Mastering the Art of Client Relationship Management in Finance

The single most useful number for any advisor managing high net worth clients in 2026 is the PwC finding that 46% of US HNW investors are planning to switch or add a wealth management provider in the next twelve to twenty-four months. The honest reading of that number is that nearly half of the HNW market is in motion at any given time. The good news is that the retention playbook is mostly knowable — segmentation by tier, a defensible touchpoint cadence, the tax integration HNW clients already expect, and a generational handoff plan that is becoming non-optional as the $84 trillion ultra-high-net-worth wealth transfer plays out between 2025 and 2030. The bad news is that the playbook most advisors are running is the one from 2018, and the 46% number is the result.

I want to walk through what I think the actual disciplines are. I run a small fee-only fiduciary practice — roughly forty households at a time — and the framework below is what survives day-to-day in that context. The article is written for other advisors and for HNW readers who want to understand what a serious advisor relationship should look like under them. None of it is individual financial advice — the right structure for your specific household, or your specific practice, depends on facts I cannot see from a blog post.

What HNW, VHNW, and UHNW actually mean

A short definition block, since the SERP still surfaces a substantial amount of traffic for "what is a high-net-worth household."

- HNW (high net worth): typically $1 million or more in liquid investable assets, excluding the primary residence.

- VHNW (very high net worth): typically $5 million and above.

- UHNW (ultra high net worth): typically $30 million and above.

The thresholds are conventional rather than statutory, but the industry uses them consistently enough that any HNW-focused practice should be explicit about which tier it serves. Globally, there are roughly 23.4 million HNWIs controlling $90.5 trillion. The UHNWI subset is approximately 0.003% of the world population but holds about 13% of total wealth. The BlackRock Advisor Trends Survey reports the global UHNWI population at 426,330 individuals as of 2023 — growing 7.6% year-over-year and holding $49.2 trillion combined.

Two demographic notes worth carrying into the rest of the article. First, the US hosts roughly 40% of global UHNWIs — approximately 205,000 individuals — with New York at 16,630, Hong Kong at 12,546, and Los Angeles at 8,955. Second, the self-made share of UHNW wealth is 67.7%, with only 8.5% fully inherited and 23.7% hybrid. The old-money stereotype is not the modal HNW client. The modal HNW client is a founder, a senior executive, a partner, or a late-career professional who built the wealth and who therefore thinks about it operationally — which has direct implications for how an advisor should engage them.

Money-in-motion: the 46% switching reality

I want to open with the operational implication of the PwC switching number before anything else, because retention is the discipline that compounds.

The single seven-question self-audit I would run against every HNW relationship in a book:

- Cadence. When was the last time I delivered a written or video update on this client's specific portfolio — not a generic market note?

- Tax integration. When was the last time I led, rather than reacted to, a tax-planning conversation with this client?

- Heir introduction. Have I been formally introduced to this client's adult children, intended heirs, or trustees? If not — what is the plan to do so this year?

- Plan freshness. Does this client's financial plan reflect their actual current goals, or is it the plan from three years ago with updated balances?

- Digital experience. Does this client have a working secure portal login, a recent video review, and a clear answer to "how do I see what's happening with my money?"

- Multi-advisor coordination. Have I had a substantive conversation with this client's CPA, estate attorney, or other advisors in the past twelve months?

- Fee transparency. When was the last time I proactively walked this client through what they pay me, what they pay the underlying products, and what the total drag is on their return?

The PwC research is consistent with what I see in practice. Most of the HNW clients who leave do not leave because of returns. They leave because some combination of those seven questions has been answered "no" for too long, and a competitor — sometimes a more digital-first competitor — has answered "yes". The audit is the work.

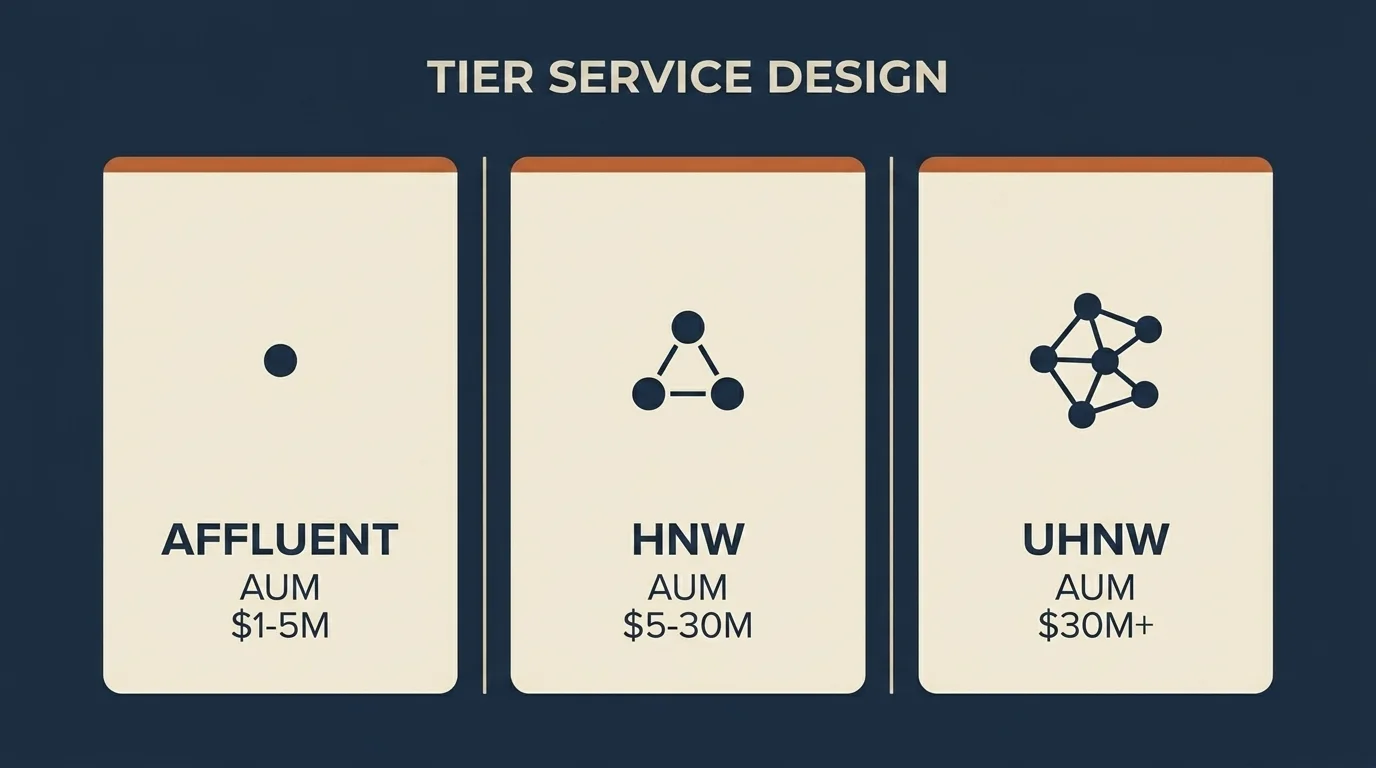

The HNW tier service-design matrix

The biggest gap I see in how the industry writes about managing HNW clients is the failure to differentiate by tier. An Affluent ($1-5M) household has materially different needs from an HNW household ($5-30M), which has materially different needs from a UHNW household ($30M+). The service model has to track the complexity, not just the AUM number.

| Service dimension | Affluent ($1-5M) | HNW ($5-30M) | UHNW ($30M+) |

|---|---|---|---|

| Review cadence | Annual full + semi-annual check-in | Quarterly full review | Monthly working contact, quarterly governance |

| Touchpoint mix | Mostly digital (portal, video, email) | Hybrid: quarterly video + annual in-person | High-touch, often family-office-coordinated |

| Product mix | Traditional 60/40 with some satellite | Add ~15% alternatives (private credit, real estate) | Heavy alternatives + direct holdings + structured products |

| Planning depth | Retirement + tax-loss harvesting + Roth ladder | Add asset location, concentrated-position planning, donor-advised funds | Add family governance, dynasty/trust structuring, multi-jurisdiction tax |

| Fee structure | AUM-based, transparent | Hybrid AUM + flat planning fee for complexity | Often retainer + AUM + project fees for special work |

| Multi-advisor coordination | Light — coordinate with CPA at tax season | Active — quarterly touch with CPA + estate attorney | Active — quarterly working meetings with the full team |

A few specific notes the matrix only hints at. The BlackRock advisor survey reports that alternative-investment allocations now sit at roughly 15% of HNW portfolios, with private equity, private credit, real estate, and (more carefully) crypto exposure showing up in the HNW band that was almost entirely 60/40 a decade ago. Roughly 55% of HNW assets are now in model portfolios, often including separately managed accounts (SMAs) and liquid alternatives. For UHNW specifically, 1 in 5 UHNWIs is foreign-born relative to their current residence and 17% own businesses headquartered outside their country of residence, which means multi-jurisdiction tax, residency planning, and currency exposure are baseline UHNW conversations rather than edge cases.

And one structural fact about service breadth. HNW-focused advisory practices offer 11.5 services on average versus 7.1 across advisory practices broadly, and nearly two-thirds of wealthy individuals work with multiple advisors at once (financial advisor + CPA + estate attorney + private banker). The competitor is not just the other RIA across town. The competitor is sometimes the client's own CPA who decides to expand into wealth management.

The $84 trillion generational handoff

The single most important multi-year HNW story is the wealth transfer in progress. UHNWI collective wealth is projected to grow from $63 trillion in 2025 to $84 trillion by 2030, with the UHNWI population expanding 33% to 734,100 by 2030. Industry-wide, the Boomer-to-heir handoff over the next two decades will be the largest intergenerational wealth movement in modern finance.

The implication for any HNW practice is that retention is now a multi-generational problem. If you are working with an aging founder couple deep in the UHNW band and you have not been introduced to their adult children, your AUM is at structural risk regardless of how well you are serving the founder.

A defensible heir-introduction structure has three pieces.

1. The family meeting. Once or twice a year, with the principals and the adult heirs in the same room (or video). The first meeting is not a planning meeting — it is a "this is the framework, this is how the family thinks about money, this is the advisor relationship the family has built". It is an introduction, not a sales call.

2. The donor-advised fund (DAF) or charitable strategy conversation. This is the lowest-stakes way to get the next generation engaged with the family's wealth — most heirs in their thirties and forties are receptive to philanthropic planning even when they are not yet interested in tax-loss harvesting. The DAF is the meeting agenda that brings the family to the table.

3. The trust and estate alignment meeting. Coordinated with the estate attorney, walks through the trust structures, the trustees, the intended timeline, and the role of the advisor across the handoff. This is the meeting that determines whether the advisor relationship survives the principal's death.

One more datum to carry through this. 76% of HNWIs under 40 list ESG as an important investment objective. If you are introducing yourself to a 38-year-old heir and your only prepared conversation is "your father liked this 60/40 allocation", you are not retaining the next generation. The values-discovery conversation is the entry point.

The 89/17 tax-trust gap

The single most consequential gap between HNW client expectation and advisor delivery in the current data is the tax-integration gap. 89% of HNW clients expect their advisor to deliver tax-planning advice; only 17% of advisors consider after-tax returns a primary driver of portfolio decisions. The 72-point spread is the largest expectation gap in the HNW data I have seen.

For an advisor who is not a CPA — which is most advisors — the question is which tax conversations are inside the scope of fiduciary financial planning and which require handoff to a tax professional. Four to six conversations are clearly inside scope.

Tax-loss harvesting. Realizing losses in taxable accounts to offset realized gains, within the wash-sale rules. Annual, mechanical, high-impact at HNW scale. The CFP and CPA both work on this.

Asset location. Placing assets across taxable, tax-deferred, and tax-free accounts so that tax-inefficient holdings (bonds, REITs, actively-managed funds) live in tax-deferred space and tax-efficient holdings (broad equity index funds) live in taxable space. Pure planning territory, no CPA required.

Roth conversion windows. Identifying the years — typically gaps between retirement and RMD age, low-income years post-business-sale, years with deductible losses available — when a partial Roth conversion will be tax-efficient at the household's specific bracket trajectory. This is the single most planning-leveraged use of the 2026 tax-code landscape.

Charitable bunching. Concentrating multiple years of charitable giving into a single high-income year using a donor-advised fund, often with appreciated long-term stock rather than cash. Tax-deductible at fair market value, capital gains avoided, and the DAF distributes to charities over time.

Concentrated-position planning. For founders and executives who hold a large fraction of their net worth in a single company stock, the multi-year exit strategy — direct sale, gifting, exchange funds, 10b5-1 plans — is squarely inside advisor scope when coordinated with the CPA and the company's compliance team.

The honest framing for a fiduciary planner is that the CPA handles the return; the planner handles the multi-year tax trajectory. A client whose advisor does not engage on that trajectory is a client whose advisor has answered "no" to question 2 of the retention audit.

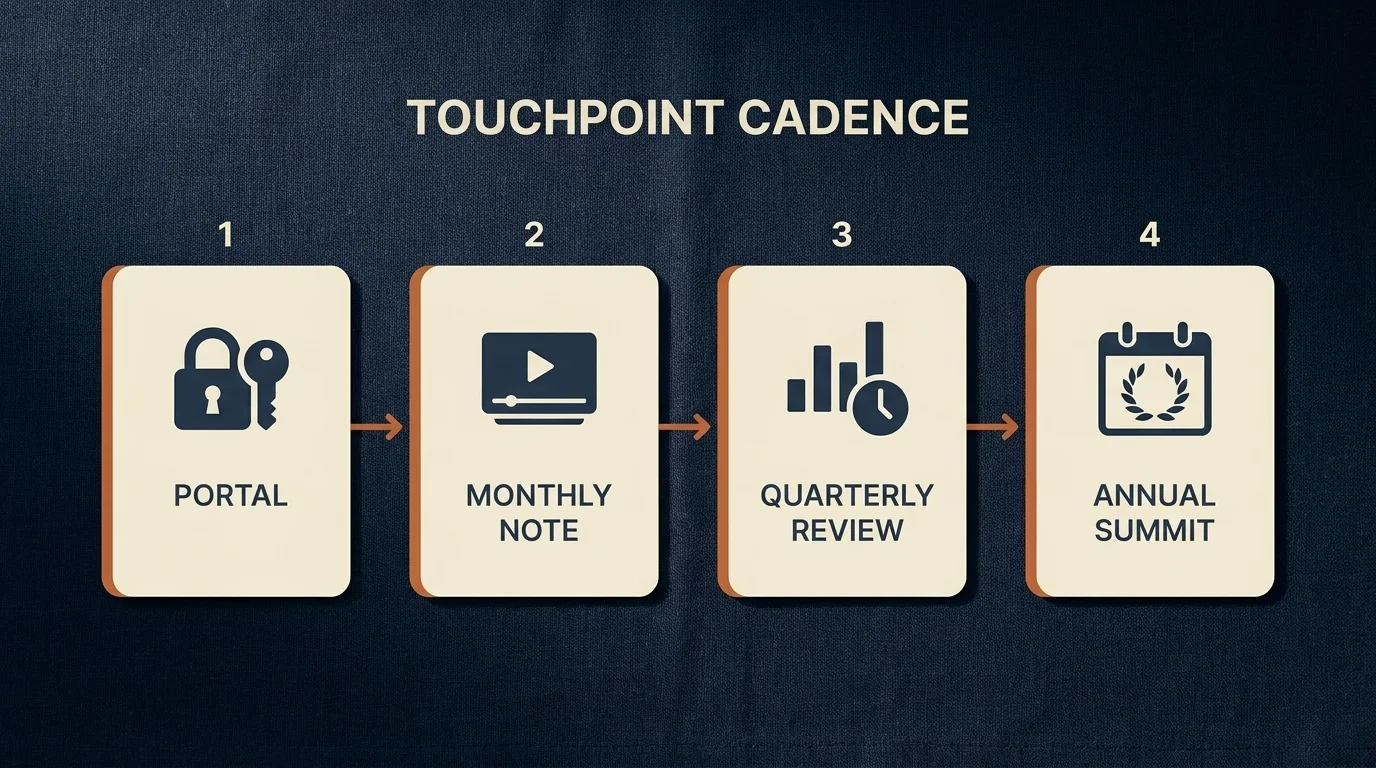

Digital-touch service blueprint

Only 1 in 5 HNW clients prefer in-person meetings as their primary advisor contact. The rest prefer remote planning, ongoing digital advice, and self-directed access for transactional activity. That is a structural shift from a decade ago, and the practices that have adapted look different from the practices that have not.

A defensible HNW digital cadence has four layers.

1. Secure portal access. Real-time portfolio view, document repository (planning summaries, statements, tax documents), and secure messaging. Table stakes in 2026.

2. Monthly market and portfolio note. Two to five minutes of recorded video covering what changed in the market and how it intersects with this client's specific situation. Generic market notes do not work — clients can read the headlines. The video has to refer to the client's plan.

3. Quarterly virtual portfolio review. Forty-five minutes, video, working through the portfolio, the year-to-date tax position, the upcoming planning items. The review is recorded and posted to the secure portal.

4. Annual in-person or full-day virtual summit. The longer working session — multi-year planning, tax projections, estate updates, generational coordination if relevant. For UHNW relationships this expands into a multi-day family meeting.

The cadence is the relationship. A client who knows when the next contact is coming and what it will cover is a client who is not interviewing competitors.

Behavioral finance for HNW conversations

The "emotional intelligence" framing in most advisor literature is vague enough to be unhelpful. The useful version is naming the specific behavioral biases that drive HNW client conversations off-track, and having a rehearsed rebuttal for each.

Loss aversion. Daniel Kahneman and Amos Tversky's finding that losses register psychologically at roughly twice the magnitude of equivalent gains. The script: "I understand the 20% drawdown is uncomfortable. The question is not whether the loss feels real — it does. The question is whether selling here changes the long-term plan, and it usually doesn't. The plan was built to absorb this."

Recency bias. The tendency to over-weight what just happened. The script: "I hear that the last three months felt different. Let me walk you back through the 25-year horizon we built the plan around, and where the last three months sit inside it."

Anchoring. Over-weighting a salient prior number (the IPO price, the all-time high, the original purchase basis). The script: "The number you're anchoring to is real, but it is not the relevant number for the decision in front of us. The relevant number is the post-tax cash this asset will produce over your remaining horizon."

Mental accounting. Treating identical dollars differently depending on which "bucket" they're in (taxable vs. retirement, founder stock vs. salary savings, "play money" vs. "real money"). The script: "I want to consolidate these decisions because the dollar is the same dollar regardless of which account it's in, and the tax cost of moving it is something we can plan for."

The list is not exhaustive — overconfidence, herding, and confirmation bias all have HNW-specific manifestations — but the four above account for most of the difficult conversations I have on a quarterly basis.

What this means for your practice

If you are running an HNW practice, three things follow from this entire framework.

First, the audit. Run the seven-question retention audit against every relationship in the book — not once, but quarterly. The clients who score "no" on three or more questions are the ones most likely to be inside the 46%.

Second, the tier discipline. Decide which tier your practice actually serves and price the service accordingly. A practice that tries to deliver UHNW service at HNW fees will burn out, and a practice that delivers Affluent service at HNW fees will lose the clients to a competitor who delivers the depth they're paying for.

Third, the generational work. Begin the heir-introduction conversation with every founder couple and every late-career household before the principal turns 70, not after. The relationships you build in those meetings are the multi-decade AUM continuity of your practice.

And the standard fiduciary caveat, the way I always close. None of this is individual financial advice. The right service model for any specific client depends on facts I cannot see — their full balance sheet, their tax situation, their family structure, their actual planning objectives. The framework is the structure of the conversation. The work is the conversation itself, done with care and at the right cadence, for as long as the relationship lasts.

Frequently Asked Questions

HNW (high net worth) starts at $1 million or more in liquid investable assets, excluding the primary residence. VHNW (very high net worth) starts at $5 million. UHNW (ultra high net worth) starts at $30 million. Each tier requires a distinct service model — cadence, product mix, planning depth, and fee structure scale with complexity, not just AUM.

46% of US HNW investors plan to change or add a wealth management provider in the next 12 to 24 months, according to PwC research. That makes retention — not new-client acquisition — the single most consequential discipline of the current cycle, and most defections track to gaps in cadence, tax integration, heir introduction, or digital experience rather than to portfolio returns.

UHNWI collective wealth is projected to grow from $63 trillion in 2025 to $84 trillion by 2030, with the UHNWI population expanding 33% to 734,100. The Boomer-to-heir handoff is the largest intergenerational wealth movement in modern finance, and any HNW practice without an explicit heir-introduction strategy is at structural risk regardless of how well it serves the current principals.

A defensible cadence is a secure portal with real-time access, a monthly two-to-five-minute portfolio-specific video note, a quarterly virtual portfolio review, and an annual in-person or full-day virtual planning summit. Only 1 in 5 HNW clients want in-person as their primary touchpoint — the rest prefer remote planning with digital self-direction for transactional activity. For UHNW relationships the cadence expands into monthly working contact with quarterly governance meetings.

89% of HNW clients expect tax-planning advice; only 17% of advisors lead with after-tax returns — a 72-point expectation gap. A non-CPA fiduciary advisor can credibly lead on four to six tax conversations: tax-loss harvesting, asset location, Roth conversion windows, charitable bunching via donor-advised funds, and concentrated-position multi-year exit strategy. Coordinate the rest with the client's CPA.

Trust at the HNW level comes from four disciplines, in order: tier-appropriate service depth (the right cadence and product mix for the asset level), tax integration (closing the 89/17 expectation gap), generational coordination (formal heir introductions before the principal turns 70), and fee transparency (proactively walking the client through all-in costs annually). Generic 'transparency in communication' and 'consistent performance' are necessary but not sufficient.

Name the specific behavioral bias driving the conversation. Loss aversion: 'The question is not whether the drawdown feels real — it is. The question is whether selling here changes the long-term plan.' Recency bias: 'Let me walk you back through the 25-year horizon we built the plan around.' Anchoring: 'The number you're anchoring to is real but is not the relevant number for the decision in front of us.' The rebuttal scripts depend on which bias is active, and the right script in the right moment matters more than generic empathy.

HNW households have heterogeneous balance sheets and complex multi-jurisdiction tax situations — 1 in 5 UHNWIs is foreign-born and 17% own businesses in different countries from their residence. The 67.7% of UHNW wealth that is self-made comes from founders and senior professionals who think about money operationally. A standardized service model fails this population by design; the practices that retain HNW clients build a service blueprint per household, anchored on cadence, tax trajectory, and generational coordination.

The practical version of emotional intelligence in advisor work is naming the specific behavioral bias driving a client conversation and having a rehearsed rebuttal for each — loss aversion, recency bias, anchoring, mental accounting, overconfidence, herding. Generic 'empathy and active listening' is too vague to deploy. The named-bias rebuttal scripts, used in the right moment, are what separate advisors who hold clients through a 20% drawdown from advisors who lose them.

Run a seven-question quarterly retention audit on every relationship: portfolio-specific cadence; advisor-led tax planning; formal heir introduction; plan freshness; secure portal and digital experience; multi-advisor coordination with CPA and estate attorney; proactive fee transparency. Clients who score 'no' on three or more questions are the ones most likely to be inside the 46% PwC switching population — and the audit identifies the specific gap to close before they shop you.