Demystifying Cryptocurrency: A Beginners Guide to Digital Assets

The number I keep coming back to when someone asks me where to start with cryptocurrency for beginners is not a bitcoin price. It is the spot Bitcoin ETF figure: U.S. spot Bitcoin ETFs have crossed $150 billion in assets under management by early 2026, with BlackRock's IBIT alone holding roughly $55 billion. What that number actually measures is the share of bitcoin exposure that has migrated into ordinary brokerage accounts in the eighteen months since the ETFs went live. What it does not tell us is whether any individual reader of this guide should buy any of it — that is between you and a licensed financial advisor — but it does tell us the world a beginner is walking into is structurally different from the one most "intro to crypto" articles describe.

This guide is for people who want the honest version of how the asset class currently works in the United States in 2026: how it is built, what kinds of tokens exist, how to actually buy a small amount, where to keep it, what the regulators have finally clarified, and where the real risks are. I am not going to predict prices, and I am not going to pretend most of what gets called "crypto" is anything other than speculation with good branding. But there is a small portion of it that is interesting, and it is worth knowing how to tell the two apart.

How blockchain and cryptocurrency actually work

A cryptocurrency is a digital token whose ownership and transfers are recorded on a blockchain — a database that is replicated across many independent computers (called nodes) instead of held inside a single bank or company. When you send a token, those nodes collectively verify the transaction and bundle it into a block of recent transactions, which is then linked to the previous block via a cryptographic hash. The chain that results is append-only: changing an old block would invalidate every hash that follows it, which is what makes the ledger tamper-resistant.

The mechanism that decides which node gets to add the next block is the consensus algorithm. The two that matter for beginners are proof of work and proof of stake.

Proof of work vs proof of stake

In proof of work, nodes (called miners) compete to solve a computationally expensive puzzle. The first to solve it gets to add the next block and is paid a block reward in the network's native token. This is how Bitcoin works. The honest version of why it works: solving the puzzle is expensive, so attacking the network costs money, which makes attacks unprofitable in equilibrium. The honest version of the cost: it consumes a lot of electricity. That is the trade-off.

In proof of stake, validators are chosen to add blocks in proportion to how much of the native token they have locked up (staked) as collateral. Misbehave and your stake gets slashed — that is the cost that replaces the electricity bill. This is how Ethereum works since The Merge in 2022, and it is how nearly every smart-contract chain launched after 2020 works.

Neither mechanism is morally superior. They make different trade-offs around energy consumption, decentralization, and finality. What matters for a beginner is just knowing the term so the next time someone says "ETH staking yield" you know they mean validator rewards on a proof-of-stake chain, not interest from a bank.

What changed in 2024–2026

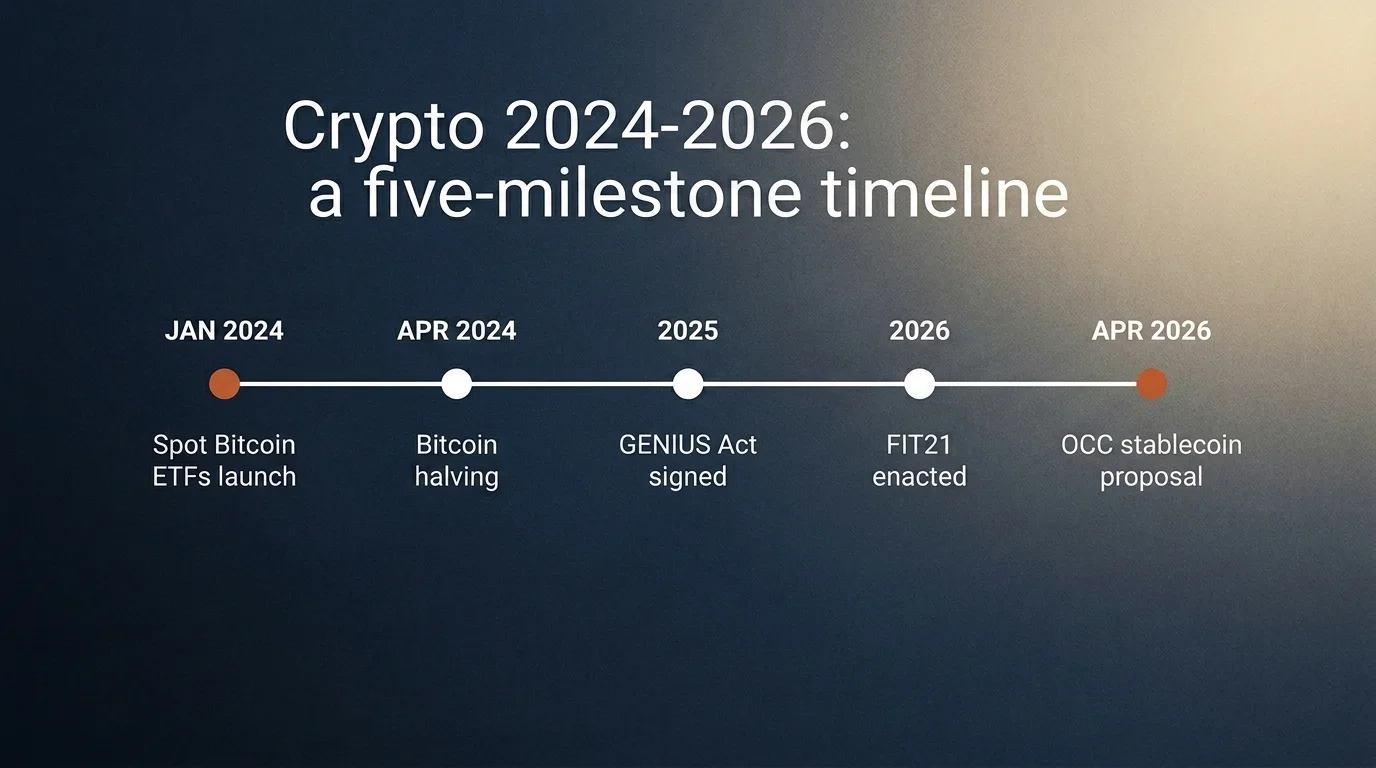

Most of the beginner-crypto content on the open internet was written between 2019 and 2023. That timing matters because the U.S. regulatory and product landscape has shifted more in the eighteen months between January 2024 and April 2026 than in the entire decade before it.

- January 2024 — Spot Bitcoin ETFs went live. By early 2026, combined AUM crossed $150 billion, with BlackRock's iShares Bitcoin Trust (IBIT) alone holding roughly $55 billion. Morgan Stanley's spot Bitcoin ETF (MSBT) launched in early April 2026, bringing another tier-one Wall Street brand into the product. For a beginner, the practical consequence is that you can now get bitcoin price exposure inside an ordinary IRA or brokerage account without ever touching a wallet.

- April 20, 2024 — The Bitcoin halving. The block reward dropped from 6.25 BTC to 3.125 BTC, the fourth halving in Bitcoin's history. Halvings cut the issuance rate of new BTC in half every four years. They are not, by themselves, a price catalyst — they are a programmatic supply event that traders pretend is a price catalyst.

- 2025 — The GENIUS Act became law. The first federal U.S. stablecoin framework. I will cover the details in the stablecoin section below; for now, the headline is that the global crypto market briefly crossed $4 trillion after enactment.

- FIT21 (Financial Innovation and Technology for the 21st Century Act). Defined the SEC vs CFTC jurisdictional split that the industry had been litigating in federal court for the previous five years. I will cover this in the regulation section below.

- April 2026 — The OCC published its GENIUS Act implementation proposal. Federal regulator framework for stablecoin issuers is now being formalized, with both federal pathways and state-level options for issuers under $10 billion in outstanding tokens.

- Tax year 2025 — Form 1099-DA became real. Crypto brokers must now report digital-asset transactions to the IRS. Forms for 2025 transactions were mailed by February 17, 2026. Cost-basis reporting begins for 2026 transactions, with those forms arriving in early 2027.

If you read a beginner-crypto guide that does not mention any of the above, it is out of date.

Types of cryptocurrency: the distinction that actually matters

There are tens of thousands of tradable tokens. Listing them is a poor use of a beginner's attention. The distinction that matters is this: a protocol that generates fee revenue from real users paying for real economic activity is a different thing from a token whose price chart is correlated with bitcoin. The first one is something you can analyze. The second one is a speculative asset whose price is driven by liquidity and sentiment. Both can make or lose you money. Only one of them is investable in any rigorous sense of the word.

With that filter in mind, here are the categories worth knowing.

| Category | Examples | What it actually is | Beginner relevance |

|---|---|---|---|

| Bitcoin | BTC | A fixed-supply, proof-of-work monetary asset. No general-purpose programmability. | The benchmark. Every other token's price is implicitly priced against it. |

| Smart-contract platforms | ETH, SOL, AVAX, others | Proof-of-stake networks that run programmable applications and collect transaction fees from users. | The protocols here generate measurable fee revenue. You can analyze them like a business. |

| Stablecoins | USDC, USDT, others | Tokens pegged to $1 USD, backed by reserves (cash, Treasuries) held by a regulated issuer. | Increasingly the actual payment rail of crypto. See dedicated section below. |

| DeFi tokens | UNI, AAVE, others | Governance tokens for specific decentralized-finance protocols (lending, trading). | Highly variable. Some have real fee revenue, most are correlated speculation. |

| Memecoins / altcoins | Pick any | Tokens whose primary value driver is attention and liquidity rotation. | Speculation. Sized accordingly or not at all. |

When you hear someone talk about "Ethereum" and "Cardano" and "Ripple" in the same breath, what they are doing is conflating very different things. Ethereum settles billions of dollars of stablecoin transfers and DeFi activity per day and earns fee revenue from doing so. The honest version of what most other Layer 1s do is: they wait to see whether enough activity migrates to them to justify their valuation, and most do not.

Stablecoins: what the GENIUS Act actually changed

If I had to pick the single most important development for beginners since 2024, it would not be the ETF approval. It would be the GENIUS Act, signed in 2025, because it converts stablecoins from a regulatory grey zone into a clearly regulated payment instrument.

A stablecoin is a cryptocurrency that is pegged to a stable reference value, almost always $1 USD. The two largest by supply are USDC (issued by Circle) and USDT (issued by Tether). They are the rails on which most non-bitcoin crypto activity actually moves — when someone "buys ETH on an exchange" what is actually happening behind the scenes is usually USDC-for-ETH, not dollars-for-ETH.

Under the GENIUS Act, U.S.-issued stablecoins must:

- Be backed 100% by cash or short-term U.S. Treasuries (no commercial paper, no riskier collateral).

- Publish monthly reserve disclosures.

- Comply with AML and sanctions rules.

- Pay no interest to holders (regulators wanted to keep them as payment instruments, not yield products).

- Give holders priority in any issuer insolvency — meaning if the issuer fails, stablecoin holders get paid before general creditors.

FIT21 separately classifies these tokens as "Permitted Payment Stablecoins", explicitly not securities and not commodities. That distinction matters because it removes the legal ambiguity that hung over the entire sector through 2024.

What the GENIUS Act does not change: foreign-issued stablecoins, which still operate under whichever regime their issuer's jurisdiction provides. USDT, the largest stablecoin globally, is issued offshore. That is a different risk profile than USDC, and a beginner should know that before treating the two as interchangeable.

How to buy your first $50–$100 of crypto

The process below is exchange-agnostic and assumes you have decided, with appropriate professional advice if needed, that owning a small amount of bitcoin or ether is something you want to do. If you are not at that point, skip this section.

- Pick a regulated U.S. exchange. The mainstream options are Coinbase, Kraken, and Gemini. They differ on fees and interface, but all three are U.S.-registered, hold the relevant state money-transmitter licenses, and segregate customer assets. Most of them allow purchases as low as $1–$5 via fractional buying, which means you can experiment with the mechanics on a tiny amount before committing more capital.

- Complete KYC. You will be asked for ID and proof of address. This is the same know-your-customer process you went through to open a brokerage account. There is no reputable U.S. exchange where you can skip it, and the ones that promise you can are not where a beginner should be.

- Fund the account. ACH transfer is the lowest-fee option for most exchanges. Wire transfer is faster but costs more. Debit-card buys are the fastest but the most expensive — typically a 3–4% premium baked into the fee structure.

- Buy a fractional amount. You can own 0.0001 BTC. There is no minimum imposed by the asset itself; the minimums are imposed by the exchange and are typically small.

- Decide on custody. Leaving your coins on the exchange is convenient. It is also the configuration that produced 2022's largest losses. The custody section below covers the alternatives.

That is it. The mechanics are not the hard part. The hard parts are everything around the mechanics — sizing, custody, tax reporting, and not being scammed.

Custody: where the rubber meets the road

I lived through the 2022 cycle inside a fund that did not blow up, and the uncomfortable thing I learned watching the ones that did is that custody matters more than anything else the industry has built. The collapses of Terra, Celsius, Three Arrows Capital, and FTX were not a single phenomenon — they were four different failures that shared one thing: customers had handed over the keys and trusted an intermediary to keep them safe. In the FTX case, the intermediary was committing fraud. In the Celsius case, it was running an unsustainable yield. In each case, the customers who had self-custodied their coins lost nothing. The customers who had not, lost everything.

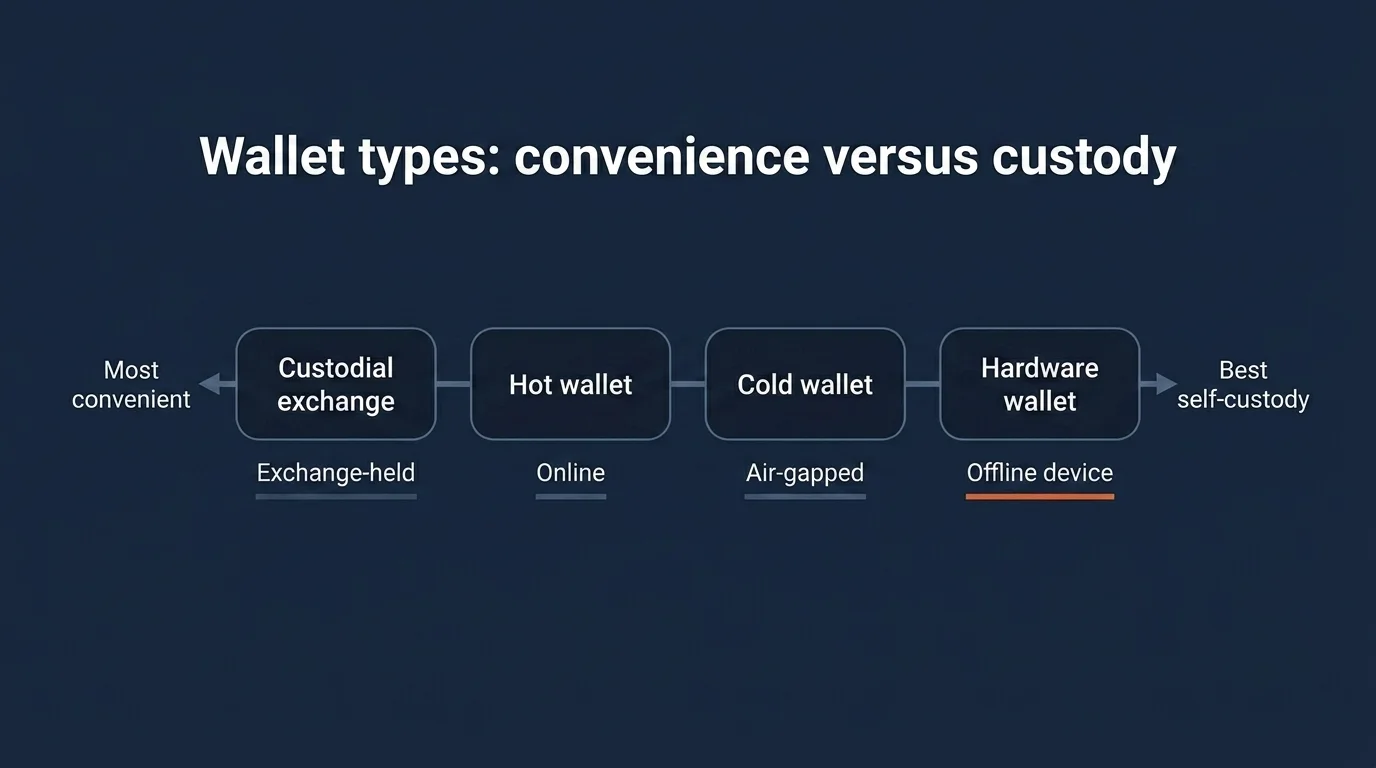

A wallet, in crypto, is not where your coins live — your coins live on the blockchain. A wallet is the software or hardware that holds the private keys that authorize you to move them. Whoever controls the keys, controls the coins.

Cold wallet vs hot wallet, hardware vs software

| Wallet type | Who controls keys | Online? | Typical use | Beginner fit |

|---|---|---|---|---|

| Custodial (exchange) | The exchange | Online | Active trading, fiat on-ramps | Convenient. Riskiest. Not a long-term storage solution. |

| Hot software wallet | You | Online | Day-to-day onchain activity, DeFi | Good for small balances and learning the mechanics. |

| Cold software wallet | You | Air-gapped | Larger balances on a dedicated device | Better than hot, harder than hardware. Niche. |

| Hardware wallet | You | Offline | Long-term holdings | The right answer for any meaningful balance. |

A "hot" wallet is connected to the internet — your phone, your browser, your laptop. A "cold" wallet is not. Hardware wallets (Ledger, Trezor, Coldcard, others) are purpose-built devices that hold your keys offline and only sign transactions when you physically authorize them. They are the standard for any beginner crypto wallet decision involving more than a few hundred dollars of holdings.

If a single piece of advice in this guide saves a reader from material loss, it is this: do not store more than you can afford to forget on a centralized exchange. The exchanges in 2025 are better-regulated than the ones that failed in 2022. They are not infallible.

Seed phrase hygiene

When you set up a self-custodial wallet, it gives you a recovery phrase — typically 12 or 24 words. That phrase IS your wallet. Anyone with the phrase can drain the wallet. Anyone without the phrase, including you, cannot recover it if the device is lost.

The only correct ways to store a seed phrase are: written on paper or stamped into metal, in two physical locations you control, never typed into any internet-connected device, never photographed, never emailed, never stored in a password manager that syncs to the cloud, never shared with anyone — including a "support agent" who contacts you about a "wallet issue." Support agents do not exist. The phone number on the back of the hardware wallet box is the only legitimate channel.

Cryptocurrency scams: $11.4 billion in 2025

I want this number to land. Americans lost $11.4 billion to cryptocurrency scams in 2025, a 22% increase from 2024, across 181,565 complaints filed with the FBI's Internet Crime Complaint Center. Crypto-linked fraud accounted for more than half of all U.S. internet fraud losses ($20.9 billion total) in 2025. Americans aged 60 and over lost $7.7 billion specifically in crypto-related fraud — a 60% jump year over year — with the average per-victim loss reaching $62,604.

These are not anomalies. This is the steady-state level of crypto-adjacent fraud in the United States.

The FBI's Operation Level Up has notified more than 8,000 victims and prevented over $500 million in additional losses since launch, but the program reaches a small fraction of total victims. The work of avoiding fraud falls mostly on the user.

The patterns repeat. If you can recognize the shape, you can avoid most of the loss.

- "Pig butchering" / romance scams. A stranger reaches out via text, dating app, or social DM. The conversation moves to a private channel. Eventually they introduce a "trading platform" they are using and offer to help you set it up. The platform is fake. Every dollar you deposit goes to them. If a recently-met online contact is teaching you to invest, you are inside the script.

- Anyone who asks for payment in crypto. Government agencies, employers, utility companies, courts, and the IRS do not accept crypto. They never will. A demand for payment in cryptocurrency is, on its own, sufficient to identify the contact as fraudulent.

- "Guaranteed returns." No legitimate investment guarantees returns. Especially not in crypto, where volatility is the defining feature of the asset class. Numerical "guarantees" are the marker of a Ponzi structure.

- Pressure to act fast. Real opportunities do not require you to skip diligence. "This window closes in 24 hours" is not a feature of legitimate investments; it is a feature of fraudulent ones.

- Unsolicited recovery services. If you have already been scammed, a second wave of scammers will contact you offering to "recover" your funds. They cannot. Pay them and you lose more.

- Fake support accounts. Every major exchange and wallet brand is impersonated on Telegram, Discord, X, and email. Real support never contacts you first, never asks for your seed phrase, never asks you to install screen-sharing software. Ever.

How much should a beginner actually allocate?

This is the section where I am required to say something that the persona of a hedge fund alumnus may make sound stronger than it should: I am not your financial advisor, and individual allocation is between you and a licensed one who knows your circumstances. With that on the record, here is what the consensus 2026 framing looks like, drawn from public guidance and not from any individual recommendation.

Most financial advisors who cover the asset class suggest capping crypto exposure at 1–5% of total portfolio value, and only investing money the holder can afford to lose entirely. The dominant 2026 frame inside that 1–5% sleeve is "core/satellite": roughly 70% in BTC and ETH (the two assets with the most established liquidity, longest track records, and clearest fundamentals), and roughly 30% in higher-variance positions if the holder wants exposure to more speculative names.

Dollar-cost averaging — buying a fixed dollar amount at a fixed cadence rather than trying to time a single entry — is the standard mechanic for someone building exposure for the first time. It removes the "did I buy at the top?" question from the process, which is the question that produces the worst beginner behavior.

Bitcoin directly vs spot Bitcoin ETF

A practical question that did not exist before January 2024: should you buy bitcoin on an exchange and hold it in your own wallet, or buy a spot Bitcoin ETF in your brokerage account?

Both give you bitcoin price exposure. They differ on three things.

- Custody. Direct ownership means you hold the keys. ETF ownership means BlackRock or Fidelity or one of the other issuers holds the bitcoin and you hold a share in the fund.

- Tax wrapper. ETFs sit inside ordinary brokerage and IRA accounts. Direct holdings do not — you cannot put self-custodied bitcoin into a Roth IRA without specialized custodians.

- Use. You cannot pay a counterparty in ETF shares. If you ever want to use bitcoin for payments, settle a transaction onchain, or tip into DeFi, you need direct holdings.

Beginners often start with an ETF and graduate to self-custody once they are comfortable with wallets. There is nothing wrong with that progression. There is also nothing wrong with stopping at the ETF.

Crypto and your taxes: Form 1099-DA

For tax year 2025, crypto brokers were required to issue Form 1099-DA reporting your gross proceeds from digital-asset transactions to both you and the IRS, with mailings completed by February 17, 2026. Cost-basis reporting begins with 2026 transactions, meaning the 1099-DA forms you will receive in early 2027 will include the basis your broker reported.

Three things every U.S. beginner should know about the new regime:

- The IRS receives a copy of every 1099-DA your broker sends you. If your tax return does not match what the broker reported, the IRS issues an automated CP2000 notice. This is a much higher detection rate than the "self-report and hope" environment that existed before 2025.

- The IRS treats cryptocurrency as property, not currency. Every sale, swap, or use to pay for something is a taxable event for capital-gains purposes. Buying bitcoin and holding it is not taxable. Swapping bitcoin for ether is.

- Cost-basis tracking across multiple exchanges is the part where mistakes are easiest to make. Crypto-tax software (CoinTracker, Koinly, others) ingests your exchange history and produces consolidated reports. For anyone with more than a handful of transactions per year, this is the practical answer.

I am not a tax professional. The detail above is a starting point, not a substitute for one.

The 2026 U.S. regulatory landscape

For roughly five years, the U.S. crypto industry operated under jurisdictional ambiguity: was a given token a security under the SEC's purview, a commodity under the CFTC's, or something else? Most of the enforcement actions of 2022–2024 turned on that question. As of 2026, FIT21 has settled it.

FIT21 sorts digital assets into three buckets:

- Digital Commodities — regulated by the CFTC. The category covers assets on networks that are "functional and decentralized" by the statutory definition. Bitcoin clearly fits. Ether plausibly fits.

- Restricted Digital Assets — regulated by the SEC. The category covers tokens issued under arrangements that look like investment contracts, especially during the early phase of a network's life when the issuer retains control.

- Permitted Payment Stablecoins — regulated separately under the GENIUS Act framework, neither securities nor commodities.

The practical effect for a beginner is that the legal status of the major assets is now legible. Bitcoin is a commodity. Stablecoins issued under the GENIUS framework are payment instruments. Most other tokens fall under one of the SEC categories until the network matures sufficiently to migrate to the CFTC bucket. That clarity does not make any specific token a good investment. It does mean the lawyers and compliance teams that previously waved off the asset class on legal-uncertainty grounds no longer have that excuse.

The OCC's April 2026 implementation proposal for GENIUS Act stablecoin issuers continues to formalize the federal pathway. State pathways exist for issuers under $10 billion in outstanding tokens. The shape of the U.S. stablecoin industry over the next 24 months will be determined by how aggressively issuers consolidate onto the federal vs state tracks.

Outside the United States, regulation is fragmented by jurisdiction and continues to evolve at a different pace. None of those frameworks are the focus of this guide.

What this guide does not tell you

In keeping with my own rule about disclosing the limits of any analysis, here is what I have not addressed and you should not infer.

- Whether to buy any of this. That is between you and a licensed financial advisor who knows your full circumstances. I have explained how the asset class is built and where the risks concentrate. I have not told you to allocate.

- Where the next cycle goes. I do not know. Anyone who claims to is either selling something or about to be wrong on the record.

- Which specific Layer 1 ecosystems beyond BTC and ETH end up with durable economic activity. That is an open empirical question. Five years from now we will know which protocols generated real fee revenue from real users at scale, and most of the speculation in 2026 will have been wrong about it.

- What happens if a major regulated U.S. stablecoin issuer fails. The GENIUS Act gives holders priority in insolvency, but the framework has not been stress-tested against an actual failure event. The next two years will tell us whether the protections work in practice.

What would have to change for me to update the picture above: a major spot ETF unwind that pulls institutional flows back out, a stablecoin holder loss event that proves the new framework's reserve protections were less robust than advertised, a regulatory rollback in a future Congress, or — on the upside — measurable enterprise stablecoin adoption inside U.S. commercial banking. I will be watching for all four, and you can too.

That is the cryptocurrency for beginners walkthrough as I would write it for a friend in 2026. The mechanics are learnable. The custody is learnable. The fraud patterns are learnable. The asset class itself is volatile, partially regulated, and in the middle of a structural transition from speculative-retail-only to retail-plus-institutional. Treat it accordingly.

Frequently Asked Questions

A blockchain is a database replicated across many independent computers that records transactions in append-only blocks linked by cryptographic hashes. Cryptocurrencies are tokens whose ownership and transfers are recorded on a blockchain. The two are inseparable: a cryptocurrency without a blockchain is just a database entry; a blockchain without a token is a private ledger most enterprises ended up not needing.

Bitcoin (a fixed-supply monetary asset), smart-contract platforms like Ethereum (which run programmable applications and earn fee revenue), stablecoins like USDC and USDT (pegged to $1 USD and increasingly the actual payment rail of crypto), DeFi tokens (governance tokens for specific protocols), and memecoins (speculation on attention). The distinction that matters is whether a given asset generates measurable economic activity or whether its price simply tracks bitcoin.

For any meaningful balance, use a hardware wallet (Ledger, Trezor, or similar) that holds your private keys offline. Write the recovery seed phrase on paper or stamp it into metal, store it in two physical locations you control, and never type, photograph, or share it digitally. Do not store more than active-trading amounts on a centralized exchange. Anyone claiming to be 'support' who asks for your seed phrase is fraudulent.

Most financial advisors suggest capping crypto exposure at 1-5% of your total portfolio and only investing money you can afford to lose. Many beginners use dollar-cost averaging — buying a fixed dollar amount weekly or monthly — to smooth out volatility. Most major U.S. exchanges allow fractional purchases starting at $1-$5. Individual circumstances vary; consult a licensed financial advisor for your situation.

Spot Bitcoin ETFs (BlackRock's IBIT, Fidelity's FBTC, Morgan Stanley's MSBT, and others, all launched after January 2024) provide bitcoin price exposure inside an ordinary brokerage or IRA account — simpler taxes, no wallets, and no custody risk. Direct ownership on an exchange or in a self-custodied wallet gives you actual control of the asset, the ability to use it onchain, and exposure outside the brokerage system. Beginners often start with an ETF and graduate to self-custody once comfortable with wallets.

Yes — Americans lost $11.4 billion to crypto scams in 2025, a 22% increase from 2024 (FBI Internet Crime Report). Crypto-linked fraud accounted for more than half of all U.S. internet crime losses. Top red flags: anyone asking for payment in crypto, 'guaranteed' returns, romance partners pushing you to invest, pressure to act fast, and unsolicited 'support' agents asking for seed phrases.

Yes. The IRS treats cryptocurrency as property. Selling, swapping, or spending crypto can trigger capital gains. Starting with the 2025 tax year, U.S. crypto brokers must issue Form 1099-DA reporting your gross proceeds, with cost-basis reporting beginning for 2026 transactions. The IRS receives a copy of every 1099-DA — mismatched returns trigger automated CP2000 notices.