Culinary Capital: The Rise of Foodpreneurs in Personal Finance Pursuits

The question I am asked most often, by people considering becoming a food entrepreneur, is some version of: how much money do I actually need to start, and where does it come from. The honest answer in 2026 is that the capital environment for food and beverage has tightened materially, that almost nobody raises venture capital for a food business — and that the founders quietly making this work are using a stack of older, less glamorous funding paths that the financial media rarely writes about. I want to walk through what that stack actually looks like, who has used it, and what the numbers underneath it look like.

I am not writing this as a coach. I built a specialty food brand from a farmers' market stand into a profitable seven-figure business with thirty-one employees across two facilities, and I am writing as someone who made payroll through a quarter where our largest customer pushed terms from net-30 to net-45 and our ingredient suppliers tightened to net-15 the same month. That is the lens.

How food entrepreneurs raise capital in 2026

The first thing to know is the context. 2026 is being described by trade press as "one of the toughest fundraising environments" for food and beverage startups. Pre-seed and seed activity is quiet. Investors are demanding traction, clean cap tables, and meaningful pilot results before they will write a check. The founders who are getting funded are the ones who can show real revenue, real gross margin, and a real customer who is paying retail price.

Some of that is sector-specific gravity. Total US restaurant industry sales for 2026 are forecast at $1.55 trillion and global foodservice sales at over $4 trillion, so it is not that the market has shrunk. But the venture capital that does flow into food and beverage is competing for attention against AI, which absorbed roughly $211 billion — about half of the $425 billion of global VC deployed in 2025. A food entrepreneur pitching against an AI startup is not pitching the same investor on the same terms.

Three other shifts matter for anyone planning 2026 capex.

First, FoodTech venture capital has reweighted. About 60% of FoodTech VC dollars now target climate-focused startups with measurable impact — sustainable ingredients, climate-smart agriculture, food-as-medicine, AI-driven supply chains. A traditional restaurant or specialty food brand is no longer the FoodTech VC story.

Second, restaurant M&A is forecast to rebuild into 2026 after three years of declines, and the restaurant IPO window may reopen for brands with strong unit economics and scalable concepts. If you are a foodpreneur with the right shape of business, the exit door is opening at the same time the entry door is narrowing.

Third, AI and automation capex is now a hard budget line, not a maybe. 82% of restaurant executives plan significant 2026 increases in AI tech investment, and roughly 55% of fast-casual operators are already running kitchen-display AI, smart ovens, or robotics — cutting cook times by about 30% and order errors by about 50%. A new entrant who plans 2026 capex without an AI/automation line is planning the wrong year.

I am pairing those numbers with one quote I think captures the moment, from Daniel Scharff at Startup CPG: in the current environment, founders are layering "alternative/non-dilutive financing" — equity crowdfunding, friends and family, SBA loans, angels, grants — rather than chasing a VC round. That is the stack that actually works in 2026, and it is what the rest of this article is about.

Named food entrepreneur case studies

The clearest way to show this is with real founders who have closed real rounds.

Eat Happy Kitchen raised approximately $700,000 via equity crowdfunding — directly from the existing audience of its companion cookbook. The structural lesson here is that an existing audience is itself a capital stack. If you have built a brand that has people who already buy from you, equity crowdfunding can pull from that base on terms a generalist VC would not match.

Kahawa 1893 has been cited as a capital-efficiency benchmark — roughly $20 of revenue generated per $1 of capital raised. I want to underline what that ratio actually says: it says the business converted capital into revenue at high enough efficiency that growth was not bottlenecked by needing the next round. That is the kind of unit economics that survives a tight capital environment.

Uncle Waithley's blended angel investment with SBA debt, which is the most common mid-sized food entrepreneur stack in my experience and worth describing plainly. Angels write the early equity that lets you set up production and prove the unit economics. SBA debt — once you have a track record — funds the working capital, the equipment, and the expansion. Together they are cheaper than a pure equity round and they leave the founder with more of the company.

DEFI Snacks and RIP Cold Brew are the bootstrap stories — founded out of personal savings, no outside equity at the start. The bootstrap path is rarely written about because it does not generate press releases, but it is the modal path. Roughly 77% of all startups rely on personal savings for initial funding, and food businesses are not the exception.

Whoa Dough raised through small-business loans — the boring, debt-driven path that most founder profiles skip over. If your concept generates predictable cash from day one, debt is often cheaper than equity, and it does not put a board on your business.

Five companies. Five different stacks. None of them required venture capital, and none of them are unusual. This is what the actual funding landscape looks like for a foodpreneur in 2026.

Restaurant investment vehicles compared

If you are evaluating which vehicle to use — or which combination — the table below is the version I would draw on a whiteboard for a founder sitting across the desk. Numbers and constraints are pulled from the SBA, FoodNavigator-USA, and the broader 2026 capital-environment sources cited above.

| Vehicle | Typical size | Dilution | Time-to-close | Restaurant/food-brand fit | 2026 availability |

|---|---|---|---|---|---|

| SBA 7(a) loan | Up to $5M cap | None (debt) | 45–90 days | Strong — covers real estate, equipment, working capital, refinance, change of ownership | Open; tiered rate ceilings under the Working Capital Pilot |

| SBA microloan | Up to $50k | None | 30–60 days | Good for startup capex, equipment, inventory | Open |

| Equity crowdfunding | $100k–$1M+ | Equity (broad cap table) | 60–180 days | Strong fit when you have an existing audience or local following | Open and growing |

| Angel round | $50k–$500k | Equity | 30–120 days | Good for early concept proof + relationship capital | Selective; angels are demanding traction in 2026 |

| Friends and family | $10k–$100k | Either (often convertible notes) | Days–weeks | Common, fast | Always available; risk is relational, not financial |

| Non-dilutive grants | $5k–$250k | None | Variable | Strong for climate-positive, regional, or minority-founder concepts | Wider in 2026 — non-dilutive financing is the trade-press headline |

| Restaurant REITs / institutional capital | $5M+ | Varies | Months | Real estate side only; not for the operator | Reopening with M&A unfreeze |

| Ghost-kitchen franchising | Variable | License fee model | Weeks | Good for delivery-first concepts with lower capex | Active |

| Venture capital | $500k–$10M+ | Equity (significant) | 90–180 days | Weak fit unless you are FoodTech with climate or AI angle | Tight; only ~0.05% of startups raise VC |

A few things to read out of that table. The SBA 7(a) is the workhorse for any food entrepreneur who has any kind of track record — its $5M cap and the Working Capital Pilot's tiered rate ceilings (base + 6.5% for ≤$50k, +6.0% for $50k–$250k, +4.5% for $250k–$350k, +3.0% above $350k) make it the cheapest scaled capital you are going to find. Equity crowdfunding is the vehicle that most underrated by founders who do not know they have an audience. Venture capital is the one vehicle on this table that most readers should write off entirely.

Funding paths for foodpreneurs without VC

If only 0.05% of startups raise venture capital, the planning question for most food entrepreneurs is not "how do I get a term sheet". It is "how do I assemble a funding stack from everything else". That stack usually has three or four layers.

The first layer is personal capital and friends-and-family. Roughly 77% of startups begin here. The number is not a moral verdict — it is a description of how the financing market actually works. The discipline at this layer is to know exactly how much of your household balance sheet you are committing and to put it in writing for the people who are lending into the business with you. I have seen more founder relationships ruined by undocumented family loans than by failed businesses.

The second layer is small SBA debt or microloans. The SBA microloan program tops out at $50k and is set up specifically for the kind of equipment and starting inventory most food businesses need. It is slower than a credit card and faster than equity. If you cannot service a $50k loan from projected gross margin in year one, the concept needs a closer look before you raise anything larger.

The third layer is equity crowdfunding or angels for the production-scale step. This is the Eat Happy Kitchen path — turn the audience you already have into the investor base. Or it is the angel route, where the early check buys you not just dollars but a relationship with someone who has built a comparable business and can open doors.

The fourth layer is growth-stage SBA 7(a) for working capital and expansion. This is where Uncle Waithley's lives — angel equity for proof, SBA 7(a) for the scale-up. It is the cleanest large-dollar stack I have seen used in food, and it leaves the founder with more of the company than any equivalent equity round.

The thing I want to name plainly: profitable businesses and fundable businesses are not the same thing, and the playbooks are different. Most food entrepreneurs should be building the first kind. The financial media is almost entirely written about the second one, which is why most founders feel like they are failing when in fact they are simply playing a different and usually better game.

Profit margins and the failure curve

I want to bring two tables together because they only make sense as a pair.

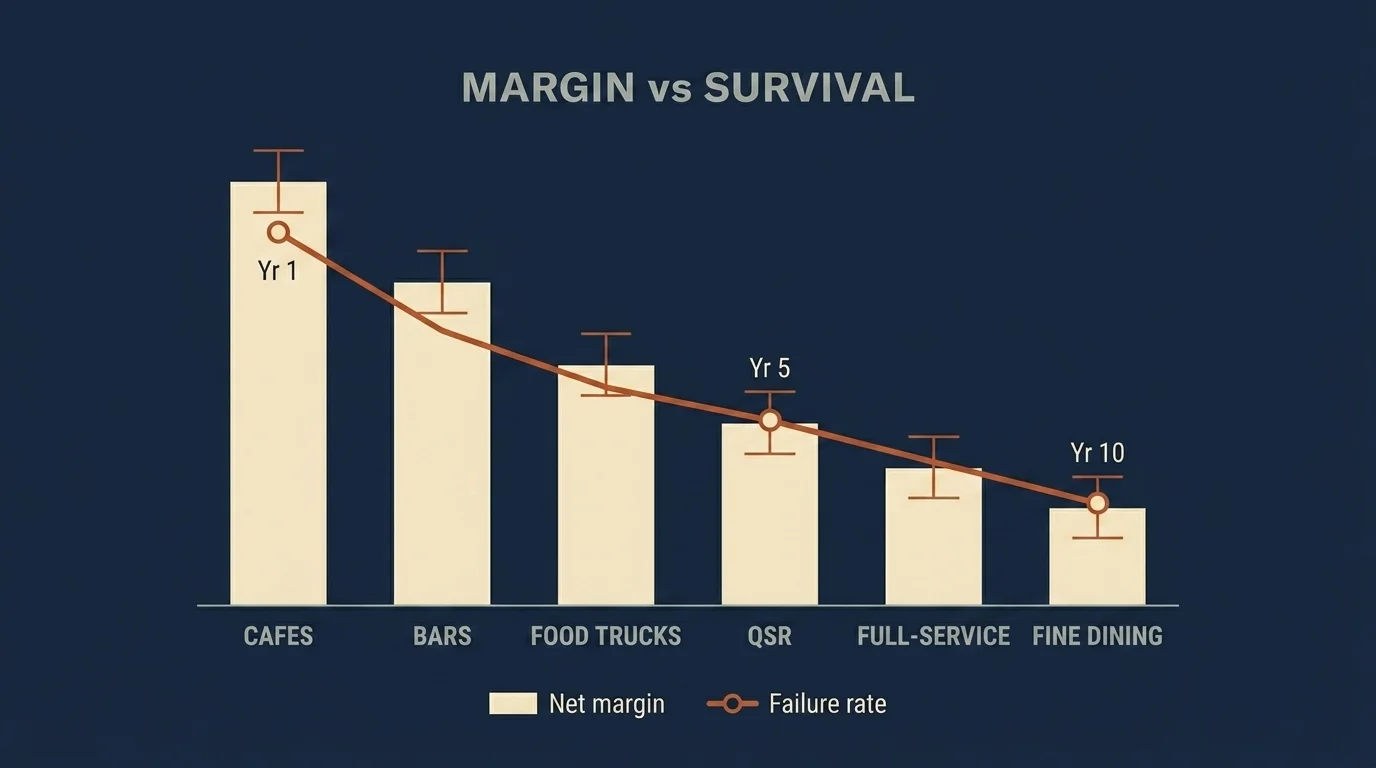

The first is the profit margin by restaurant concept in 2026:

| Concept | Net margin |

|---|---|

| Cafes / fast-casual | 12–18% |

| Bars | 10–15% |

| Food trucks | 7–15% |

| Quick-service (QSR) | 6–9% |

| Full-service | 2–6% |

| Fine dining | 2–5% |

The second is the startup failure curve across all sectors:

| Time | Cumulative failure rate |

|---|---|

| Year 1 | 20.4% |

| Year 5 | 49.4% |

| Year 10 | 65.3% |

These two tables are the central decision frame for a food entrepreneur. A fine-dining concept running at 2–5% net margin has almost no room to absorb a bad year, and food businesses live in a sector where 42% of US restaurants entered 2026 unprofitable. A fast-casual or food-truck concept running at 12–18% has structurally more cushion against the same shock. This is not a recommendation of one concept over another. It is a statement that the concept choice is itself the funding choice — because it determines how much of a margin error your stack has to absorb.

Two more numbers worth carrying through the planning. The top two causes of startup failure are no-market-need (42%) and cash flow / financial mismanagement (29%). Both of those are funding-stack problems before they are operational problems. A founder who has pre-sold product to a defined audience has solved the first cause before raising. A founder who has built a stack that does not depend on the next funding round closing on time has solved the second.

And one labor number, because it is now the dominant operating cost in this industry: 78% of restaurants are understaffed, turnover is 75%, average days to fill a position is 21, and average hourly earnings hit $21.57 in January 2026. 98% of operators cite labor costs as a top concern. If your concept's profit margin assumes a labor cost you cannot actually hire at, the margin is theoretical.

Foodpreneur archetypes that actually win

A few founder-level patterns are worth naming, because they cut against the dominant founder narrative.

A 50-year-old founder is roughly 3x more likely to succeed than a 20- or 30-year-old. Repeat founders — including those who previously failed — outperform first-timers at about 20% success versus 18%. The cultural story of food entrepreneurship is the young founder with the dream. The data story is the operator with twenty years of industry experience who knows the cost of every ingredient and has watched at least one business cycle.

The second pattern is what trade press is now calling the "viral / community-built" brand path — founders launching from home kitchens, online communities, and existing audiences without formal food-industry training or VC backing. The 2026 brand-watch lists explicitly highlight this archetype, and it is the only first-time-founder profile I think has a real edge in the current environment. The edge is that the audience is the cap stack — you have validated demand and built a distribution channel before you have raised. That is the same structural advantage Eat Happy Kitchen used.

If you are thinking about food entrepreneur ideas, the question to start with is not "what would I love to cook" — it is "where do I already have an audience, a distribution channel, or a margin advantage that the rest of the market does not have". The answer to that question is the concept worth funding.

A check you can run this week

Here is the specific check you can run on your own situation this week — whether you are an aspiring food entrepreneur planning a launch, or an operator a year or two in deciding what to fund next.

Pull the realistic gross margin of the concept you are planning. Subtract a realistic labor line — not a hopeful one, the one that reflects $21.57 an hour for the staff you will actually be able to hire. Subtract rent, utilities, and ingredient cost variance. The number left over is your monthly contribution margin per unit of throughput. Multiply that by your honest unit volume in month six. That is the cash the business will actually generate in its first half-year. If that number does not service the debt or the runway in your funding stack, the stack is wrong — not the concept, not the market, the stack. Fix the stack before you commit the capital.

Two final caveats from the way I write about money. None of this is individual financial advice — the right funding decision for your situation depends on facts I cannot see from a blog post, including your personal balance sheet, your local market, your tax situation, and the specific contracts on your table. Before you commit to any stack of equity, debt, and personal capital, talk to a licensed advisor or a fiduciary planner who can see the whole picture. The numbers I have walked through are the right inputs to that conversation, not a substitute for it.

Frequently Asked Questions

Startup capex varies sharply by concept. Food trucks can launch under $100,000; full-service restaurants typically require $250,000 to $750,000 or more in capex before opening. SBA 7(a) loans cap at $5 million and cover real estate, equipment, working capital, and refinancing — making them the most common scaled debt vehicle for food entrepreneurs in 2026.

The maximum 7(a) loan is $5 million. The 7(a) Working Capital Pilot tiers maximum rate spreads by loan size: base plus 6.5% for loans up to $50,000, plus 6.0% for $50,000–$250,000, plus 4.5% for $250,000–$350,000, and plus 3.0% for loans above $350,000. Eligible uses include working capital, equipment, real estate, debt refinance, and change-of-ownership — all common food entrepreneur needs.

Across all startups, 20.4% fail in year one, 49.4% by year five, and 65.3% by year ten. The two leading causes are no market need (42% of failures) and cash-flow or financial mismanagement (29%). For food specifically, 42% of US restaurants entered 2026 unprofitable — concept choice (and therefore funding-stack choice) is the dominant variable.

Only about 0.05% of startups raise venture capital, and roughly 77% rely on personal savings to start. Recent food entrepreneurs are layering SBA loans, equity crowdfunding, angel investment, friends-and-family debt, and non-dilutive grants — the stack the F&B community now calls 'alternative financing.' Eat Happy Kitchen raised $700,000 in equity crowdfunding from its existing cookbook audience; Uncle Waithley's used an angels + SBA blend; DEFI Snacks and RIP Cold Brew bootstrapped from personal savings.

In 2026, cafes and fast-casual lead at 12–18% net margin, followed by bars (10–15%) and food trucks (7–15%). Quick-service runs 6–9%, full-service 2–6%, and fine dining the thinnest at 2–5%. The margin a concept can sustain is the single most important variable a food entrepreneur should price into their funding stack before committing capital.

A foodpreneur is a food entrepreneur — someone who has built a food business, whether a restaurant, specialty food brand, food truck, or food-adjacent enterprise. They sit at the intersection of personal finance and operating a business: every personal-finance decision they make (debt service capacity, household runway, tax structure) interacts directly with how the business is funded and how much of it they retain. For most people, building a food business is the largest single capital allocation of their working life.