Alternative Investments: Exploring Beyond Stocks and Bonds

Three things changed in alternative investments in 2025 and 2026 that are worth getting clear about before the next paragraph of theory: Vanguard put its brand on a private-markets product for the first time (the WVB All Markets Fund, jointly with Blackstone and Wellington, an interval fund permitted up to 40% in private markets — see Bloomberg's coverage); U.S. regulators cleared private credit managers to market into the roughly $13 trillion defined contribution (401(k)/403(b)) market; and in April 2026, Hamilton Lane launched two interval funds — credit and infrastructure — at $2,500 minimums and raised over $350M in commitments in roughly six weeks.

That is the price side of the alternatives story — the part that gets the headlines. The value side is what this guide is about: which alternative investments actually earn their place in a portfolio, what they cost in cash and in lockup, and which retail vehicles are real on-ramps versus marketing wrappers. The honest valuation question for any allocator considering alternatives right now is not "should I get exposure" — it is: what is the after-fee, after-lockup return I can expect from each vehicle over a five-to-ten-year holding period, and what is the single variable that would invalidate that expectation? We will take it asset class by asset class.

What Counts as an Alternative Investment

"Alternative investments" is a residual category — it means everything that is not a publicly-listed stock or a publicly-listed bond. That residual is doing more work in 2026 than it did in 2014. It now includes private credit funds and business development companies (BDCs), private equity and venture capital, real estate (publicly-traded REITs, non-traded REITs, crowdfunding platforms, opportunity-zone funds), commodities (futures, ETFs, physical metals), hedge funds and their retail proxies, infrastructure, farmland and timber, structured notes, and collectibles (art, wine, watches, sports cards). The residual category has gotten so large that "alts" is no longer one allocation decision; it is twelve.

The snapshot below is the one-screen version. Each row is a separate underwriting decision.

| Category | Typical minimum | Accreditation needed? | Liquidity | Target return (gross, 5–10 yr horizon) |

|---|---|---|---|---|

| Publicly-traded BDC / BDC ETF | A single share | No | Daily | 8–11% yield (BIZD 30-day SEC yield 8.56% as of Feb 2026) |

| Non-traded BDC | $1k–$25k | Often | Quarterly tender at NAV | 8–10% target distribution |

| Interval fund (private credit, infra) | $2,500–$25k | No (most retail share classes) | 5–25% NAV per quarter | 8–11% credit; mid-teens infra IRRs |

| Public REIT / REIT ETF | A single share | No | Daily | 8–10% total return |

| Non-traded REIT / RE crowdfunding | $10–$25k | Mixed | Limited / quarterly tender | 6–10% net target |

| Opportunity Zone fund | $25k–$250k | Typically | 10-year hold for full benefit | Capital-gains deferral + LTCG exclusion |

| Traditional private equity | $250k+ | Yes | 7–10 yr lockup | Target 13–18% IRR |

| Retail PE vehicle (e.g., Moonfare, HL Private Assets) | $10k–$25k | Mixed | Interval / tender | Target net 10–14% |

| Hedge fund (direct) | $500k+ | Yes | Quarterly–annual | Strategy-dependent |

| Long/short or multi-strategy ETF / interval fund | A single share / $2,500 | No | Daily or quarterly | Strategy-dependent |

| Commodity ETF (DBC, GSG, GLD) | A single share | No | Daily | Inflation-linked; not a target-return product |

| Art (Masterworks) | $20/share, $15k account | No | Limited secondary | Mid-single-digit to low-double-digit |

| Wine (Vint, Vinovest) | $25–$1,000 | No | Limited | Mid-single-digit |

| Farmland (AcreTrader, FarmTogether) | $5k–$25k | Often | 5–10 yr hold | 7–11% net target |

Numbers are public marketing or index data, not promises. Underwrite each one against your own time horizon before you fund it.

Private Credit and BDCs: The 2025–26 Story

Private credit is non-bank lending to companies — mostly senior secured, mostly floating-rate, usually direct to middle-market borrowers. As an industry it is on track to approach $4 trillion by 2030, up from roughly $2.2 trillion today. The reason the topic is everywhere in 2026 is not that the asset class is new — it is that the distribution of the asset class changed. The DC-plan opening cited above, the WVB All Markets Fund, Apollo's and Blue Owl's retail products, and a wave of new interval funds collectively mean that the retail-friendly wrappers (BDCs, interval funds, tender-offer funds) now hold roughly $550 billion AUM — about 25% of the $2.2T private credit industry, with nontraded BDCs alone projected to cross $1T by 2030.

The simplest retail entry point is a publicly-traded BDC or a BDC ETF. A BDC is a closed-end vehicle regulated under the '40 Act that lends to middle-market companies and must distribute the bulk of its taxable income — which is why yields read like high-yield bonds rather than equities. As of February 18, 2026, VanEck's BIZD ETF posted a 30-day SEC yield of 8.56%, and the MVIS US Business Development Companies Index dividend yield was 11.3% at year-end 2025 — nearly double leveraged loans (6.8%) and U.S. high-yield bonds (6.5%). BIZD itself holds roughly $1.6 billion in assets across about 35 BDCs, market-cap weighted, no accreditation gate, trades like any stock.

Three things to underwrite before treating that yield as "real":

- Default risk in the underlying loan book. BDC NAVs absorb credit losses, and the index has not yet been tested by a full down-credit cycle since the 2025–26 portfolio shift toward senior secured loans. The active 2025–26 pivot to senior secured is documented in the DFIN BDC market overview, and it is a structural improvement — but improvement is not immunity.

- The price-to-NAV discount. Publicly-traded BDCs frequently trade at meaningful discounts or premiums to their net asset value. Buying a portfolio of mid-market loans at 90 cents on the dollar is materially different than buying it at 110. Look at the discount when you size the position.

- Distribution coverage from net investment income. Distributions paid out of return of capital are not the same animal as distributions paid out of net investment income. Read the latest 10-Q before you assume the yield is sustainable.

For an investor who wants private credit exposure without a single-name BDC bet, BIZD or one of the interval funds discussed below is the cleaner route. What would change my mind on the broad BDC thesis? One thing, specifically: realized credit losses across the index running at more than 200 basis points annually for two consecutive years. A single bad year is noise; two consecutive years would tell me the recent senior-secured pivot has not, in fact, hardened the loan book against the cycle.

Real Estate: REITs, Crowdfunding, and Opportunity Zones 2.0

Real estate is the oldest alternative and the most accessible. The 2026 framing question is which wrapper, at what cost: a public REIT or REIT ETF (daily liquidity, full daily volatility, target 8–10% total return through a cycle), a non-traded REIT (quarterly or annual tender at NAV, fee load typically 1.5–3% all-in), a private real-estate crowdfunding platform like Fundrise at a $10 minimum or CrowdStreet (accredited, $25k+ deal minimums), or single-family-rental platforms like Arrived. The wrapper choice drives more of the after-fee return than the asset choice does — pay attention to where the fees sit.

The freshest piece of the real estate landscape is what the One Big Beautiful Bill Act of 2025 (OBBBA) did to the Opportunity Zone program. Signed July 4, 2025, OBBBA made the QOZ program a permanent feature of the tax code. For investments made after December 31, 2026, the structure is materially different from the 2017-vintage program: capital-gains deferral is five years rather than the previous staggered schedule; the 10% basis step-up at year five is retained; the seven-year additional basis step-up is eliminated; and the 10-year exclusion on new gains is preserved, but the stepped-up basis is frozen at the fair-market value on the year-30 anniversary. Existing zone designations sunset at the end of 2026; new zone designations are made within a 90-day window starting July 1, 2026; and new QOF reporting carries fines of up to $10K, or $50K for funds over $10M. The headline is that the program is permanent; the small print is that the math for any specific QOF is now meaningfully different post-2026 than it was for 2018–2024 vintage capital.

Farmland and timber sit in the same H3 with smaller volume but a clean narrative — long-duration real assets with inflation-linked cash flows. AcreTrader and FarmTogether opened the asset class to accredited retail at $5k–$25k minimums. Target net returns are usually in the high single digits over a 5–10 year hold; the chief risk is that you are illiquid by design.

Private Equity and Venture Capital

Private equity has the largest head-of-funnel search demand in the alternatives universe (60,500 monthly searches on the head term alone) and the most fee-loaded delivery. Traditional limited-partnership PE remains accreditation-gated, $250k+ minimums, 7–10 year lockups, and 2-and-20 fee schedules in the median fund. What is genuinely new is the retail-access layer: Moonfare and Hamilton Lane Private Assets Fund operate as fund-of-funds or interval-fund retail wrappers around the same institutional PE managers at $10k–$25k minimums and quarterly liquidity windows.

Two data points worth keeping in mind. First, the underlying private equity industry's exit math has shifted: per Moonfare's PE Outlook 2026, 71% of value created at PE exit now comes from revenue growth — the highest weighting since at least 2017. Less financial engineering, more operating improvement. That is a healthier composition of return, but it also means PE returns will increasingly track the operating economy rather than the leverage cycle. Second, 76% of private-wealth advisors say their clients view private markets as higher-reward than public markets. That is a sentiment number, not a math number, and it is the kind of survey result that should make a valuation-minded investor a little more cautious about entry pricing rather than a little more confident.

Venture is a separate animal — power-law return distribution, secondary-market frictions, vintage-year cohort effects. Retail-accessible VC products exist, but the asymmetric returns that justify the asset class are concentrated in a handful of funds the retail wrappers cannot get into.

Hedge Funds (and Their Retail Proxies)

Direct hedge-fund investment is still accreditation-gated, $500k–$1M minimums, 2-and-20 in the older funds, and quarterly-to-annual redemption windows. For most retail allocators, the relevant question is what subset of the hedge-fund return stream is available in registered, daily-liquid form. The answer in 2026 is: more than you think. Long/short equity, managed futures, merger arbitrage (MERFX is a long-standing example), and anti-beta (BTAL) all exist as ETFs or '40 Act mutual funds. Multi-strategy interval funds — many launched in the past three years — package what used to be hedge-fund-of-funds exposure into a $2,500-minimum quarterly-tender wrapper.

The honest framing is that these retail proxies are not hedge funds in disguise; they are registered-vehicle approximations of specific hedge-fund strategies. They get you a meaningful slice of the underlying strategy's exposure with daily NAV, daily liquidity (for ETFs), and a fee schedule one notch lower than the 2-and-20 originals. That is a fair trade for an allocator who does not have $500k earmarked for a single name and does not want a K-1.

Commodities

Commodities are the asset class that does best when the rest of the portfolio does worst — they are an inflation hedge first and a return-generating asset class second. The retail menu is essentially three layers: broad commodity ETFs (DBC, GSG, PDBC), precious metals (GLD, SLV, and the physical metals they hold), and energy/agriculture single-commodity products (USO for oil, UNG for natural gas).

Two structural costs are worth understanding before sizing a commodity allocation. The first is roll yield — futures-based commodity ETFs do not hold the physical asset; they hold front-month futures contracts and roll them forward. When the curve is in contango (later-dated futures more expensive than near-dated), the fund loses on every roll; in backwardation, it gains. DBC and GSG can run a 1–3% annual drag from contango alone in flat-spot markets. The second is expense — DBC at 0.85% is the cheap end of the commodity-ETF world; some have all-in costs north of 1.5%. Physical gold ETFs (GLD, IAU) avoid the roll problem entirely.

Gold itself has had an unusual 2024–26 run, driven by central-bank buying and dollar-reserve diversification rather than retail flows. The cleanest way to size that exposure is to decide whether you want gold as a long-term portfolio insurance position (5–10% allocation, hold through cycles) or as a tactical trade (in which case you are timing, not allocating, and the rest of this guide does not apply).

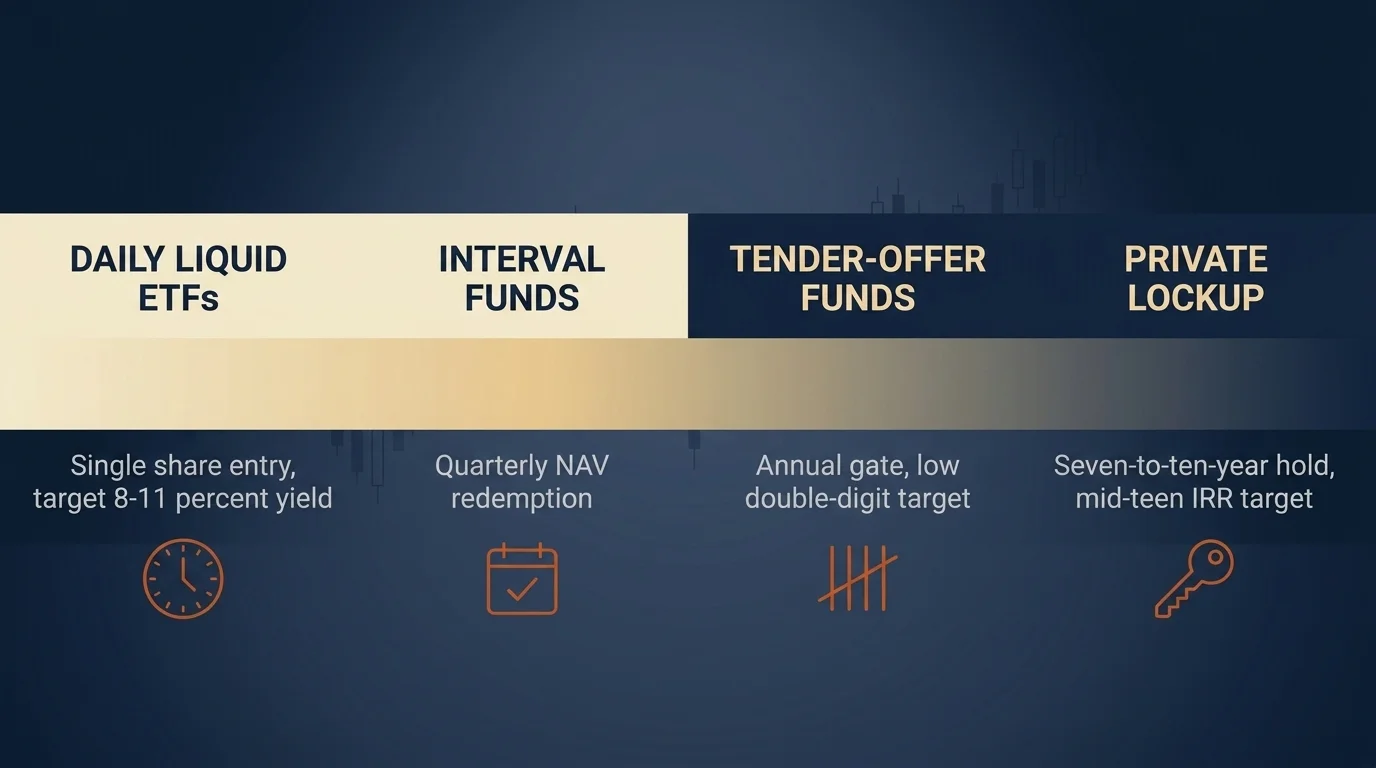

Interval Funds: The Retail On-Ramp to Private Markets

Interval funds are the most important structural innovation in retail alternatives in the last five years, and most allocators still do not fully understand them. The mechanics: a registered '40 Act fund that allows limited quarterly redemptions — typically 5%–25% of NAV per quarter — at NAV. Daily NAV pricing. 1099 tax reporting (not K-1). Minimums commonly $2,500. No accreditation required for retail share classes.

That structure is what makes them workable for private credit, private real estate, and private infrastructure — asset classes that need illiquidity to capture their illiquidity premium, but cannot operate in a daily-liquidity ETF wrapper. The Hamilton Lane Credit Income Fund (HLCIF) and the Hamilton Lane Private Infrastructure Fund (HLPIF), launched in April 2026 at $2,500 minimums, gathered $350M-plus in commitments in roughly six weeks. The WVB All Markets Fund (Vanguard × Blackstone × Wellington) is built on the same structure with a broader mandate: up to 60% public equities, 30% fixed income, and 40% private markets, announced May 2025 and debuting in late 2025.

The trade-off worth surfacing: a 5–25% quarterly redemption gate is not daily liquidity, and during a market dislocation the gate will mechanically fill before retail redemptions clear. You can underwrite the asset class you want exposure to inside an interval fund; you cannot underwrite the redemption window in a stress scenario. That is the right way to size the position — small enough that being temporarily gated does not change anything important about your financial life.

Collectibles and Passion Assets

The lowest-competition rank in the alternatives keyword cluster is collectibles, which is a useful tell about how seriously most editorial competitors are taking the category. The argument for collectibles as a portfolio asset is narrow and worth being honest about: they are low-correlation, they generate no cash flow, and their valuation rests on a thin layer of secondary-market comparables that can vanish in a downturn. They are an asset class in the sense that someone will buy what you own — they are not an asset class in the sense that cash flow compounds inside the position.

Within those caveats, the retail wrappers have improved. Masterworks securitizes shares of blue-chip art at $20 per share with a $15,000 account-open threshold. Vint and Vinovest do the same for fine wine at $25–$1,000 minimums. Rally and Otis fractionalize watches, cars, and sports cards. The cost structure is non-trivial — Masterworks charges a 1.5% annual management fee plus a 20% profit-share on exits — and the holding periods are long and uncertain.

A tax detail most retail investors miss: under U.S. tax law, collectibles are subject to a maximum long-term capital-gains rate of 28%, materially higher than the 20% maximum on long-term gains for stocks. That is a structural after-tax drag of 800 basis points on every realized gain. Size accordingly.

Structured Notes and Other Tax-Advantaged Niches

Structured notes — bank-issued debt instruments with returns linked to an underlying index or basket, often with principal-protection features — sit in a corner of the alts universe that gets neglected because the products are complex and the issuance market is opaque. They are worth a paragraph: they let an allocator dial in a payoff structure (capped upside, defined downside, contingent coupons) at the cost of credit exposure to the issuing bank and limited secondary liquidity. The structure is right for a small slice of a portfolio, sized in a way where the issuer credit exposure is genuinely de minimis.

The other tax-advantaged angle is Section 1031 like-kind exchanges for direct real estate, energy partnerships with intangible drilling cost (IDC) deductions, and the Opportunity Zone framework discussed above. All of them work for the right investor and the wrong allocation size; none of them work as a substitute for an actual valuation framework.

How Much of a Portfolio Belongs in Alternatives?

The Yale endowment model, popularized by David Swensen, runs alternatives above 60% of portfolio assets — but the endowment has a perpetual time horizon, a tax-exempt structure, and a level of manager access retail does not have. Most retail-investor frameworks land in the 5–20% range, and the cleanest way to think about it is to reframe the traditional 60/40 portfolio as 50/30/20: 50% stocks, 30% bonds, 20% alternatives spread across two or three sub-categories.

The directional case for that 20% is that individual-investor alts AUM is projected to grow from $4 trillion today to $12 trillion over the next decade; semi-liquid and evergreen funds have grown 60% since 2022; and Hamilton Lane forecasts 20% of all private-market capital will sit in evergreen structures within a decade. The macro flow is real; that does not mean the allocation is automatically a good idea for any specific investor.

Three sizing checks before any allocation decision:

- Do you have a cash reserve equal to at least six months of expenses sitting outside the alts allocation? If not, you do not yet have the slack to hold a 7–10 year illiquid position through a personal cash-flow event.

- Can you tolerate quarterly mark-to-NAV volatility on a position you cannot easily exit? Interval funds and non-traded REITs print quarterly NAVs that move; the lockup means you cannot trade around those moves.

- Are you sized small enough that being gated in a stress scenario does not change your life? That is the real risk in retail alternatives — not that the asset class underperforms, but that you need cash precisely when the redemption gate fills.

If all three are yes, a 10–20% alternatives allocation looks reasonable. If any of them are no, the right answer is a smaller allocation, or none, until they are.

Related Article: Sustainable Investing: Aligning Values with Financial Goals

Are You an Accredited Investor? (And Why It Matters Less Than It Used To)

The federal accredited-investor definition matters less than it used to because the retail-friendly wrappers — BDC ETFs, interval funds, real-estate crowdfunding at sub-$1k minimums — do not require accreditation. But it still gates direct PE, hedge funds, traditional non-traded BDCs, and most CrowdStreet/RealtyMogul deals.

The thresholds, per the SEC's accredited-investor page: $200,000 in individual income (or $300,000 joint) for each of the prior two years with a reasonable expectation of the same in the current year; or $1 million in net worth, excluding the value of a primary residence; or — added in the SEC's 2020 amendments — a Series 7, 65, or 82 license, regardless of income or net worth; or status as a "knowledgeable employee" of a private fund (qualifying for that fund family's offerings, not all private offerings).

The 2020 expansion is the under-reported part. If you hold an active Series 65 license — the credential commonly held by registered investment advisors — you are accredited regardless of net worth. That alone reframes the accreditation question for a substantial number of finance professionals and licensed advisors.

Alternative Investment Platforms: A Comparison Table

The comparison below is the snippet-magnet section. Every platform on the table is publicly soliciting retail capital as of May 2026; minimums and fees are from each platform's published material or third-party verification. Marketed targets, not promised returns.

| Platform | Asset class | Minimum | Accreditation | Fees | Liquidity |

|---|---|---|---|---|---|

| Fundrise | Private real estate | $10 | No | 0.85% advisory + 0.85% asset mgmt | Quarterly tender (gated in stress) |

| Yieldstreet | Multi-asset private credit / RE / art | $10,000 | Mixed by deal | 0–2.5% management | Deal-by-deal lockup |

| Masterworks | Securitized blue-chip art | $20/share, $15k account | No | 1.5% AUM + 20% profit share | Limited secondary |

| Hamilton Lane HLCIF | Private credit (interval) | $2,500 | No (retail share classes) | Disclosed in prospectus | 5–25% NAV per quarter |

| Hamilton Lane HLPIF | Private infrastructure (interval) | $2,500 | No (retail share classes) | Disclosed in prospectus | 5–25% NAV per quarter |

| WVB All Markets Fund | Multi-asset incl. private mkts | Per fund docs | No | Disclosed in prospectus | Quarterly 5–25% NAV per Bloomberg coverage |

| CrowdStreet | Commercial real estate deals | $25,000 | Yes | Sponsor-specific | Deal lockup |

| RealtyMogul | Commercial / private REITs | $5,000 / $25,000 | Mixed | Sponsor-specific | Deal lockup |

| Arrived | Single-family rentals | $100 | No | 1% gross rents + sourcing | 5–7 yr hold target |

| Moonfare | Retail PE feeder | $50,000+ | Yes | Disclosed per fund | Limited secondary |

| AcreTrader | Farmland | $5,000+ | Often | 0.75% + 5% commission | 5–10 yr hold |

| Vinovest | Fine wine | $25–$1,000 | No | 2.5% + 2.85% storage | Limited secondary |

The right way to read this table is by liquidity column first, then fee column, then minimum. The fee load on an illiquid 7–10 year position compounds in the wrong direction; a 2% all-in fee is six percentage points of cumulative drag over six years. The cost structure of the platform is doing as much work in your after-fee return as the underlying asset selection.

What Would Change My Mind

The integrative argument for alternative investments in 2026 rests on three claims: that retail-accessible vehicles have closed enough of the structural gap that an individual investor can reasonably access institutional-quality private credit, real estate, and PE at a fee load one notch above public-market index funds; that the underlying assets still earn an illiquidity premium that survives the fee layer; and that the diversification benefit is real over a five-to-ten-year holding period.

What would change my mind on that argument? One thing, specifically: the next full down-credit cycle revealing realized losses in the new generation of retail interval funds substantially worse than the marketed return-after-default-assumption suggested. Not a single bad quarter — interval funds are designed to absorb quarter-by-quarter mark-to-NAV volatility. Two consecutive years of realized credit losses across the retail private credit cohort running above 200 bps annually would tell me the retail wrappers were structured around a benign credit assumption that did not hold, and that the after-fee illiquidity premium had been compressed below the level that justifies the lockup. I am watching the realized-loss data through the next credit cycle, not the quarterly NAV print and not the marketed yield.

Until then, the math reads like a reasonable case for a 10–20% allocation, sized small enough to hold through a stress scenario, diversified across two or three of the sub-categories above, and tilted toward the vehicles where the fee layer is at least transparent. The point of all of this is not to chase a yield headline; it is to add one more lever to a portfolio's expected after-fee, after-tax return over a five-to-ten-year horizon. If the lever does not pull that result in the right direction, the allocation is doing nothing for you and should be smaller.

This article is for educational purposes and is not individual financial advice. Alternative investments often carry illiquidity, complex tax treatment, fee layers that compound over multi-year holding periods, and concentrated default risk in down credit cycles. Consult a licensed financial advisor and read each offering's prospectus before allocating capital. Past performance and marketed targets are not guarantees of future returns.

Frequently Asked Questions

Alternative investments are asset classes outside traditional stocks and bonds — private credit, business development companies (BDCs), private equity, real estate, hedge funds, commodities, and collectibles. In 2025–26 they became newly accessible to retail investors via interval funds (e.g., Hamilton Lane HLCIF at a $2,500 minimum) and joint ventures like the WVB All Markets Fund from Vanguard, Blackstone, and Wellington.

Not always. Public BDC ETFs like VanEck's BIZD trade on the open market with no accreditation needed; Fundrise opens private real estate at a $10 minimum to anyone; the WVB All Markets Fund and Hamilton Lane HLCIF interval funds open to non-accredited retail at $2,500. Traditional private equity, hedge funds, and many private credit funds still require accreditation: $200K individual income ($300K joint), $1M+ net worth excluding primary residence, or a Series 7/65/82 license.

As low as $10 (Fundrise private REITs), $20 per share with a $15K account threshold (Masterworks art), $2,500 (Hamilton Lane HLCIF / HLPIF interval funds), $10,000 (Yieldstreet), and $250,000+ for traditional private equity.

The MVIS US Business Development Companies Index dividend yield was 11.3% at the end of 2025 — nearly double leveraged loans (6.8%) and U.S. high-yield bonds (6.5%). VanEck's BIZD ETF posted an 8.56% 30-day SEC yield as of February 18, 2026.

Endowment-style portfolios (Yale model) can allocate 60%+ to alternatives. Most retail-investor frameworks target 5%–20%, often reframing the traditional 60/40 (stocks/bonds) as 50/30/20 (stocks/bonds/alts). Size only after you have a six-month cash reserve outside the allocation, can tolerate quarterly mark-to-NAV volatility, and are small enough that being gated in a stress scenario does not change your life.

Private credit is non-bank lending to companies — typically senior secured, often floating-rate. Industry AUM is on track to approach $4 trillion by 2030, up from roughly $2.2 trillion today. U.S. regulators recently cleared private credit managers to market into the ~$13 trillion defined contribution (401(k)/403(b)) market, a structural opening that is reshaping retail access. Retail-friendly vehicles — BDCs, interval funds, BDC ETFs like BIZD — now hold about $550 billion AUM.

A registered '40 Act fund that allows limited quarterly redemptions — typically 5%–25% of NAV per quarter — at NAV. Interval funds offer 1099 tax reporting, daily NAV pricing, and access to illiquid assets (private credit, private infrastructure, real estate) at retail-friendly minimums (commonly $2,500). The Hamilton Lane Credit Income Fund (HLCIF) raised over $350 million in commitments in roughly six weeks after its April 2026 launch.

Signed July 4, 2025, OBBBA made the Qualified Opportunity Zone program permanent. For investments after Dec 31, 2026, capital-gains deferral is five years; the 10% basis step-up at year 5 is retained; the additional year-7 step-up is eliminated; the 10-year exclusion on new gains is preserved but stepped-up basis freezes at the fair-market value on the year-30 anniversary. Current zone designations sunset at the end of 2026, with new designations made within a 90-day window starting July 1, 2026. New QOF reporting carries fines of up to $10K (or $50K for funds over $10M).

For non-accredited retail investors, the simplest entry is a publicly-traded BDC ETF like VanEck's BIZD — ~$1.6 billion AUM, ~35 BDC holdings, 8.56% 30-day SEC yield as of February 2026, no accreditation required, traded on a major exchange. The next step up is an interval fund like Hamilton Lane HLCIF ($2,500 minimum, quarterly liquidity). Direct nontraded BDCs and private credit limited partnerships remain accreditation-gated.

The data argues yes for diversification, with caveats. Individual-investor alts AUM is projected to grow from $4 trillion today to $12 trillion over the next decade. BDCs are yielding ~11% on the index level. 76% of private-wealth advisors say their clients view private markets as higher-reward than stocks and bonds, and 71% of PE exit value now comes from revenue growth — the highest weighting since at least 2017. Caveats: longer lockups, higher fees (often 2-and-20 on traditional funds), tax complexity, and concentrated default risk in down credit cycles.

Check Out These Related Articles

Securing Financial Health: Safeguarding Consumer Interests in Investment Products

Finance Mentor vs Sponsor: What Actually Compounds a Career

Youth-Led Financial Revolutions: Crowdsourcing as a Catalyst for Investment Innovation