conversion size?

- Am I going to bridge to Medicare via the Rule of 55, SEPP, taxable brokerage, or a combination? What's the income implication for ACA subsidy eligibility in the bridge years?

- How am I handling long-term care risk — self-insure, traditional LTC insurance, hybrid, or Medicaid planning?

- What is my withdrawal-sequencing plan in years where the market is down? Do I have a sufficient short-duration fixed-income reserve to avoid forced equity sales at the wrong time?

- What is my plan for surviving spouse — does the lower-earning spouse claim Social Security in a way that maximizes survivor benefits, and is the asset location appropriate for the surviving spouse's likely tax bracket?

These are the questions I work through with clients. None of them have a generic correct answer. All of them have a correct answer for your specific household, and the work of finding it is what your planner is for.

That is retirement planning in 2026, framed for a U.S. household. None of this is individual financial advice. All of it is starting material for the conversations you should be having with the people licensed to look at your specific facts.

Frequently Asked Questions

The 2026 401(k) employee deferral limit is $24,500 (up from $23,500 in 2025). Workers age 50 or older can add an $8,000 catch-up for a $32,500 total. Workers aged 60 through 63 qualify for an enhanced $11,250 super catch-up, lifting the total to $35,750. The IRA limit is $7,500 for those under 50, and $8,600 for those 50 and older.

Starting January 1, 2026, if you earned more than $150,000 in FICA wages in 2025, all your 401(k) and 403(b) catch-up contributions must go into a Roth (after-tax) account — pre-tax catch-ups are no longer permitted at this wage level. If your employer's plan does not offer a Roth option, you lose the ability to make catch-up contributions entirely until the plan adds one.

A Roth conversion ladder is a multi-year strategy of converting portions of a traditional IRA or 401(k) to Roth in low-income years, paying ordinary income tax on each conversion, then waiting five calendar years for each conversion to 'season' before withdrawing it tax-free. After year 5, the first conversion is withdrawable; year 6, the second; and so on. Best for households with a current marginal rate meaningfully lower than their projected retirement rate.

If you leave your job in or after the calendar year you turn 55, you can take penalty-free withdrawals from THAT specific employer's 401(k) — but only that plan, not from IRAs or prior employers' 401(k)s. Income tax still applies. Public-safety employees qualify at age 50. Roll your 401(k) to an IRA after leaving and you forfeit Rule-of-55 access permanently.

Fidelity's benchmark is 10x your salary saved by age 67 (with intermediate targets of 1x by 30, 3x by 40, 6x by 50, 8x by 60). Adjust for retirement age: 12x if retiring at 65, 8x if waiting until 70. Apply Bengen's updated SAFEMAX rate of 4.7% to estimate your sustainable annual withdrawal — for a $1 million portfolio, that's about $47,000 per year before Social Security.

November 2026 finalizes full retirement age at 67 for everyone born in 1960 or later — the culmination of the 1983 amendments' phased increase. Claiming at 62 still cuts your monthly benefit by approximately 30%; waiting until 70 boosts it by approximately 24% versus FRA via the 8%-per-year delayed retirement credit.

Fidelity's 2025 estimate is $172,500 for a single 65-year-old retiree and $330,000 to $345,000 for a couple — and that figure excludes long-term care. National median nursing home cost in 2026 is $114,975 per year ($315 per day for a semi-private room); assisted living runs $70,000 to $75,000 per year. Long-term care risk is the largest uncovered cost in most retirement plans and warrants a deliberate plan.