Behavioral Finance Apps: Redefining Investor Decision-Making Dynamics

Kahneman and Tversky's 1979 prospect-theory work pinned the loss-aversion multiplier at roughly 2.25 — that is, a 1% loss feels about 2.25 times as painful as a 1% gain feels pleasant (reference summary, Behavioral Economics). Almost every one of the behavioral finance apps on the market in 2026 is, somewhere in its design choices, working with or against that number. The honest analytical question is which side of the 2.25× the app is actually on.

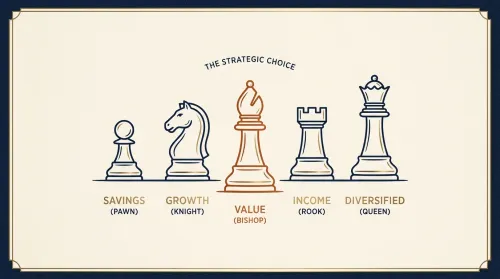

This article does what no top-ranking page for either "behavioral finance" or "best investing apps" currently does. The behavioral-finance SERP is owned by Investopedia, Wikipedia, Morgan Stanley, and the CFA Institute — all theory, zero named apps. The best-investing-apps SERP is owned by NerdWallet and Bankrate — all named apps, zero behavioral framework. The intersection is empty. Below is the working catalog: ten apps in 2026, organized into the five behavioral-design categories the discipline actually uses, with the bias each one is built to address and the trade-offs an honest review names.

The other framing that matters before getting to the apps: in January 2024, Intuit shut down Mint. Millions of users were migrated to Credit Karma, which does not have Mint's budget-envelope feature, and the ones who cared about it moved elsewhere. Most of the search volume around "behavioral finance apps" and "Mint alternatives" is the same population looking for a budgeting tool whose default behaviors actually change financial behavior rather than just visualize it. The five-category taxonomy below covers both the investing-app and the budgeting-app halves of that population.

The 5 categories of behavioral finance apps

Borrowing the working taxonomy from the Whistl 2026 Behavioral Finance Apps Guide — extended with the academic citations and the actual app roster Whistl skipped — there are five distinct behavioral-design strategies that apps in this category use. Most apps mix two or three; very few use only one.

- Impulse Control — apps that interpose friction between the impulse and the action. Spending-blocker categories, push-notification suppression during market drawdowns, app-level "wait 24 hours before this trade" defaults.

- Commitment Devices — apps that get the user to pre-commit to a behavior so the future self does not have to re-decide. Auto-rebalancing, scheduled deposits, dollar-cost averaging defaults, the IRA-match incentive structure.

- Nudge-Based — apps that use defaults, framing, and choice architecture to make the better decision the path of least resistance. Auto-enrollment in higher contribution rates, default Roth allocations, goal-visualization layers.

- Gamification — apps that use achievement loops, prize-linked savings, social leaderboards, or visual reward markers to make a desirable behavior more engaging. Done well, this category is the difference between a household that saves and one that does not. Done badly — see the Robinhood section below — it is also the difference between long-term investing and short-term trading.

- AI Coaching — apps that use conversational interfaces (Cleo, Albert, Whistl) to interrupt spending impulses in the moment and to surface patterns the user does not otherwise see.

The cleanest framework for evaluating any app in the category is: which of the five strategies does it actually use, and does the underlying behavior it promotes serve the long-term goal the user is trying to reach. The strategy is morally neutral. The alignment between the strategy and the user's actual interest is not.

The comparison table: 10 behavioral finance apps in 2026

The table below is the working roster, mapped to the five categories. Verify pricing, features, and any specific account details on the app's own site before signing up — the consumer fintech category iterates quickly and individual features get added and removed regularly. The data is current at the time of writing and will drift.

| App | Category (primary) | Behavioral mechanic | Primary bias addressed | Pricing (2026 baseline) | Best for |

|---|---|---|---|---|---|

| Acorns | Commitment Devices | Round-up auto-investing; recurring deposit defaults | Loss aversion (small "losses" feel like spare change) | Subscription tier | First-time investors who cannot get themselves to fund a brokerage account |

| Stash | Commitment Devices + Gamification | Auto-invest defaults; fractional-share education | Status quo bias | Subscription tier | Beginners who want education paired with auto-invest defaults |

| YNAB (You Need a Budget) | Commitment Devices | Forced zero-based category assignment before any spending | Status quo bias; mental accounting | Annual subscription | Households whose problem is "I don't know where the money went" |

| Monarch Money | Nudge-Based | Goal-visualization, joint-household account aggregation, post-Mint workflow | Mental accounting; status quo bias | Annual subscription | Mint refugees who want a budgeting tool with explicit goal nudges |

| Copilot | Nudge-Based | Categorization AI, monthly reports, subscription audit | Inattention bias | Annual subscription | iOS-first users who want strong categorization and a clean reporting layer |

| Rocket Money | Impulse Control | Subscription cancellation, bill negotiation, spending alerts | Inattention bias; status quo (subscriptions you forgot) | Freemium + premium tier | Households leaking money to forgotten subscriptions |

| M1 Finance | Impulse Control + Commitment Devices | Two daily trading windows; Pies auto-rebalancing across up to 100 assets | Active-trading impulse; rebalancing inertia | Brokerage; tier-based fees | DIY investors who want strong allocation discipline without daily portfolio tinkering |

| Wealthfront | Commitment Devices | Risk questionnaire (psychometric profiling, done seriously); auto-rebalancing; tax-loss harvesting | Status quo bias; behavior-gap risk | AUM-based fee | Hands-off investors who want robo-advisor management with thoughtful defaults |

| Betterment | Commitment Devices | Risk questionnaire; goal-based account structuring; auto-rebalancing | Mental accounting; behavior-gap risk | AUM-based fee | Goal-oriented investors with multiple objectives in different accounts |

| Empower (Personal Capital) | AI Coaching + Nudge-Based | Net-worth dashboard; advisor coaching layer for larger accounts | Inattention bias; mental accounting | Free dashboard + advisory tier | Households with multiple accounts who want consolidated reporting plus optional advice |

Two patterns worth pulling out of the table. First: the strongest commitment-device apps for the long-term investor (M1, Wealthfront, Betterment) are all built around defaults that reduce the daily decision burden — auto-rebalancing, scheduled deposits, trading windows. The behavior they promote is the one that compounds. Second: the strongest impulse-control apps for the budget-leak problem (Rocket Money, YNAB, Copilot) all work by making the relevant information visible before the decision is made. The point of an impulse-control app is not to make spending impossible; it is to make the second of friction that allows the conscious decision to happen.

Robo-advisor risk questionnaires are psychometric profiling — done right

The original framing of behavioral finance apps as something exotic obscures a useful fact: the robo-advisor risk questionnaires you have probably already filled out on Wealthfront or Betterment are psychometric profiling, done seriously and at scale. They are, in fact, the most widely-used behavioral-finance instrument in retail finance today.

A well-built robo questionnaire does three things at once. It establishes a baseline risk tolerance — how the household reports it would feel during a 30% drawdown — and uses that to set an initial allocation. It also captures risk capacity through liquidity questions, income stability, and time horizon, which together bound how much volatility the household can actually absorb. And it commits the user to a default allocation that the auto-rebalancer will enforce, which removes the per-quarter decision burden that creates most behavior-gap return loss.

The single most important variable an honest robo questionnaire establishes is not "what is your risk tolerance" — it is "what is the time horizon over which you should be measuring your returns." A questionnaire that lets the user select a five-year horizon and then maps them to a 90% equity allocation is doing the user a small but real disservice; a questionnaire that names the time horizon explicitly and reflects it in the allocation is doing the thing the discipline was designed to do.

For most retail investors with a single primary brokerage relationship, the robo-advisor commitment device — combined with a thoughtful initial questionnaire and rigorous auto-rebalancing — is the highest-leverage behavioral finance app available. The version that fits a given household depends on whether the user wants tax-loss harvesting (Wealthfront), goal-based account structuring (Betterment), or a hybrid with human-advisor access at a higher asset tier (Empower).

Friction as a feature: why M1's daily trading windows help

The most counterintuitive behavioral-finance design pattern is the deliberate introduction of friction. M1 Finance is the cleanest current example: the app runs two daily trading windows (morning and afternoon) rather than offering instant order execution. Per NerdWallet's 2026 review, the windows are explicitly designed to suppress active-trading impulses. The household that wants to react to a morning headline does not get to execute until the window opens — and by the time it does, the impulse has often passed.

The same logic underpins Acorns' round-up delay (round-ups accumulate and invest periodically, not instantly), YNAB's manual category-assignment requirement (every dollar gets a job before it gets spent), and the "review-and-confirm" steps that several apps interpose between a large transaction and its execution. None of these features are technically necessary. They exist because the apps' designers concluded that the user is best served when the decision is slower than the impulse.

Friction-as-a-feature is the cleanest design alignment available in this category. The app is explicitly slowing the user down on the actions that long-term outcomes favor slowing down — and not slowing them down on the actions that long-term outcomes favor speeding up. The behavior promoted by the friction is the behavior that compounds.

Related Article: Finance Mentor vs Sponsor: What Actually Compounds a Career

When behavioral design works against you: the Robinhood cautionary tale

Not every behavioral-finance design choice serves the user. Robinhood is the documented case study. The app's gamified interface (now-removed confetti animations, color-coded daily P&L visualizations, push-notification cadence around market events) was explicitly designed for engagement, and engagement maps cleanly onto active trading. NerdWallet's 2026 review (updated April 17, 2026) puts the assessment plainly: "Robinhood makes the bulk of revenue from strategies antithetical to proven long-term investing."

That is the right way to read the design choice. The features are real behavioral-finance mechanics. The bias they exploit — recency bias, the dopamine loop of immediate price feedback — is real. The user-side outcome of acting on those mechanics is, on average, worse risk-adjusted returns than the user would have achieved by doing nothing.

The honest counterweight, in fairness to Robinhood, is the IRA match. Robinhood pays a 1% match on standard IRA contributions and 3% for Gold members (NerdWallet). That is a textbook commitment-device alignment — real money that rewards the long-term retirement contribution, structurally similar to the employer 401(k) match. For a user who is going to use Robinhood anyway, funding the IRA inside the platform and turning off the trading-app notifications captures the aligned mechanic without exposing the user to the misaligned one.

The broader pattern is the rule: behavioral mechanics are tools, and the same tool can be deployed for or against the user. The discipline of evaluating an app is not "does this app use behavioral finance" — every fintech app does — but "do the specific behavioral mechanics in this app align with the long-term outcome the user is trying to reach."

The "Mint successor" shortlist: where displaced users actually went

For the post-Mint population specifically, the working five-app shortlist:

- Monarch Money — nudge-based; strong goal-visualization layer; the post-Mint default for households that want budgeting plus net-worth tracking in one place. Subscription-priced.

- Copilot — nudge-based; iOS-first; the strongest categorization AI in the category and a clean monthly-reporting layer.

- YNAB — commitment device; the most opinionated of the post-Mint options. Forces a zero-based monthly budget before any spending happens. Steepest learning curve, highest behavior-change leverage when it sticks.

- Rocket Money — impulse control; the post-Mint default for the "I keep getting charged for subscriptions I don't use" problem. Strong subscription-cancellation workflow.

- Empower (formerly Personal Capital) — AI coaching and nudge-based; the strongest free dashboard for net-worth tracking across accounts, with an optional advisory layer at a higher asset tier.

There is no single right answer in this shortlist. The right tool is the one whose defaults match the specific behavior the household is trying to change. A household that mostly needs visibility chooses Monarch or Copilot. A household that mostly needs a zero-based budget commitment chooses YNAB. A household leaking money to subscriptions chooses Rocket Money. The wrong choice for any of these problems is the one optimized for a different problem entirely.

Related Article: Youth-Led Financial Revolutions: Crowdsourcing as a Catalyst for Investment Innovation

What an app actually does about your biases

For the user who wants a working mapping from the named biases to the specific app mechanics:

- Loss aversion (the 2.25× multiplier) — Acorns round-ups defuse the "loss" of saving by reframing it as spare change; the deposit feels smaller than its actual cash-flow impact. Wealthfront and Betterment auto-rebalancing defuses the equivalent loss-aversion problem in portfolios — the rebalancer sells winners and buys losers automatically, which the human investor resists doing.

- Status quo bias — YNAB's forced category assignment, Betterment's goal-based account structuring, and any app's "auto-escalating retirement contribution" feature are all attacks on status quo bias. The default changes, the user does not have to.

- Recency bias — M1 Finance's two trading windows interpose friction between the morning headline and the trade. The behavior the friction blocks is the recency-bias-driven impulse trade.

- Mental accounting — Empower's consolidated net-worth dashboard explicitly defeats mental accounting by collapsing every account onto one balance sheet. Betterment's goal-based accounts do the opposite — they intentionally separate accounts by goal — which works better for some households and worse for others. Know which side of mental accounting your household actually needs to address.

- Inattention — Rocket Money's subscription audit and Copilot's monthly reporting are both attention-restoration mechanics. The bias is not that the spending is irrational; the bias is that the spending is unobserved.

The discipline that ties these together is the same one institutional behavioral-design programs use. The UK Behavioural Insights Team, established in 2010, and the Penn Medicine Nudge Unit treat nudges as a measurable discipline rather than a marketing aesthetic. The retail-app version of that discipline is choosing apps whose nudge architecture is documented and measurable, not just present.

What would change my mind on these recommendations

For Eli to revise the framework above, two things would have to shift. First: if the major commitment-device apps (Wealthfront, Betterment, M1) materially loosen the defaults that currently produce their long-term-investor alignment — for example, if M1 dropped the two-window trading constraint to compete with Robinhood-style instant execution — the alignment case for those apps would weaken substantially. The defaults are the product. Second: if the academic evidence base for nudge effectiveness in retail finance erodes meaningfully — the 2022 PNAS meta-analysis of 455 nudge effects across 214 publications, referenced in the behavioral-economics literature, is the current foundation — the burden on individual apps to prove their specific mechanics work would rise materially.

None of the above is individual financial advice or a recommendation to buy or use any specific app. The right app for a specific household depends on the household's actual financial goal, account structure, and the specific behavioral pattern the household is trying to change. For portfolio-allocation and account-structure decisions, talk to a licensed fee-only advisor who can see the household's specifics that no published app review can. The discipline this article tries to model is the discipline of evaluating whether an app's default behaviors align with the user's long-term goal — and that evaluation, more than any list, is the work the user has to do for themselves.

Frequently Asked Questions

An app that uses psychology — defaults, nudges, friction, commitment devices — to push the user toward better money decisions. Acorns' round-ups, Wealthfront's risk questionnaire, and YNAB's manual category rules are all behavioral finance mechanics, even when the app doesn't market itself with that term.

Yes. The risk questionnaire is psychometric profiling, automatic rebalancing defeats status-quo bias, and dollar-cost averaging through scheduled deposits defeats market-timing impulses. Wealthfront and Betterment are the cleanest examples, with Empower offering a hybrid layer for larger accounts.

Monarch Money, Copilot, YNAB, Rocket Money, and Empower picked up most of the displaced Mint users. Each leans on different behavioral mechanics — Monarch on goal visualization, YNAB on forced category assignment, Rocket Money on bill-cancellation nudges, Copilot on iOS-first categorization, Empower on consolidated net-worth tracking.

Apps that add friction — M1 Finance's two daily trading windows, Acorns' round-up defaults, Wealthfront's auto-rebalancing — outperform apps with one-tap trading when the user's goal is to stop reacting to headlines. The best app is the one whose defaults align with the behavior the user is actually trying to change.

The 2022 PNAS meta-analysis of 455 nudge effects across 214 publications shows nudges produce real but modest behavior change. The catch: the wrong nudges (Robinhood's gamified trading UI, NerdWallet's 2026 review described it as antithetical to long-term investing) can push users the wrong direction. Pick apps where the nudge architecture matches the user's actual goal, not the marketing copy.

Overlap, not identity. Every behavioral finance app uses some psychology, but only apps that are explicit about which bias they're targeting — and how — deserve the label. A pure spreadsheet replacement isn't a behavioral finance app; YNAB, with its zero-based-budget commitment device, is.

For most retail investors with a single primary brokerage relationship, the highest-leverage behavioral finance app is a thoughtful robo-advisor (Wealthfront, Betterment) or a structured DIY platform (M1 Finance) — all three are commitment-device apps whose defaults reduce daily decision burden and enforce rebalancing. For complex households with multiple goals, Empower's consolidated dashboard plus optional advisory layer adds AI coaching on top.