Empowering Voices: Unleashing the Power of Diverse Perspectives in Finance

The most useful framing for diversity in finance in 2026 is the contradiction inside the data. McKinsey's 2023 Diversity Matters Even More report finds that top-quartile diverse firms are roughly 39% more likely to financially outperform bottom-quartile peers — a number that has gotten stronger across each successive McKinsey study since 2015. And yet over the same period, several of the largest US financial institutions — Goldman Sachs, BlackRock, Vanguard, State Street, Citigroup, JPMorgan — have rolled back or rebranded their formal DEI programs. The research is not moving in the direction the corporate decisions are moving. That gap is the story.

I want to walk through the actual numbers — workforce, leadership, pay, loan approval — and then through what the named institutions are doing right now in 2026, and finally through inclusive-investing vehicles that route capital independently of any single firm's HR posture. I am writing as an operator who has run a real business through the recent capital cycle. I do not have a stake in whether the language is "DEI" or "inclusion" or "cognitive diversity" — I care about whether the funding access at the decision points actually reflects the composition of the country.

The workforce and leadership gap, by the numbers

The single most consistent finding across every credible 2024-2026 source is that diversity in finance shows up at the entry-level and shrinks at every promotion gate. The current numbers.

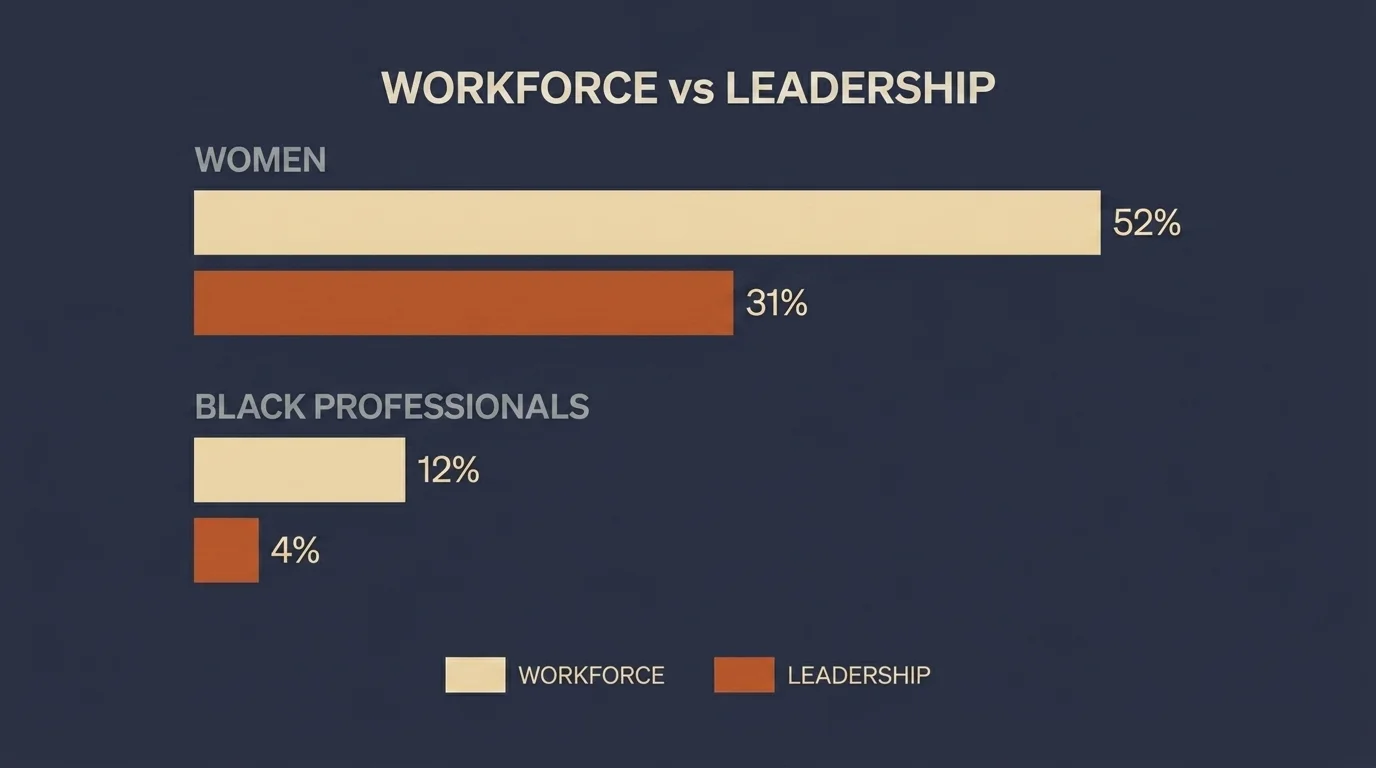

- Women: 52% of the US financial services workforce, but only 31% of senior leadership. Globally, women hold roughly 18% of financial services C-suite seats, and the commercial-bank C-suite specifically is around 19% women.

- Black professionals: roughly 12% of the US financial services workforce, but only 4–5% of senior roles. The gap widens sharply between mid-management and the executive committee.

- Adviser demographics (2023–2024): 72.1% White, 9.5% Hispanic/Latinx, 8.3% Asian, 5.6% Black/African American, 0.1% American Indian; 72.3% male, 27.7% female. The adviser bench is materially less diverse than either the underlying workforce or the client base it serves.

- UK pay gap: up to 27.2% in finance. The US gap is narrower but persistent, particularly at the partner and managing-director tiers.

The pattern in those four bullet points is the same pattern in every internal HR data set I have ever seen at a bank or financial-services firm. The entry-level cohort is reasonably representative. The leadership cohort is not. And the gap between them is mostly built between the senior-associate and the managing-director promotion gates — which is where the firm's discretionary HR processes do the most work.

The federal data confirms this picture. The GAO 2023 report (GAO-23-106427) on representation of minorities and women in financial services is the canonical reference, alongside the EEOC's parallel work. Neither agency reports a story materially different from the private-sector data above.

The business case for diversity in finance

The business case for diversity in finance is unusually well-quantified for a topic this loaded politically. McKinsey's 2023 work puts the financial-performance gap at ~39% between top-quartile and bottom-quartile diverse executive teams. CFP Board research finds companies with greater racial diversity earn roughly 15% more revenue than low-diversity peers. And the client-preference data has shifted sharply: 30% of investors preferred a diverse advisory team in 2019, rising to 58% by 2021. By 2030, affluent multicultural households in the US are projected to reach 20 million.

For an operator, the relevant question is not whether the business case is real — it is. The relevant question is whether the firms acting on the business case are the firms making the most durable decisions. I will come back to that.

From workforce to capital flow

The conversation about diversity in finance often stops at hiring. It should not. The more consequential question is where the capital goes.

The cleanest single number to anchor this on is the loan-approval disparity by applicant race in US mortgage and small-business lending: approximately 35% White / 19% Hispanic / 16% Black / 15% Asian. The gap is not a single year's data point. It is a multi-decade pattern that survives controls for credit score, income, and loan size. Capital deployment is itself a diversity variable, and one that affects which businesses get built, which households compound, and which communities have working capital.

For founders, the implication is operational. If you are a founder from an underrepresented background going to a traditional bank for SBA 7(a) capital, you are starting the conversation from inside a documented disparity. The defenses are the same ones I would recommend to any founder — clean books, a credible plan, a banker who has worked with founders like you — but the structural friction is real and is part of the picture I write about capital-stack design.

The other side of capital flow is investment allocation, which is where the inclusive-investing vehicles below come in.

Inclusive investing: the vehicles, not the slogans

A specific gap in nearly every other article on this topic is the failure to name the actual investment vehicles. If you want capital to flow toward underrepresented founders, communities, or issuers — independently of any single firm's HR posture — the vehicles below are the ones you actually hold.

- Impact Shares NAACP Minority Empowerment ETF (NACP) — tracks the Morningstar Minority Empowerment Index; built in collaboration with the NAACP.

- SPDR SSGA Gender Diversity Index ETF (SHE) — large-cap US companies with leadership reflecting gender-diversity criteria.

- Adasina Social Justice Capital ETF (JSTC) — broader social-justice screen across racial, gender, climate, and labor criteria; developed with grassroots-organization input.

- Impact Shares YWCA Women's Empowerment ETF (WOMN) — US large-caps weighted by women's-empowerment criteria.

- Calvert US Large-Cap Diversity Research Fund (CDHIX) — actively managed strategy with diversity-and-inclusion criteria baked into the security-selection process.

A few operator notes on this list. These vehicles are not all the same product. The ETFs differ on what they screen for, what they exclude, how concentrated the resulting portfolio is, and how the expense ratio compares to a broad-market index. They are also publicly traded, so the prices move with the market and you can lose money in them the same way you can lose money in any equity exposure. Before allocating, read the prospectus and the index methodology — and confirm with a licensed advisor that the position fits your overall asset allocation.

The reason to name these vehicles specifically is that "inclusive investing" as a concept gets discussed in language so abstract that readers walk away without anything they can actually buy. The point of this section is to close that gap. None of this is a recommendation of any individual vehicle. It is the inventory of what exists.

Diversity programs at the top US banks

A second specific gap in the existing literature is the failure to name actual bank programs. The list below covers the most established programs in 2026.

- JPMorgan Advancing Black Pathways — multi-program initiative covering education, workforce, and entrepreneurship pathways for Black professionals and businesses.

- Goldman Sachs Possibilities Summit + One Million Black Women — recruitment summit (Possibilities) plus a $10 billion ten-year capital commitment to Black women in the US.

- Bank of America Sophomore Diversity Program — early-pipeline program for second-year college students from underrepresented backgrounds.

- Morgan Stanley Richard B. Fisher Scholarship — scholarship and summer internship for high-performing Black, Hispanic/Latinx, and Native American undergraduates.

- Citi HBCU Innovation Lab — partnership program with Historically Black Colleges and Universities focused on fintech and innovation skill-building.

- Blackstone Future Women Leaders — pipeline program for first-year college women interested in investment careers.

These are not all "DEI" by every firm's current internal language. Several have been re-scoped or rebranded as the corporate posture has shifted. The programs themselves continue to operate in some form, with different names, application windows, and selection criteria from the pre-2023 versions. Anyone looking to apply should check the current details directly with the firm.

Where DEI in finance actually stands in 2026

The political and regulatory context has changed enough since 2023 that any honest treatment of this topic has to name what has happened.

Goldman Sachs dropped its formal board-diversity rule in 2023, after the SCOTUS Students for Fair Admissions decision changed the legal posture around explicit diversity criteria in private institutions.

BlackRock and Vanguard — the two largest index-fund managers in the US — removed traditional board-diversity requirements from their proxy-voting guidelines through 2024. The position is now framed as "we do not require, we evaluate", a meaningful shift in the practical effect on the underlying companies.

State Street dropped its 30%-women-directors voting criterion at the end of February 2025. State Street had been one of the most consistent voices on this issue for nearly a decade; the change was significant.

Citigroup retired its formal DEI initiatives at the end of February 2025, restructuring the function into the broader HR organization.

JPMorgan merged its DEI function into HR in 2025 under the rebranded "Diverse Experience, Equity & Inclusion" framing. Bloomberg's February 2026 reporting describes measurable career impact on Black bankers at both JPMorgan and Citi from the corporate-posture change.

Across the industry, three established UK-origin DEI groups merged and rebranded as "Inclusion in Finance" in 2026, explicitly pivoting toward cognitive-diversity framing as a politically less charged way to maintain the underlying work. That rebrand is the cleanest signal of where industry messaging is going.

A direct observation. None of the rollbacks above have been justified by new research showing the diversity-performance correlation has weakened. The McKinsey, CFP Board, and federal data still point the same direction they did in 2018. The corporate decisions are being driven by political and legal pressure, not by new contrary evidence. Whether that pressure persists into the next regulatory cycle is the open question — and whether the underlying programs operate effectively under different names is the question that actually determines outcomes.

An operator's read

I want to close with an operator's lens, because that is the lens I have, and because most of the writing on diversity in finance is missing it.

The numbers above describe a system in which the entry-level pipeline is broadly representative, the leadership pipeline is not, the firms know this, the research supports acting on it, and the political environment has made acting on it harder. From inside a real business, what you watch is whether the operational behavior of the institutions you depend on — your bank, your investor base, your underwriter, your custodian — actually changes with the rhetoric. Sometimes it does. Often the program survives the renaming. Sometimes the renaming is the program ending.

For founders from underrepresented backgrounds, the practical advice has not changed. Banker relationships matter more than logos. SBA pre-qualification matters. A clean cap table matters. Capital that flows independently of any single bank's HR posture — angels with patient capital, regional CDFIs, equity crowdfunding from an audience that already trusts you — matters more in 2026 than it did in 2020. Build a stack that is structurally diversified across funders, because the individual funder's posture can change overnight.

For investors who want their capital to reflect their values on this, the inclusive-investing ETFs above are the named vehicles. They are not a substitute for due diligence on the underlying methodology, and they should fit inside a broader asset allocation rather than being the whole portfolio. Talk to a licensed advisor before allocating any of this.

For HR leaders inside financial services firms, the operational reality is that the work that compounds is the boring infrastructure work — promotion criteria written down and applied consistently, mentorship networks that survive a single sponsor's exit, compensation reviews with the data on the table. Whatever the program is called this year, the underlying mechanics either work or they do not. The data shows up at the next promotion cycle.

None of this is individual financial or business advice. For the financial questions, talk to a licensed advisor who can see your specific situation. For the operational questions — funding stack, banker relationships, capital allocation — talk to an operator who has been through a cycle, ideally one who has been through a cycle in your specific sector. The structural picture in this article is the starting point of those conversations, not the substitute for them.

Frequently Asked Questions

Women hold approximately 31% of US financial services senior leadership against 52% of the underlying workforce, and Black professionals hold 4-5% of senior roles against roughly 12% of the workforce. The gap widens sharply at every promotion gate. Through 2024-2025, several major banks — Goldman Sachs, BlackRock, Vanguard, State Street, Citigroup, and JPMorgan — rolled back or rebranded their formal DEI commitments, even as the underlying performance research continued to support the business case.

Yes — the research is consistent. McKinsey's 2023 Diversity Matters Even More report finds top-quartile diverse firms are approximately 39% more likely to financially outperform bottom-quartile peers. CFP Board research shows companies with greater racial diversity earn roughly 15% more revenue than low-diversity peers. The performance correlation has gotten stronger across each successive McKinsey study since 2015, not weaker — which is why the 2024-2026 rollbacks are notable: they are being driven by political and legal pressure, not by new contrary evidence.

Inclusive investing routes capital toward underrepresented founders, communities, and issuers via specific investment vehicles — separately from how any individual firm staffs its workforce. Named US ETFs include Impact Shares NAACP Minority Empowerment ETF (NACP), SPDR SSGA Gender Diversity Index ETF (SHE), Adasina Social Justice Capital ETF (JSTC), Impact Shares YWCA Women's Empowerment ETF (WOMN), and the actively managed Calvert US Large-Cap Diversity Research Fund (CDHIX). Each uses different screening methodology, so check the prospectus before allocating.

JPMorgan (Advancing Black Pathways), Goldman Sachs (Possibilities Summit and the One Million Black Women commitment), Bank of America (Sophomore Diversity Program), Morgan Stanley (Richard B. Fisher Scholarship), Citi (HBCU Innovation Lab), and Blackstone (Future Women Leaders) are among the most established. Several have been re-scoped or rebranded since 2023 — the programs themselves continue to operate in some form with different names, application windows, and criteria from the pre-2023 versions, so check the current details directly with the firm.

The rollback is being driven by political and legal pressure following the 2023 SCOTUS Students for Fair Admissions decision and renewed federal scrutiny of corporate diversity programs, not by new contrary research. McKinsey, CFP Board, GAO, and EEOC data all still support the business case for diversity in finance. Whether the underlying programs operate effectively under their new names is the question that actually determines outcomes; the rebranding to 'cognitive diversity' or 'inclusion in finance' is a politically less charged framing for substantively similar work.

Women are approximately 52% of the US financial services workforce but only 31% of senior leadership; Black professionals are roughly 12% of the workforce but only 4-5% of senior roles. Globally, women hold approximately 18% of financial services C-suite seats. The gap widens at every promotion gate — most of the divergence is built between the senior-associate and managing-director tiers, where the firm's discretionary HR processes do the most work. The federal GAO and EEOC data confirm the same pattern in their reports on representation in financial services.