Behavioral Finance: Unveiling the Psychology of Investment Decisions

Behavioral finance starts here: the 2024 behavior gap, depending on which methodology you trust, was either 848 basis points (DALBAR) or 122 basis points annualized over 10 years (Morningstar) — and that range itself is part of the story. Either way, average equity-fund investors in 2024 earned 16.54% against an S&P 500 that returned 25.02%; the Guess Right Ratio fell to 25%, tied for an all-time low; and a $100,000 buy-and-forget S&P position over the past 20 years grew to roughly $717,000, while the average investor's same starting capital ended at about $345,000. Morningstar's Mind the Gap 2025 puts the 10-year annualized gap at 122 basis points, roughly 15% of total potential return forfeited. A 2024 SSRN working paper from Fulkerson, Jordan, Riley, and Yan argues the headline magnitude is methodology-dependent — which is the honest framing this article will take throughout. The direction is consistent across methodologies; the precise magnitude is contested. Either way, the question is why intelligent people with access to the same low-cost index funds underperform them so reliably, over multi-decade horizons, in such measurable amounts.

The answer is behavioral finance: the field that takes seriously the psychological mechanics that corrupt valuation discipline. The rest of this article is the bias library, the live case studies showing the biases at work in the current cycle, the mitigation tactics that survive contact with a real portfolio, and a short self-diagnostic. The honest valuation question is not "how does psychology affect investing in the abstract" — that's the marketing question. The honest question is: which specific biases are costing me basis points right now, and what is the disciplined practice that counters each one?

Behavioral Finance vs Traditional Finance

The textbook frame against which behavioral finance defined itself is the Efficient Markets Hypothesis and the Markowitz/Sharpe portfolio-theoretic tradition that assumes investors are rational, well-informed, and unbiased. The behavioral tradition (Kahneman, Tversky, Thaler, Shiller) starts from the documented fact that they are none of those things — and rebuilds the framework around the systematic ways they fail.

| Dimension | Traditional Finance | Behavioral Finance |

|---|---|---|

| Assumption about investors | Rational, unbiased, utility-maximizing | Boundedly rational, systematically biased |

| Anchor theorists | Markowitz, Sharpe, Fama | Kahneman, Tversky, Thaler, Shiller |

| Key model | Modern Portfolio Theory; CAPM; EMH | Prospect Theory; mental accounting; herding models |

| Market view | Prices reflect all available information | Prices reflect information plus systematic biases |

| Evidence base | Cross-sectional return regressions; factor models | Lab experiments; meta-analyses; behavior-gap field data |

| Prescription | Diversify; index; minimize fees | Above + behavioral guardrails (rules, automation, structure) |

The disciplined investor's position is not that one tradition is right and the other is wrong. It's that traditional finance gives you the target portfolio (diversified, low-cost, allocation matched to time horizon) and behavioral finance explains why you keep failing to hold it. Both halves are required.

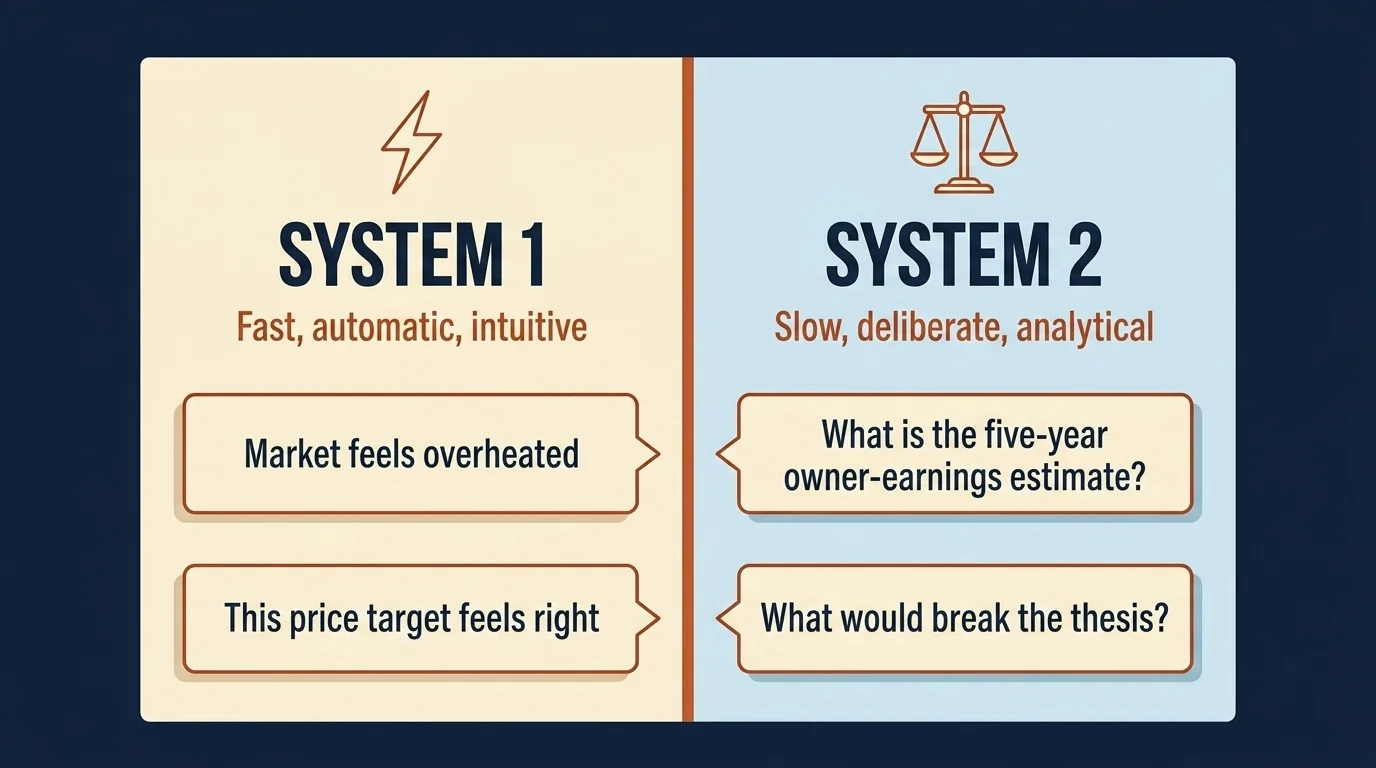

Kahneman's System 1 and System 2

Daniel Kahneman's Thinking, Fast and Slow (2011) — the canonical lay introduction to the field, anchored in the 1979 Prospect Theory work for which he and Tversky earned the 2002 Nobel Memorial Prize in Economic Sciences — frames the entire conversation in two cognitive systems:

- System 1: fast, automatic, intuitive. The mental machinery that recognizes faces, completes idiomatic sentences, and tells you the market is "overheated" based on a feeling rather than a metric.

- System 2: slow, deliberate, effortful. The machinery that runs a discounted cash-flow model, reads a 10-K, or thinks through whether a position's drawdown actually invalidates the thesis.

Almost every behavioral bias in the rest of this article is, mechanically, an instance of System 1 producing a fast answer that System 2 fails to interrogate before action is taken. The mitigation tactics later in the article (Investment Policy Statements, pre-mortems, cooling-off periods, automated rebalancing) are not magic. They are simply structural devices to force decisions out of System 1 and into System 2, where the math has a chance to win.

The Investor Bias Library

The biases below are the ones with the highest dollar consequence for retail allocators in 2026. Each follows the same template: definition, mechanism, an investing example, and the specific mitigation tactic that counters it.

Loss Aversion (Emotional)

Definition. Losses hurt more than equivalent gains feel good. The asymmetry distorts decisions toward avoiding realized losses rather than maximizing expected return.

Mechanism. Kahneman & Tversky's 1979 Prospect Theory paper put the loss-aversion coefficient (λ) at roughly 2.25 — losses were estimated to weigh about 2.25x more than equivalent gains. Two 2024 meta-analyses now contest the magnitude: Brown, Imai, Vieider & Camerer (2024), pooling 607 estimates across 150 studies, landed at λ ≈ 1.96; Walasek, Mullett & Stewart (2024) re-modeled 17 studies and got λ ≈ 1.31, dropping to ~1.07 under symmetric-stakes designs. Translation for the practitioner: losses still hurt more, but the "2x rule of thumb" is closer to 1.3x–2x depending on stakes and study design.

Investing example. Holding a losing position because selling would "lock in the loss" — even when the disciplined valuation question (would I buy this position today at its current price?) returns a clear no.

Mitigation. Pre-define kill criteria before every buy. Write down the specific conditions (impairment of incremental ROIC, change in capital allocation, thesis-breaking news) under which you will sell. When those conditions trigger, sell — independent of P&L.

Related Article: Finance Mentor vs Sponsor: What Actually Compounds a Career

Confirmation Bias (Cognitive)

Definition. The tendency to seek out, weight, and remember information that supports an existing belief while discounting contradicting evidence.

Mechanism. This is the bias that turns a thesis into an identity. Once a position is established, the brain pattern-matches favorably toward news that supports it and dismisses news that should update the prior.

Investing example. Increasing position size in a holding after good news, while explaining away three pieces of bad news as "noise" or "temporary."

Mitigation. Pre-mortem: before initiating a position, write a one-page memo describing how this investment fails. Re-read the memo every time you consider adding to the position. The discipline forces the contradicting evidence into your active consideration.

Anchoring Bias (Cognitive)

Definition. The tendency to over-weight the first piece of numerical information encountered ("the anchor") when forming subsequent judgments.

Mechanism. Anchors do not need to be relevant to be influential. Experimental subjects asked to estimate a quantity after being shown an unrelated number reliably bias toward it.

Investing example. Anchoring on cost basis. A position bought at $150 still trading at $90 is not "down 40%" in any forward-looking sense; it is a position whose current price is $90 and whose forward expected return depends on what the business is worth, not on what you paid. The cost basis is an accounting artifact, not an analytical input.

Mitigation. Each portfolio review, ask the cost-basis-free question: would I buy this position today at today's price? If no, sell. If yes, you can hold or add. P&L is not in the question.

Related Article: Youth-Led Financial Revolutions: Crowdsourcing as a Catalyst for Investment Innovation

Recency Bias (Cognitive)

Definition. Over-weighting recent events and extrapolating them forward.

Mechanism. The brain treats salient, recent data as more representative of the underlying distribution than the long-run statistics warrant. In markets, this manifests as expecting last year's winners to keep winning.

Investing example. The 2024 AI-mania trade. Investors extrapolated the 2023 returns of a handful of large-cap technology names into forward expectations of the same magnitude, and re-weighted portfolios accordingly. The forward math required to justify the resulting valuations — high incremental ROIC sustained for a decade against rising capital intensity — was rarely written down explicitly because System 1 had already decided.

Mitigation. Rebalance on a schedule, not on a feeling. Mechanical quarterly or annual rebalancing forces selling of recent winners and buying of recent losers — exactly the trade recency bias resists.

Overconfidence Bias (Cognitive)

Definition. Systematic overestimation of one's own analytical ability, judgment quality, or knowledge precision.

Mechanism. Overconfidence shows up most clearly as over-trading. The investor who is "sure" about a series of stock picks generates a transaction-cost drag that compounds over time.

Investing example. Barber and Odean's landmark 2001 study "Boys Will Be Boys" in the Quarterly Journal of Economics, covering 37,664 households at a large discount broker from 1991–1997, found that men traded 45% more than women. Over-trading reduced their net annual returns by 2.65 percentage points versus 1.72 percentage points for women — a 93 basis point per year overconfidence cost. The mechanism was not stock-picking skill; it was the volume of decisions.

Mitigation. Trade less. Run a quarterly review, not a daily review. Track every transaction in a journal with the reason for it; review the log annually for patterns.

Herd Mentality (Emotional/Social)

Definition. The tendency to follow group behavior, especially under uncertainty, regardless of independent analysis.

Mechanism. Herd behavior is rational at the individual level (the crowd often has information the individual lacks) and pathological at the system level (the crowd can be wrong en masse).

Investing example. GameStop in January 2021. Tens of millions of retail accounts bid the same handful of names into nine-figure valuations against the underlying business economics, in a coordinated social-proof cascade. Better Markets' 2026 retrospective notes the meme-stock playbook has since migrated to crypto, prediction markets, and 24/7 trading — same mechanics, broader surface area.

Mitigation. Write your Investment Policy Statement before market events, and check decisions against it during them. The IPS is the precommitment device.

Sunk Cost Fallacy and the Disposition Effect (Cognitive/Emotional)

Definition. The tendency to factor irrecoverable past costs into forward decisions. The disposition effect is the investing-specific manifestation: selling winners too early and holding losers too long.

Mechanism. Coined by Hersh Shefrin and Meir Statman in 1985, the disposition effect is loss aversion plus anchoring plus mental accounting working in concert. The investor refuses to realize the loss because doing so converts a "paper" position into a "confirmed mistake."

Investing example. You sold AAPL at +20% (to "take profits") but you're still holding a battered EV name at -60% from cost. The math says the EV position should be evaluated on forward return, not on its drawdown; the bias says don't realize the loss.

Mitigation. Same as anchoring — the cost-basis-free question. Combined with quarterly tax-loss harvesting that converts the disposition trap into a realized tax benefit, which structurally disarms the emotional cost.

Mental Accounting (Cognitive)

Definition. Treating money differently depending on its source or intended use, even though all money is fungible.

Mechanism. Thaler's contribution to the field. Investors carve their wealth into mental buckets — "rainy day," "fun money," "kids' college" — and apply different risk tolerances to each. The bucket boundaries are psychologically real and economically arbitrary.

Investing example. Treating a tax refund or a year-end bonus as "windfall" money and investing it more aggressively than the same dollars accumulated through payroll. Or holding a high-fee actively-managed mutual fund in a taxable account while paying down 4% mortgage debt — the spread is negative net of fees and tax, but the accounts feel separate.

Mitigation. Run a household-wide net-worth statement quarterly. Treat every dollar as equally yours, regardless of which account it lives in.

Availability Heuristic (Cognitive)

Definition. Judging the probability of an event by how easily examples come to mind.

Mechanism. Salient, recent, vivid examples bias probability estimates upward. The 2020 COVID drawdown is more available than the 2009–2019 bull market, so risk feels larger than it is.

Investing example. Holding excess cash for years after a market shock because the drawdown is mentally available, while compounding opportunity quietly disappears.

Mitigation. Use base rates. The historical equity drawdown distribution is published and accessible — work from the data, not the most recent vivid memory.

Related Article: Sustainable Investing: Aligning Values with Financial Goals

FOMO / Social Proof (Emotional)

Definition. Fear of missing out — the discomfort of seeing peers or markets pursue gains you are not part of.

Mechanism. FOMO is herd mentality with a phone in your hand. Push notifications, group chats, and gamified feeds compress the time between feeling the bias and acting on it from days to seconds.

Investing example. Buying into a parabolic move two weeks into the second leg up, on the strength of social-feed evidence rather than analytical evidence.

Mitigation. A 48–72 hour cooling-off period before any unplanned trade larger than 1% of portfolio. Combined with the IPS, the cooling-off period almost completely disarms the FOMO impulse.

What the Fear & Greed Index Actually Measures (and Where It Fails)

The CNN Fear & Greed Index aggregates seven market-sentiment inputs into a single 0–100 score: S&P 500 momentum relative to its 125-day moving average; the count of 52-week highs vs lows; advancing vs declining volume; put/call ratio; the VIX; safe-haven demand (20-day stock-vs-bond returns); and junk-bond demand. Readings below 20 are "extreme fear"; above 80 is "extreme greed."

What the Index actually measures is the level of fear or greed implicit in current market positioning. That is a useful contrarian signal when readings are at extremes: extreme-fear readings historically clustered around major bottoms (March 2020 COVID low; October 2022); extreme-greed readings clustered around late-stage rally peaks (November 2021 crypto top). What it does not measure is the future direction of prices — the Index lags during sustained trends, can stay at extremes for months, and is structurally less useful in 24/7 crypto markets where sentiment is manipulable.

The disciplined use is as a precommitment check. Define in your IPS: if the Index reads below 25, I will rebalance toward equities by X%; if it reads above 75, I will trim equities back to target. The Index then becomes a behavioral guardrail — not a buy/sell trigger, but a forcing mechanism that converts a System 1 impulse ("I'm scared, sell everything") into a System 2 decision ("the IPS says rebalance toward, not away").

Live Case Studies: GameStop, FTX, AI-Mania, Mag-7

The academic literature stops its case studies at the 1999 dotcom bubble and the 2008 housing collapse. The four cases below are the current-cycle reality of behavioral biases at work.

GameStop, January 2021 — herd + social proof. Coordinated retail buying through r/wallstreetbets drove a stock with mid-single-digit earnings power to nine-figure valuations against a fundamentally unchanged business. The mechanism was social proof at scale; the casualties were the late-entrant retail buyers who provided exit liquidity to the earlier participants. Better Markets' 2026 retrospective documents the playbook migrating into crypto, prediction markets, and 24/7 trading apps — the same mechanics, now operating across a broader surface area.

FTX, November 2022 — overconfidence + halo effect. A celebrity-endorsed exchange custodied tens of billions in customer assets with no functional separation between exchange and proprietary trading. Investors and depositors anchored on the founder's public profile, the institutional partnerships, and the visible asset-management AUM as evidence of competence and integrity. None of those signals tested the actual question — was customer money segregated from the trading book — and the bias against asking is what made the unwind so total.

AI-mania, 2024 — recency + extrapolation. Following the 2023 returns of a small set of large-cap technology names, capital flowed into the same names at successively higher multiples on the assumption that recent returns extrapolated forward. The forward math required to justify the resulting valuations — incremental ROIC sustained at unprecedented levels against rising capital intensity from compute investment — was rarely written down explicitly.

Mag-7 concentration and de-crowding, 2024–2025 — familiarity + herd. By early 2025 the Magnificent Seven traded at a forward P/E of ~45x versus ~19x for the other 493 S&P names. Net hedge-fund exposure peaked at 21% in June 2024 and drifted to 15.5% by January 2025; in late April 2025, Morgan Stanley's prime brokerage reported that 60% of every gross dollar of hedge-fund selling over a five-day window was in Mag-7 names. The concentration was familiarity bias — the names everyone knew, in the country everyone invested from. The de-crowding, when it came, was herd behavior firing in the opposite direction. Both directions of the trade were behavioral; the underlying businesses changed less in those windows than the positioning did.

How Modern Trading Apps Amplify Bias

The 2020s introduced a structural amplifier to nearly every bias above: feed-driven trading apps designed around engagement metrics that mirror social-media product design. A 2024 Management Science study found Robinhood's "Top Movers" tab steers user attention toward extreme-return stocks, leading directly to portfolio underperformance — a textbook recency-bias amplifier built into the default UI.

In January 2024 the Massachusetts Securities Division fined Robinhood approximately $7.5 million for gamified features (confetti animations, lottery-style stock rewards, push notifications) that "trivialized investing and nudged customers toward frequent trades." Robinhood removed the contested features as part of the settlement; by April 2025 the firm had 25.9 million funded accounts. The settlement is notable not because it changed retail behavior — it did not, materially — but because it documented the regulatory recognition that UX design choices can be bias-amplification mechanisms in ways that matter at scale.

The practical implication for the disciplined investor is to engineer your trading environment for fewer decisions, not more. Notifications off. Portfolio app reviewed on a schedule, not on a feeling. Order tickets that require a written reason before submission. The architectural changes are doing exactly what the gamified apps are doing — using interface design to push behavior — only in the disciplined direction.

Related Article: Impact of Inflation on Investment Strategies

Mitigation Tactics × Biases

The matrix below lists the practical behavioral guardrails that work in a real portfolio, crossed against the biases each one counters. None of them require unusual willpower; all of them work by moving the decision out of System 1.

| Tactic | Counters |

|---|---|

| Investment Policy Statement (IPS) | Herd mentality, FOMO, recency, loss aversion |

| Pre-mortem before every buy | Confirmation bias, overconfidence |

| Kill criteria written before purchase | Loss aversion, disposition effect, sunk cost |

| Automated DCA contributions | FOMO, recency, market-timing impulse |

| Mechanical rebalancing (calendar or band) | Recency, herd, anchoring (on cost basis) |

| 48–72 hour cooling-off period before unplanned trades > 1% portfolio | FOMO, herd, availability |

| Decision journal (every trade + reason logged) | Overconfidence, confirmation, narrative fallacy |

| Quarterly tax-loss harvesting | Disposition effect, sunk cost |

| Notifications off; portfolio review on schedule | Recency, gamification-driven availability |

| Accountability partner or fiduciary advisor | All of the above (external check) |

The right way to read this table is which two or three tactics you will actually use, not all of them. Discipline that exists on paper but isn't practiced is just self-deception in writing. Pick the smallest set that genuinely changes your behavior and add to it slowly.

Self-Diagnostic Checklist

Answer the questions below honestly. Each "yes" maps to one or more biases above and indicates which mitigation tactic to install first.

- Have you held a losing position for more than six months because selling would "lock in the loss"? (Disposition effect, loss aversion, sunk cost — install kill criteria + cost-basis-free question.)

- Did you increase technology-sector exposure after the 2024 AI rally specifically because of the recent returns? (Recency, herd — install mechanical rebalancing.)

- Do you check your portfolio more than once a day during volatile weeks? (Loss aversion, myopic loss aversion, availability — install scheduled-review discipline, notifications off.)

- Have you ever sold a position to "take profits" while simultaneously holding a larger position with worse forward prospects? (Disposition effect, mental accounting — install the cost-basis-free question.)

- Do you read more news that supports your current portfolio thesis than news that challenges it? (Confirmation bias — install pre-mortem practice.)

- Did you change your asset allocation more than once in the past 12 months in response to market conditions? (Herd, recency, overconfidence — install IPS with explicit rebalancing triggers.)

- Do you treat a tax refund, bonus, or other "windfall" differently from your regular contributions? (Mental accounting — install household-wide net worth statement.)

- Do you find yourself reluctant to make a decision your IPS calls for because the market "feels different right now"? (Recency, narrative fallacy — install the discipline of acting on the IPS regardless of feeling.)

Three or more yeses is normal; eight is a flashing yellow light. The point of the diagnostic is not to grade you; it's to make the cost of inaction visible.

Recommended Reading

The literature on this topic is unusually high quality for a popular field. The four books worth reading first:

- Daniel Kahneman, Thinking, Fast and Slow — the System 1 / System 2 framework underneath the entire field.

- Richard Thaler, Misbehaving — the autobiographical account of how mental accounting and choice architecture became respectable economics.

- Robert Shiller, Irrational Exuberance — bubbles as a recurring feature, not an anomaly.

- Morgan Housel, The Psychology of Money — the contemporary popular synthesis; not academic but unusually well-written.

The path through these books in order builds the intellectual foundation faster than any single piece of online content can.

What Would Change My Mind on Behavioral Finance

The thesis of this article is that biases are the dominant explanation for the documented gap between investor returns and the returns of the funds those investors own. What would change my mind on that thesis? One thing, specifically: a meta-analysis finding that the behavior gap reduces to near zero once methodology is properly controlled, and that the controlled estimate is consistent across multiple independent datasets. The Fulkerson et al. 2024 SSRN paper and the Kitces-hosted DALBAR critiques push in that direction, and the loss-aversion λ debate shows the field is genuinely refining the magnitude of its central claims rather than rehearsing them. But the direction of the behavior gap — investors underperforming the funds they own — has held up across DALBAR's 30-year QAIB series and Morningstar's 10-year Mind the Gap series under different methodologies. Two consecutive decades of behavior-gap data showing the gap genuinely closing would tell me something structural has changed (better investor tools, better default behavior, better automation). I haven't seen it yet.

Until that data prints, the right answer for an individual allocator is to install two or three of the mitigation tactics above, write a short Investment Policy Statement, and stop checking the portfolio more than the schedule allows. The math on what that practice is worth, compounded over a 20-year horizon, is the answer to why this field exists.

If you want the trader/decision-process angle on behavioral finance — how to build a behavioral playbook for an active portfolio with sizing rules, journal templates, and a more aggressive treatment of FOMO and emotional discipline — read the companion piece, The Art of Behavioral Finance: Decoding Investor Psychology and Decision-Making, which covers exactly that ground.

This article is for educational purposes and is not individual financial advice. Behavioral patterns vary by individual, market regime, and account context. Consult a licensed financial advisor for guidance on your specific situation, and read each fund's prospectus before allocating capital. The studies cited above represent the current state of the field; effect sizes and methodologies remain under active academic debate, as noted throughout.

Frequently Asked Questions

The behavior gap is the shortfall between fund returns and the returns the average fund investor actually earns — driven by ill-timed buying and selling. DALBAR's 2025 QAIB report (covering 2024) put it at 848 basis points for equity-fund investors that year and roughly 120 bp annualized over 20 years; Morningstar's Mind the Gap 2025 reports 122 bp annualized over the 10 years ending December 2024. Academic critiques (Fulkerson et al., 2024 SSRN) argue the methodology overstates the gap, but the direction is consistent: investor behavior costs real money.

Loss aversion is the tendency to feel the pain of a loss more strongly than the pleasure of an equivalent gain. Kahneman and Tversky's original 1992 estimate put the ratio at about 2.25 to 1, but two 2024 meta-analyses landed at 1.96 (Brown et al., 607 estimates across 150 studies) and 1.31 (Walasek et al., re-modeled across 17 studies). For investors it shows up as holding losing positions too long (because selling 'locks in the loss') and selling winners too early.

Behavioral biases typically split into four families: Self-Deception (overconfidence, illusion of control, hindsight bias), Heuristic Simplification (anchoring, framing, representativeness), Emotion (loss aversion, regret, fear and greed), and Social Influence (herd mentality, social proof). A simpler practitioner split: cognitive (information-processing errors) vs emotional (feeling-driven decisions).

It's useful, not predictive. The Index aggregates 7 market-sentiment inputs (S&P 500 momentum vs 125-day MA, 52-week highs/lows, advancing/declining volume, put/call ratio, VIX, safe-haven demand, junk-bond demand) into a 0–100 score; readings below 20 (extreme fear) historically aligned with major bottoms like March 2020, and readings above 80 (extreme greed) flagged late-stage rallies like November 2021. It lags during sustained trends and is less useful in 24/7 crypto markets, so disciplined investors treat it as a 'check yourself before you act' signal — not a buy/sell trigger.

Coined by Hersh Shefrin and Meir Statman in 1985, the disposition effect is the tendency to sell winners too early and hold losers too long — both driven by loss aversion. Worked example: you bought AAPL at $150 and sold at $180 (locking in a small win to 'take profits'), but you're still holding an EV name at -60% from your cost basis because 'I don't want to realize the loss.' The right answer ignores cost basis entirely and asks 'given today's price, would I buy this position now?' If no, it's a sell — regardless of P&L.

A 2024 Management Science study found Robinhood's 'Top Movers' tab steers attention toward extreme-return stocks, leading to portfolio underperformance — a textbook recency-bias amplifier. In January 2024, Massachusetts Securities Division fined Robinhood about $7.5 million for gamified features (confetti animations, lottery-style stock rewards, push notifications) that 'trivialized investing and nudged customers toward frequent trades'; Robinhood removed the contested features as part of the settlement. The same mechanics have since migrated into crypto, prediction markets, and 24/7 trading platforms.

In Barber & Odean's landmark 2001 study ('Boys Will Be Boys', Quarterly Journal of Economics) of 37,664 households at a large discount broker from 1991–1997, men traded 45% more than women — driven by overconfidence — and over-trading reduced their net annual returns by 2.65 percentage points versus 1.72 percentage points for women, a 93 bp/year overconfidence cost. The finding is one of the most-cited behavioral-finance results in retail-investor research.

Behavioral economics is the broader field (Thaler, Kahneman, Tversky) studying how psychology shapes economic decision-making across consumption, saving, public policy, and labor. Behavioral finance is the subset that applies those insights to financial markets — asset pricing, investor behavior, market anomalies — anchored by Shiller's Irrational Exuberance and Thaler's 2017 Nobel work. Practically: same toolkit, narrower target.

The behavioral evidence-based playbook: (1) write an Investment Policy Statement that defines target allocation and rebalancing triggers before any market move; (2) automate dollar-cost-averaging so contributions happen without a decision; (3) impose a 48–72 hour cooling-off period before any unplanned trade > 1% of portfolio; (4) keep a journal of every trade and the reason for it; (5) define 'kill criteria' before every buy. The mechanism: each tactic moves the decision from System 1 (fast, emotional) to System 2 (slow, deliberate).

Kahneman won the 2002 Nobel Memorial Prize in Economic Sciences for integrating insights from psychology into economics — specifically the work on heuristics, biases, and Prospect Theory developed with Amos Tversky in the 1970s and 80s (Tversky died in 1996 and was ineligible). The Prospect Theory paper (1979) is the foundation document for behavioral finance and remains one of the most-cited papers in economics. Kahneman died in March 2024; his 2011 book Thinking, Fast and Slow — the System 1 / System 2 framework — is the canonical lay introduction.

Check Out These Related Articles

Red vs. Blue: The Battle of Colors in Investment Marketing

Behavioral Finance Apps: Redefining Investor Decision-Making Dynamics

The Psychology Behind Investment Risk-Taking Behavior Among Millennials